Commercial and Residential Leases

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Consider the distinction between a heavily regulated public utility and a private, unregulated commodities market. In one domain, state statutes dictate the pricing, the terms of service, and the precise rights of the consumer. In the other, sophisticated parties sit across a negotiating table, entirely unshielded by the state, and draft their own economic reality. For a New York real estate professional, navigating property law requires understanding that residential and commercial leases exist in these two fundamentally separate legal universes.

Residential leasing is governed by strict statutory boundaries designed to protect human beings in their homes. Commercial leasing, however, is a blank canvas bounded only by the limits of contract law. A salesperson who treats a commercial client like a residential tenant—or vice versa—will inevitably misguide their client and jeopardize the transaction.

Here is the architecture of New York lease law, broken down by the precise mechanisms that govern the residential consumer and the commercial enterprise.

To understand New York leasing, you must first understand the default assumptions the law makes about the parties involved.

The law views a residential tenant as vulnerable. Because housing is a fundamental human need, commercial leases generally lack the statutory consumer protections granted to residential tenants. When you broker a commercial deal, you are operating in a space where commercial lease terms are primarily governed by contract law rather than statutory housing regulations.

This distinction manifests most dramatically in how the physical space is maintained and what happens when a relationship breaks down.

The Implied Warranty of Habitability

By operation of law, every residential lease in New York includes a non-waivable implied warranty of habitability. You cannot draft a residential lease that asks a tenant to accept an apartment "as-is" if the plumbing does not work. The implied warranty of habitability requires residential landlords to keep premises safe and suitable for human living. It is the unbreakable genetic code of a residential lease.

Conversely, commercial leases do not include a statutory implied warranty of habitability. If a commercial tenant leases a warehouse with a leaky roof, and the lease states the tenant is responsible for roof repairs, the tenant must fix it or conduct their business under an umbrella. There is no statutory safety net.

Eviction and Self-Help

When a lease goes sour, the rules of engagement are entirely different. Residential landlords are prohibited from using self-help eviction methods against residential tenants. A residential landlord cannot change the locks or shut off the electricity to force a non-paying tenant out; they must undergo a formal, often lengthy, judicial eviction process.

However, because commercial spaces do not involve human shelter, commercial leases may include provisions allowing a landlord to use peaceful self-help to recover possession of the premises. If a commercial tenant stops paying rent and the contract permits it, the landlord can legally change the locks on the storefront in the middle of the night.

When representing clients looking for apartments, your daily reality is governed by a web of state laws designed to cap costs, preserve tenancy, and manage the handling of funds.

Rent Regulation: ETPA and the End of Luxury Decontrol

In a purely free market, housing prices fluctuate with demand. But New York recognizes that unrestricted housing costs can displace entire communities. The Emergency Tenant Protection Act (ETPA) of 1974 establishes the framework for rent stabilization in eligible New York municipalities.

The state does not impose rent stabilization arbitrarily. It requires a mathematical trigger: municipalities in New York can adopt the Emergency Tenant Protection Act if the local housing vacancy rate falls below five percent. A vacancy rate below five percent signals a "housing emergency"—meaning the supply of housing is so constrained that tenants have lost virtually all bargaining power.

Crucial Distinction: The Emergency Tenant Protection Act applies exclusively to residential properties. There is no such thing as a rent-stabilized commercial storefront.

For the residential tenant, ETPA is a powerful shield. Rent stabilization under the Emergency Tenant Protection Act limits the percentage by which a landlord can increase rent upon lease renewal. These limits are not pulled from thin air; local Rent Guidelines Boards dictate the maximum allowable rent increases for rent-stabilized apartments each year.

Furthermore, rent stabilization guarantees residential tenants the right to renew their leases. A landlord cannot simply decline to renew a rent-stabilized lease because they want a different tenant. When renewal time comes, rent-stabilized tenants in New York have the right to choose between a one-year or a two-year lease renewal term.

For decades, landlords utilized a loophole to remove units from this protective framework. Luxury decontrol previously allowed landlords to remove apartments from rent regulation based on high rent amounts and high tenant income. If the rent crossed a certain threshold and the tenant earned above a specific income, the unit reverted to free-market pricing. However, a seismic shift occurred in recent property law: the Housing Stability and Tenant Protection Act (HSTPA) of 2019 permanently eliminated luxury decontrol in New York. Once an apartment is rent-stabilized today, it remains stabilized regardless of how high the legal regulated rent goes or how much the tenant earns.

Security Deposits: The 14-Day Rule

Before 2019, it was common for landlords to ask tenants with poor credit for three or four months of rent upfront. That is now illegal. New York residential landlords cannot charge a security deposit exceeding the amount of one month of rent. Furthermore, New York residential landlords are prohibited from collecting the last month of rent in advance along with a security deposit. At lease signing, a residential tenant can only be required to produce the first month's rent and exactly one month's security deposit.

The state also strictly monitors how these funds are stored and returned. New York landlords of buildings with six or more residential units must place security deposits in an interest-bearing bank account.

When the tenant leaves, the clock immediately starts ticking. A residential landlord must return a tenant's security deposit within fourteen days after the tenant vacates the apartment. To prevent surprise deductions, residential tenants have a statutory right to request a pre-move-out inspection to identify potential security deposit deductions before they hand over the keys. If the landlord does withhold money for damages, residential landlords must provide an itemized written statement of deductions if retaining any portion of a security deposit. Failure to meet these 14-day requirements can result in the landlord forfeiting the right to keep any of the deposit.

Subleasing and the Duty to Mitigate

Life happens. Tenants get transferred for work or need to break their leases. If a residential tenant needs to leave early, New York residential tenants hold a statutory right to sublease their apartments, provided they follow the proper legal procedures. Even if the lease explicitly forbids subletting, a residential landlord cannot unreasonably withhold consent to a residential tenant's sublease request.

If a tenant simply abandons the apartment entirely, the landlord cannot just let the apartment sit empty and sue the former tenant for the remaining rent. New York residential landlords possess a statutory duty to mitigate damages if a tenant abandons the property. This means the statutory duty to mitigate damages requires residential landlords to make reasonable efforts to re-rent an abandoned apartment at fair market value to minimize the financial hit to the departing tenant.

Walk out of the residential apartment building and down to the retail storefront on the ground floor. The legal landscape here is entirely inverted. There are no Rent Guidelines Boards, no statutory rights to sublease, and no caps on security deposits.

Because businesses are assumed to be sophisticated entities capable of negotiating their own risks, commercial landlords are exempt from the strict fourteen-day security deposit return deadline mandated for residential landlords. The return of a commercial deposit takes as long as the contract says it takes. Similarly, New York commercial landlords have no statutory duty to mitigate damages upon a tenant's abandonment of the leased space. If a commercial tenant goes bankrupt and abandons a $10,000-a-month retail space with three years left on the lease, the landlord can let the space sit completely dark and successfully sue the tenant for the entire remaining balance.

Furthermore, commercial tenants depend entirely on specific lease contract language for any right to assign or sublet the space. If the lease does not explicitly grant the right to sublet, the commercial tenant has no right to do so.

Structuring the Commercial Lease: Clauses and Economics

Because the state provides no default rules, commercial leases are heavily engineered documents. Every right must be explicitly written.

- The Use Clause: A landlord wants to carefully curate the mix of tenants in a commercial building. Therefore, a commercial lease use clause strictly dictates the permissible business activities a tenant may conduct in the rented space. If a tenant signs a lease to operate a "high-end boutique shoe store," they cannot pivot to selling hot food without violating the lease.

- Renewals: Unlike rent-stabilized residential tenants, commercial tenants have no automatic right to stay. A commercial lease renewal option grants the tenant the contractual right to extend the lease term. To avoid unpredictable negotiations at the end of the term, commercial lease renewals frequently specify predetermined rent increases for the extended term.

Escalation Clauses: Hedging Against Inflation

Commercial leases often last five, ten, or twenty years. Landlords cannot predict the cost of property taxes, heating oil, or maintenance a decade in advance. To protect their profit margins, landlords utilize rent escalation clauses, which allow commercial landlords to pass increased building operating costs directly to tenants.

There are three primary methods of commercial rent escalation you must understand:

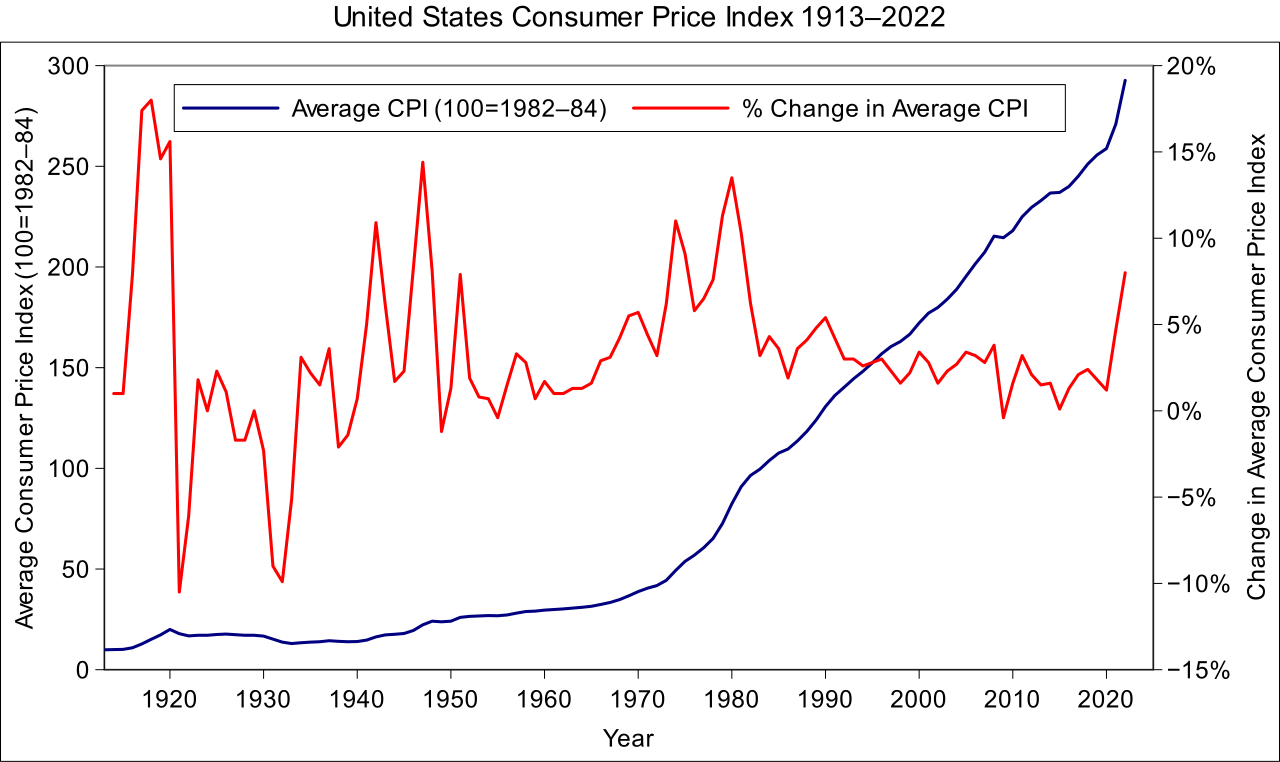

- Consumer Price Index (CPI) Escalation: This is a broad economic hedge. A Consumer Price Index escalation clause adjusts commercial rent proportionally to changes in the rate of inflation.

- Porter's Wage Escalation: This is a unique real estate metric. It is difficult to audit a landlord's exact maintenance costs, so parties agree to use an external benchmark. A porter's wage escalation clause bases commercial rent increases on the hourly wage of local unionized building maintenance workers. If the union negotiates a 4% raise for porters, the tenant's rent increases proportionately.

- Direct Operating Expense Escalation: This requires rigorous accounting. A direct operating expense escalation clause passes specific building maintenance costs to the commercial tenant, usually calculated based on the tenant's pro-rata share of the building's square footage.

The Financial Triad: SNDA and Estoppel

When a commercial property is sold or refinanced, the banks involved need absolute certainty about the status of the leases inside the building. This introduces a suite of standard commercial clauses that agents must master.

The first is the SNDA (Subordination, Non-Disturbance, and Attornment) agreement, which manages the relationship between the tenant, the landlord, and the landlord's mortgage lender:

- Subordination: The bank demands priority. A subordination clause makes a commercial tenant's leasehold interest secondary to the landlord's mortgage. If the landlord defaults, the bank's claim supersedes the tenant's lease.

- Non-Disturbance: The tenant demands protection in return. A non-disturbance agreement protects a commercial tenant from eviction during a landlord's mortgage foreclosure, provided the tenant is still paying rent.

- Attornment: The bank demands a seamless transition. An attornment clause requires a commercial tenant to acknowledge a new property owner as the landlord following a sale or foreclosure.

Finally, when a building is under contract to be sold, the buyer will ask the current tenants to sign an estoppel certificate. An estoppel certificate legally binds a commercial tenant to the factual lease terms acknowledged within the document. If the tenant signs an estoppel stating their security deposit is $5,000, they cannot later claim to the new owner that they actually put down $10,000. It acts as a permanent, legally binding snapshot of the lease at a specific moment in time.

Mastering New York leasing requires keeping these two frameworks distinct in your mind. The table below summarizes the key legal divergences you will encounter in your daily practice.

| Feature | Residential Leases (Statutory Universe) | Commercial Leases (Contractual Universe) |

|---|---|---|

| Implied Warranty of Habitability | Mandatory and non-waivable. | None. Property is taken as defined in the lease. |

| Eviction Mechanism | Strict judicial process; self-help prohibited. | Peaceful self-help permitted if written in the contract. |

| Rent Increases | Capped by Rent Guidelines Boards if ETPA applies. | Dictated by the market, escalations, and the lease. |

| Security Deposits | Max 1 month; 14-day return with itemized list. | Governed strictly by the negotiated lease. |

| Duty to Mitigate Damages | Landlord must make reasonable efforts to re-rent. | None. Landlord can let space sit empty and collect rent. |

| Subleasing Rights | Statutory right; landlord cannot unreasonably withhold. | Entirely dependent on lease language. |

Understand these rules not just as abstract laws, but as the underlying physics of every transaction you facilitate. Knowing whether you are standing in the regulated landscape of a residential home or the open market of a commercial enterprise will define your success as a real estate professional.