Ownership, Beneficiaries, and Premium Modes

An insurance policy is not merely a conditional promise to pay; it is a piece of legal property. Just as holding the title to a physical estate grants the owner the authority to decide who resides there, who inherits it, and how the mortgage is structured, a health insurance policy operates on the same architectural principles. The policyowner acts as the sole director of this contract. Understanding the specific mechanisms of this control—who holds the rights, how dependents are shielded by law, who receives the capital when tragedy strikes, and the mathematical trade-offs of funding the policy—is the foundation of insurance mechanics. You are not just selling a product; you are architecting a financial failsafe governed by precise legal rules.

At the center of every insurance contract is the policyowner. It is a fundamental rule of contract law that the policyowner possesses all ownership rights contained in a health insurance policy. The insured may be the person whose health or life is being evaluated, but the owner holds the actual levers of control.

Because the owner controls the contract, they possess two critical, non-transferable powers:

- The health insurance policyowner has the exclusive right to name or change the policy beneficiary. The insurance company will only accept beneficiary instructions from the owner, regardless of who is paying the premiums.

- The health insurance policyowner has the exclusive right to select the premium payment mode. This dictates the cash-flow mechanics of the policy, which directly impacts the policy's total cost.

Health insurance frequently extends beyond the individual to protect the family unit. Both federal law and state regulations impose strict parameters on how and when dependents are covered.

Newborns and Adopted Children

Biological and adoptive realities do not wait for bureaucratic paperwork. Therefore, insurance law provides immediate, automatic protection for the most vulnerable dependents:

- Newborn children are automatically covered under a parent's health insurance policy from the exact moment of birth. There is no waiting period or exclusion for congenital defects.

- Similarly, adopted children are covered under a parent's health insurance policy from the exact date of placement for adoption.

However, this automatic coverage is not an indefinite free pass. To sustain it, the policyowner must usually notify the insurer and pay any required additional premium within 31 days of birth (or placement). Failure to notify the insurer and pay the premium within this 31-day window allows the insurer to drop the child's coverage.

The Affordable Care Act (ACA) Mandates

Before the ACA, dependents aging out of pediatric care or leaving for college routinely lost health coverage. Today, federal law establishes a universal safety net: the Affordable Care Act mandates that health insurance plans must allow dependent children to remain on a parent's policy until age 26.

This mandate applies broadly, stripping away many traditional disqualifiers:

- Marital Status: Married dependent children can remain on a parent's health insurance policy until age 26 under the Affordable Care Act.

- Residency: Geography does not sever the insurance bond. Dependent children do not need to live with the parent to remain on the parent's health insurance policy until age 26.

Dependent Children with Disabilities

What happens when a child reaches age 26 but cannot care for themselves? Insurance law provides a permanent exception to the limiting age for severe disabilities.

Unmarried children who are incapable of self-support due to physical or mental disability can remain on a parent's health policy indefinitely.

This is not automatic; it requires documentation. Proof of a child's incapacity and dependency must typically be provided to the insurer within 31 days of the child reaching the limiting age (e.g., their 26th birthday). Once established, the insurer may occasionally request ongoing proof, but the coverage remains intact as long as the dependency and the parent's policy endure.

While traditional health insurance pays benefits directly to medical providers or reimburses the insured, Accidental Death and Dismemberment (AD&D) policies operate differently. They distribute lump-sum cash payouts, requiring precise beneficiary designations.

In an AD&D policy, payouts are split into two distinct categories:

The Capital Sum: This is the payout for severe, non-fatal injuries (like the loss of a limb or eyesight). Because the insured survives the accident, the capital sum for dismemberment is paid directly to the living insured.

The Principal Sum: This is the maximum payout for accidental death. Because the insured does not survive, the principal sum for loss of life is paid to the named beneficiary.

The Hierarchy of Succession

When directing the Principal Sum, the policyowner establishes a precise chain of succession. Insurance companies do not guess who should receive the money; they follow the named hierarchy strictly.

| Level | Designation | Definition & Trigger |

|---|---|---|

| 1st | Primary Beneficiary | The first person designated to receive the death benefit in an Accidental Death and Dismemberment policy. If they outlive the insured, they receive 100% of the funds. |

| 2nd | Contingent Beneficiary | The backup. A contingent beneficiary receives the policy death benefit only if the primary beneficiary dies before the insured. |

| 3rd | Tertiary Beneficiary | The final named backup. A tertiary beneficiary receives the policy death benefit only if both the primary and contingent beneficiaries die before the insured. |

| 4th | The Estate | If no named beneficiary is alive at the time of the insured's death, the death benefit is paid to the insured's estate, where it becomes subject to probate and creditors. |

Revocable vs. Irrevocable Designations

The policyowner’s right to change a beneficiary depends entirely on how the designation was initially drafted.

- Revocable Beneficiary: This is the standard designation. A revocable beneficiary designation allows the policyowner to change the beneficiary at any time without the beneficiary's consent.

- Irrevocable Beneficiary: This is a much rarer, heavier legal mechanism, often used in divorce settlements. An irrevocable beneficiary designation requires the current beneficiary's written consent before the policyowner can legally change the beneficiary.

By making a beneficiary irrevocable, the policyowner actually surrenders a portion of their absolute ownership rights. Because the irrevocable beneficiary now has a vested legal interest in the policy's value, a policyowner cannot borrow against a policy or assign a policy with an irrevocable beneficiary without the irrevocable beneficiary's written consent.

The Common Disaster and Simultaneous Death

Consider a scenario where a husband (the insured) names his wife as the primary beneficiary and his brother as the contingent beneficiary. The husband and wife are involved in a catastrophic car accident and both die at the scene. Who gets the money?

If the law assumed the wife survived her husband by even one minute, the death benefit would go to her estate (and her heirs). If the law assumed the husband survived the wife, the money would bypass her estate and go directly to his brother, the contingent beneficiary.

To solve this legal nightmare, the Uniform Simultaneous Death Act steps in.

The Uniform Simultaneous Death Act: A uniform law stating that if the insured and primary beneficiary die in the same accident, the law assumes the primary beneficiary died first.

This elegantly solves the common disaster problem. By legally declaring that the primary beneficiary died first, the primary beneficiary is effectively removed from the equation. The legal assumption that the primary beneficiary died first in a common disaster ensures the death benefit passes directly to the contingent beneficiary. This protects the policyowner's original intent and keeps the insurance proceeds out of probate court.

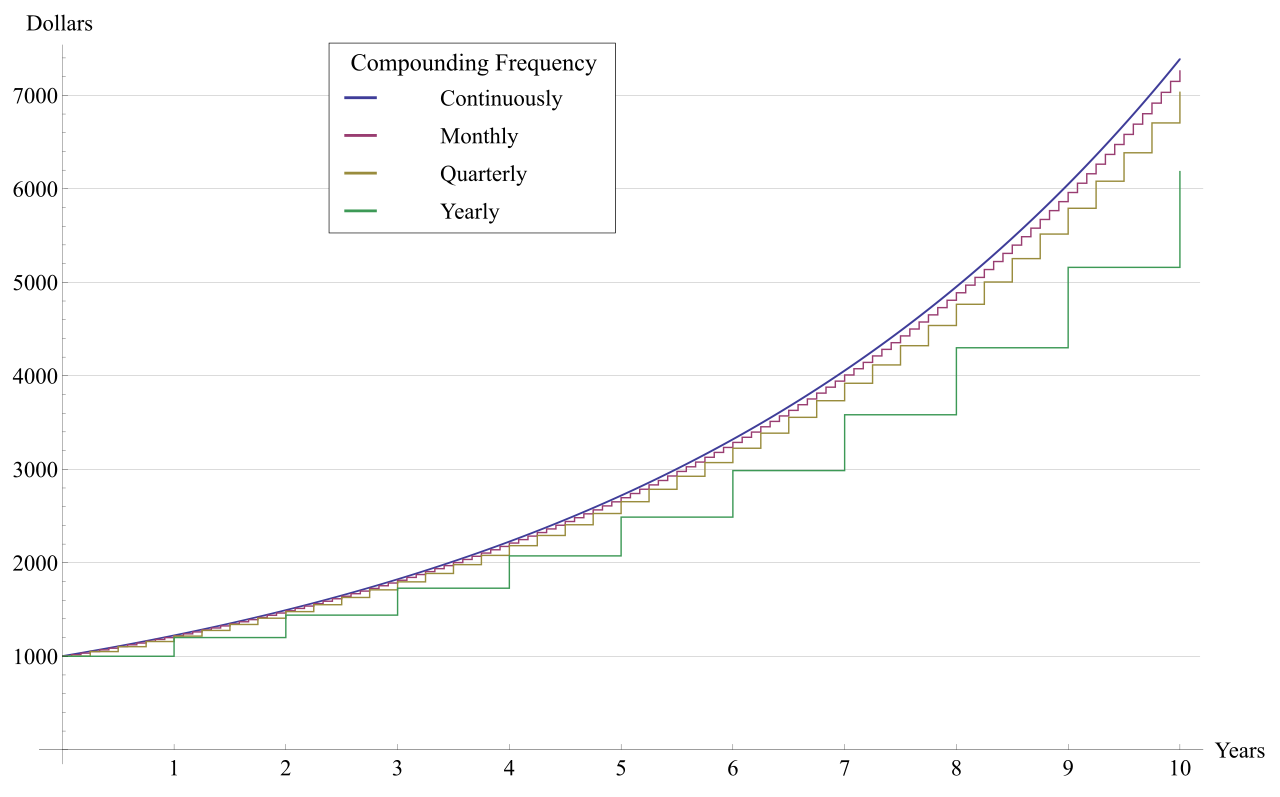

Insurance mathematically relies on the predictable inflow of capital. The way a policyowner chooses to fund their policy is called the premium mode. Simply put, the premium payment mode represents the frequency with which insurance policy premiums are paid.

Standard premium payment modes include annual, semi-annual, quarterly, and monthly options.

The Cost of Convenience

When a policyowner selects their premium mode, they are also selecting their final price point. While paying a small amount every month feels easier on a budget, paying health insurance premiums more frequently increases the total annual cost of the policy.

Why does an insurer penalize frequency? Two reasons:

- Administrative Overhead: Processing twelve monthly payments costs the insurer significantly more in banking fees and administrative labor than processing one annual payment.

- Lost Investment Capital: Insurers make their profit by investing premiums. If you pay annually, the insurer has your full premium to invest on day one. If you pay monthly, they lose out on eleven months of compound interest for the bulk of that money.

Therefore, insurers charge higher total annual premiums for frequent payment modes to cover additional administrative fees and loss of investment interest.

The mathematical rule is absolute:

- The annual premium payment mode results in the lowest overall cost for a health insurance policy.

- The monthly premium payment mode results in the highest overall annual cost for a health insurance policy.

Grace Periods by Premium Mode

Life is unpredictable, and payments are occasionally missed. A grace period is the mandatory window of time after a premium due date during which the policy remains actively in force, even though the premium has not been paid.

The length of a health insurance grace period is directly linked to the premium payment mode. The more frequently you pay, the shorter your grace period.

- The mandatory grace period for a health insurance policy with weekly premium payments is 7 days.

- The mandatory grace period for a health insurance policy with monthly premium payments is 10 days.

- The mandatory grace period for a health insurance policy with annual, semi-annual, or quarterly premium payments is 31 days.

Understanding these temporal boundaries allows you, as a producer, to accurately advise clients on how their cash flow decisions dictate both the cost and the vulnerability of their coverage.