Like-Kind Exchanges (1031 Exchange)

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

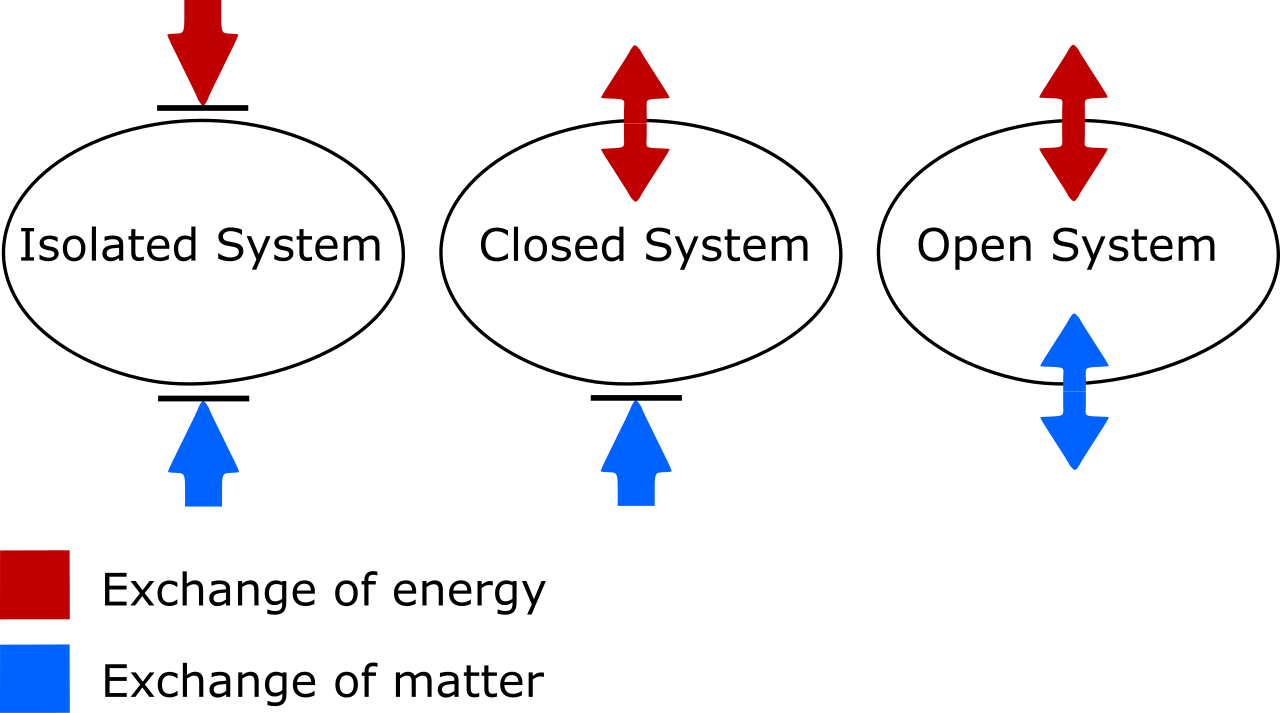

In physics, the law of conservation of energy dictates that energy cannot be created or destroyed within a closed system; it simply transforms from one state to another. In the realm of real estate finance, the United States tax code offers a remarkably similar mechanism for preserving capital. Governed by Section 1031 of the Internal Revenue Code, a 1031 exchange allows a real estate investor to defer paying capital gains taxes on an investment property when the investment property is sold, provided that the capital flows seamlessly into a qualifying replacement property.

For a real estate professional operating in New York, where commercial portfolios and multi-family investments represent vast concentrations of wealth, mastering this concept is essential. You are not merely trading physical structures; you are managing the thermodynamic flow of your client's equity. If the transaction is structured correctly, the wealth is perfectly conserved and transformed into a new asset. If the rules are broken, the "closed system" ruptures, and capital leaks out in the form of immediate taxation.

The fundamental prerequisite for a 1031 exchange is the classification of the properties involved. To qualify for a 1031 exchange, the relinquished property and the replacement property must be held for productive use in a trade, business, or for investment.

Because the IRS requires the asset to be an engine of business or investment, primary personal residences do not qualify for a 1031 tax-deferred exchange. An individual cannot sell the home they sleep in every night and use Section 1031 to avoid taxes on the gain.

When clients hear the phrase "like-kind," they often intuitively—and incorrectly—assume that the replacement property must be identical in form to the one being sold. They believe an apartment building must be exchanged for an apartment building. In taxation jurisprudence, the term like-kind refers to the nature or character of the real estate rather than the property's grade or quality.

This creates a tremendously broad canvas for the investor. The rule is absolute: any real estate held for investment or business purposes is considered like-kind to any other real estate held for investment or business purposes.

The Extremes of "Like-Kind" An investor can exchange vacant land for a commercial building under 1031 exchange rules because both are considered like-kind real estate. A client could sell a parking lot in Queens and acquire a strip mall in Buffalo, or sell a timber farm upstate to buy a rental condominium in Manhattan. As long as both are U.S. real property held for investment, the nature of the asset satisfies the tax code.

The single most fatal error an investor can make in a 1031 exchange occurs at the closing table of the relinquished property. If a taxpayer directly takes possession of the cash from the sale of a relinquished property, the transaction is immediately disqualified from being a 1031 tax-deferred exchange.

In the eyes of the IRS, the moment the cash touches the taxpayer's bank account, the economic gain has been realized. The system is no longer closed; the money has been extracted, even if the taxpayer intended to use it to buy a new property the very next day.

To prevent this "constructive receipt" of funds, the code requires an arbiter. A Qualified Intermediary (QI) is an independent third party who facilitates a 1031 exchange by holding the funds from the sale of the relinquished property. The QI legally inserts themselves into the transaction, sells the relinquished property on behalf of the taxpayer, holds the capital in a secure escrow, and then uses that exact capital to purchase the replacement property.

The Requirement of Absolute Independence

The intermediary must be truly independent. A taxpayer cannot use their attorney, accountant, or employee to hold the funds. Furthermore, a real estate agent who has represented the taxpayer in a transaction within the past two years cannot serve as the Qualified Intermediary for that taxpayer's 1031 exchange. If you are acting as the client's broker, you must ensure they hire an institutional QI well before the closing of the relinquished property.

When we speak of deferring taxes in an exchange, we are looking for a perfectly efficient transfer. However, if any capital "leaks" out of the exchange into the hands of the investor—either as cash or debt relief—that leakage is subject to taxation. In tax parlance, this taxable leakage is known as "boot."

Boot refers to any non-like-kind property or cash received by the investor during a 1031 exchange transaction. The receipt of boot in a 1031 exchange triggers a taxable event for the investor to the extent of the boot received. Receiving boot does not invalidate the entire exchange; it simply means the exchange is partially taxable.

There are two primary forms of boot you will encounter in real estate finance:

- Cash Boot: The investor sells a property yielding $1,000,000 in equity, but only uses $800,000 to acquire the replacement property, taking the remaining $200,000 in cash. The $200,000 is cash boot and is subject to capital gains tax.

- Mortgage Boot: This concept is more subtle but equally vital. Mortgage boot occurs in a 1031 exchange when the mortgage liability assumed on the replacement property is less than the mortgage liability paid off on the relinquished property.

Consider a scenario where an investor sells a building for $3,000,000 that carries a $2,000,000 mortgage. They buy a replacement property for $2,000,000 in cash and take on no new mortgage. The IRS views debt relief as an economic benefit. Because the investor's liabilities decreased by $2,000,000, that reduction is treated as taxable mortgage boot.

The Golden Rules of Complete Deferral

To prevent any boot from occurring, the transaction must satisfy two strict financial parameters:

| Complete Deferral Requirement | Application in Practice |

|---|---|

| Value Matching | To defer all capital gains taxes in a 1031 exchange, the replacement property must be of equal or greater value than the relinquished property. |

| Equity Matching | To defer all capital gains taxes in a 1031 exchange, the investor must reinvest all net equity from the sale of the relinquished property into the replacement property. |

The Internal Revenue Service strictly dictates the velocity at which an exchange must occur. The timeline begins the moment the deed of the relinquished property is transferred to the buyer. From that precise day, two unyielding deadlines are triggered.

- The 45-Day Rule: The 1031 exchange identification period requires the investor to identify potential replacement properties within 45 days of selling the relinquished property. This identification must be made in writing, signed, and delivered to the Qualified Intermediary.

- The 180-Day Rule: The 1031 exchange acquisition period requires the investor to close on the replacement property within 180 days of selling the relinquished property.

A critical mathematical necessity to grasp is that the 45-day identification period and the 180-day closing period in a 1031 exchange run concurrently. The investor does not get 45 days to identify plus an additional 180 days to close. Day 45 is merely a waypoint on the 180-day journey. If a client identifies a property on day 44, they have precisely 136 days left to complete the acquisition.

These constraints are unforgiving. The strict 45-day and 180-day deadlines in a 1031 exchange cannot be extended even if the final day falls on a weekend or a legal holiday. If day 45 is Thanksgiving Day, the identification must be finalized and delivered before the deadline passes. There are no exceptions for market conditions, delayed appraisals, or uncooperative lenders.

During the 45-day identification window, an investor cannot simply hand the Qualified Intermediary a list of fifty random properties they might want to buy. The IRS requires specificity and limits the scope of potential targets through three distinct identification rules. The investor must choose one of these rules to follow.

1. The Three-Property Rule

The most commonly utilized strategy by real estate professionals. The Three-Property Rule in a 1031 exchange allows an investor to identify up to three potential replacement properties regardless of the properties' total fair market value. Why it matters: A client selling a $1,000,000 duplex can identify three massive $50,000,000 commercial towers. As long as they buy at least one of those three exact properties to satisfy their required value, the exchange is valid.

2. The 200% Rule

If an investor wishes to diversify a large asset into many smaller assets, three properties may not be enough. The 200% Rule in a 1031 exchange allows an investor to identify any number of replacement properties as long as their total fair market value does not exceed 200% of the relinquished property's value. Why it matters: If the client sells a property for $2,000,000, they can identify ten, fifteen, or twenty potential replacement properties, provided the cumulative asking price of all identified properties does not exceed $4,000,000.

3. The 95% Rule

Reserved largely for massive institutional portfolio acquisitions, the 95% Rule in a 1031 exchange allows an investor to identify any number of replacement properties if the investor ultimately acquires properties with a total value of at least 95% of the identified properties' value. Why it matters: An investor can identify $10,000,000 worth of assorted properties without adhering to the three-property limit or the 200% limit. However, the margin for error is virtually nonexistent. If deals fall through and they only close on $9,000,000 (90%) of the identified properties by day 180, the entire exchange fails and becomes fully taxable.

Understanding the mechanics of Section 1031—the strict adherence to timelines, the exactness required to avoid boot, and the absolute necessity of the Qualified Intermediary—elevates a real estate salesperson from a mere transaction coordinator to a true financial strategist. By ensuring the closed system of equity remains intact, you provide one of the most powerful wealth-building mechanisms available in modern American finance.