Retirement Plans and Social Security Benefits

Every dollar a client earns is subject to the gravitational pull of taxation, and every year they live brings them closer to the cessation of their working income. The fundamental purpose of retirement planning—and the life insurance products that support it—is to dictate the terms on which these two forces operate. To accomplish this, the modern financial system uses a dual-layered architecture. The foundational layer is the mandatory, state-managed social safety net, while the secondary layer consists of private employer-sponsored plans structured around strict federal tax codes. For an insurance producer, understanding the mechanics of these two layers is not an academic exercise; it is the structural engineering required to build an effective financial plan, ensuring clients do not outlive their money or leave dependents financially exposed.

When you look at employer-sponsored retirement plans, you are essentially looking at a negotiation between businesses and the federal government. The government wants citizens to save for their own retirement so they do not become burdens on the state. To incentivize this, the government offers massive tax breaks. However, the government will only hand out those tax breaks if the employer plays by strict rules of fairness.

This dynamic creates two distinct categories of retirement plans: Qualified and Nonqualified.

Qualified Retirement Plans: The Public Park

Think of a qualified retirement plan as a public park subsidized by the city. Because it receives public tax benefits, everyone must be allowed to play, and the rules are strictly enforced.

To exist as a qualified plan, the arrangement must meet the federal guidelines of the Employee Retirement Income Security Act (ERISA). Furthermore, the Internal Revenue Service must approve a qualified retirement plan for the plan to receive favorable tax treatment.

Because of this IRS approval and ERISA compliance, qualified retirement plans are legally prohibited from discriminating in favor of highly compensated employees or executives. A business owner cannot set up a 401(k) purely for the C-suite; if the executives get to participate, the rank-and-file workers must be offered equitable participation.

In exchange for this egalitarian structure, the IRS grants phenomenal tax advantages:

- For the Employer: Employer contributions to a qualified retirement plan are tax-deductible as an ordinary business expense.

- For the Employee: Employee contributions to a qualified retirement plan are made with pre-tax dollars, lowering their taxable income for the year.

- For the Fund: Earnings within a qualified retirement plan grow on a tax-deferred basis until the funds are withdrawn. The friction of annual capital gains taxes is completely removed, allowing compound interest to work at maximum velocity.

However, the IRS does not let you shelter this money forever. To ensure this money is actually used for retirement, withdrawals from a qualified retirement plan prior to age 59 1/2 are generally subject to a 10 percent penalty tax. On the back end, you cannot simply leave the money untouched to pass onto your heirs tax-free. Qualified retirement plans require participants to take required minimum distributions (RMDs) starting at a specific age mandated by the Internal Revenue Service.

Nonqualified Retirement Plans: The VIP Lounge

Sometimes, an employer wants to discriminate. A company might want to offer a massive incentive to recruit a star CEO or retain top executives without having to offer the same proportionate benefit to all five hundred entry-level employees.

Enter the nonqualified plan. If the qualified plan is a public park, the nonqualified plan is a private VIP lounge.

Nonqualified retirement plans are not required to meet the federal guidelines of the Employee Retirement Income Security Act (ERISA), and they do not require formal approval from the Internal Revenue Service. Because they bypass ERISA, employers can legally design nonqualified retirement plans to exclusively benefit highly compensated executives. Deferred compensation plans and executive bonus plans are common examples of nonqualified retirement plans used as "golden handcuffs" to retain top talent.

But the IRS does not give away free lunches. By choosing to discriminate, the employer and the employee forfeit the upfront tax subsidies:

- For the Employee: Employee contributions to a nonqualified retirement plan are made with after-tax dollars.

- For the Employer: Employer contributions to a nonqualified retirement plan are not tax-deductible for the business until the employee actually receives the benefit (which could be decades later).

Despite the loss of upfront deductions, there is one shared benefit: earnings on contributions within a nonqualified retirement plan accumulate on a tax-deferred basis, still allowing for efficient compound growth.

| Feature | Qualified Plans | Nonqualified Plans |

|---|---|---|

| ERISA Compliance | Mandatory | Not Required |

| IRS Approval | Required for tax benefits | Not Required |

| Discrimination | Prohibited (must cover rank & file) | Permitted (can target executives) |

| Employee Contributions | Pre-tax | After-tax |

| Employer Deduction | Immediate (when contributed) | Delayed (when employee receives payout) |

While private plans are vital for wealth accumulation, the absolute floor of American retirement and mortality planning is Social Security. Formally known as Old-Age, Survivors, and Disability Insurance (OASDI), it is exactly what the name implies: an insurance system, not an investment account.

The Social Security system is funded through mandatory payroll taxes collected under the Federal Insurance Contributions Act (FICA). When you sit with a client and look at their pay stub, the FICA tax is the premium they are paying into this national insurance pool.

The Mathematics of the Benefit

How does the government determine what a worker gets out of the system? It operates on a points system based on an individual's lifetime earnings record.

Workers earn Social Security credits based on their annual earned income. No matter how wealthy a client is, a worker can earn a maximum of four Social Security credits in a single calendar year.

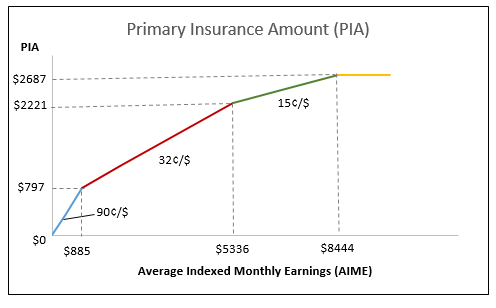

When it is time to calculate the actual monthly payout, a worker's Social Security benefits are based on the individual's Primary Insurance Amount (PIA). Think of the PIA as the baseline 100% payout figure. To find this number, the government looks backward: the Primary Insurance Amount (PIA) is calculated using a worker's Average Indexed Monthly Earnings (AIME) over their working lifetime. It indexes their historical wages for inflation, averages out the highest-earning 35 years, and applies a formula to spit out the PIA.

Insured Status: Fully vs. Currently

To claim benefits from OASDI, a worker must actually be "insured" by the system. Social Security recognizes two distinct tiers of insured status: Fully Insured and Currently Insured.

Fully Insured Status Think of fully insured status as completing a marathon. A worker achieves fully insured status under Social Security after accumulating 40 quarters of coverage (which translates to roughly 10 years of working and paying FICA taxes). Reaching this threshold unlocks the entire OASDI vault:

- Fully insured status qualifies a worker to receive Social Security retirement benefits.

- Fully insured status qualifies a deceased worker's eligible dependents for comprehensive Social Security survivor benefits.

Currently Insured Status What happens if a 26-year-old worker dies in a car accident? They have not worked for 10 years, so they do not have 40 credits. Does the system abandon their young family? No. The system has a "sprint" threshold for this exact tragedy.

Currently insured status requires a worker to have earned at least 6 Social Security credits during the 13-quarter period ending with the quarter of death. Because this is a much lower hurdle, currently insured status provides limited Social Security survivor benefits compared to fully insured status. Furthermore, currently insured status does not qualify a worker for Social Security retirement benefits—it exists strictly as a temporary safety net for young workers who die prematurely.

For a fully insured worker, retirement benefits are not a rigid switch; they are a dial that the worker can turn based on when they decide to stop working. The baseline payout is the Primary Insurance Amount (PIA), but when the worker claims it alters the math forever.

- Early Retirement: A worker can choose to begin receiving permanently reduced Social Security retirement benefits as early as age 62. The trade-off is severe; the monthly check is slashed to account for the extra years of payouts.

- The Baseline: Waiting until Full Retirement Age (FRA) allows a worker to receive 100 percent of their calculated Primary Insurance Amount (PIA).

- Delayed Retirement: The government incentivizes workers to keep contributing to the economy. Delaying Social Security retirement benefits past Full Retirement Age permanently increases the monthly benefit amount up to age 70.

As an insurance producer, your most vital application of Social Security knowledge will involve Survivor Benefits. When a breadwinner dies, Social Security steps in, but it leaves massive, terrifying gaps in income. Life insurance is mathematically designed to fill those specific gaps.

First, Social Security pays a one-time lump-sum death benefit of $255 to a qualifying surviving spouse or eligible child. (This amount has not changed in decades and barely covers the cost of floral arrangements at a modern funeral, making private life insurance critical).

Beyond the lump sum, who gets a monthly check if a fully insured worker dies?

- The Children: Social Security survivor benefits are available to an unmarried child of a deceased worker if the child is under age 18. Furthermore, if a child is severely disabled before age 22, the age 18 cutoff is waived—a surviving spouse caring for a severely disabled child of any age is eligible for Social Security survivor benefits.

- The Spouse (Childcare): Social Security survivor benefits are available to a surviving spouse caring for a deceased worker's child who is under age 16.

- The Spouse (Retirement): A surviving spouse is generally eligible to begin receiving reduced Social Security widow or widower benefits at age 60.

- The Parents: In a lesser-known provision, Social Security survivor benefits are available to dependent parents age 62 or older if the deceased worker provided at least half of the parents' financial support.

The Blackout Period: The Life Insurance Catalyst

If you look closely at the ages listed above, a glaring mathematical trap emerges for the surviving spouse.

The spouse receives a check while caring for a child, but only until that child turns 16. The spouse cannot claim their own widow/widower benefit until age 60.

What happens to the surviving spouse between the time the youngest child turns 16 and the spouse turns 60? Nothing.

The Social Security Blackout Period is the timeframe during which a surviving spouse is not eligible to receive any Social Security survivor benefits.

The mechanics are absolute:

- The Social Security blackout period begins when the youngest child of a deceased worker reaches age 16.

- The Social Security blackout period ends when the surviving spouse reaches age 60 and becomes eligible for widow or widower benefits.

If a 40-year-old widow's youngest child just turned 16, that widow is about to enter a 20-year income desert where OASDI provides zero financial support to them directly. This is the single most important concept to grasp when designing a life insurance plan for a young family. As a producer, you are not just selling a death benefit; you are bridging the Blackout Period, ensuring that a surviving spouse isn't forced to deplete the family's qualified and nonqualified retirement assets just to survive until age 60.