Life Policy Riders

Consider the engineering of a modern passenger aircraft. The basic airframe and engines guarantee flight, but it is the auxiliary systems—de-icing boots on the wings, redundant hydraulic lines, terrain-avoidance radars—that ensure the aircraft survives specific, localized threats. A standard life insurance contract functions much like that base airframe. It executes a straightforward, guaranteed transaction: premium in, death benefit out. Yet, a human life does not unfold in a predictable, straight line. People suffer debilitating injuries, inflation quietly erodes the purchasing power of money, and unexpected terminal illnesses threaten a family's financial stability long before death actually occurs. To adapt the rigid structure of a base policy to the unpredictable reality of a human life, the insurance industry relies on specialized, modular attachments called riders.

To understand how a life insurance policy operates in the real world, you must view it as a highly customizable contract.

A life insurance rider is an optional provision attached to a base policy to add or modify coverage.

Because transferring additional risk from the individual to the insurance company incurs a mathematical cost, adding a rider to a life insurance policy typically requires the policyowner to pay an additional premium. You are buying specific, targeted protection on top of the underlying death benefit.

As an insurance producer, your job is not merely to sell a base policy, but to architect a contract that anticipates your client's most critical vulnerabilities. We categorize these tools into four functional groups: protecting the premium stream, future-proofing the coverage, accelerating the benefit while alive, and modifying terms for accidents.

A life insurance policy is only valid if the premiums are paid. If your client is in a severe car crash and loses their ability to earn a living, the very policy designed to protect their family might lapse due to unpaid premiums. We solve this actuarial paradox with disability-focused riders.

The Waiver of Premium Rider

The waiver of premium rider is arguably the most fundamental modification you can attach to a policy. It exempts the policyowner from paying premiums if the insured becomes totally disabled.

However, insurance companies require proof that the disability is permanent, not just a temporary bout of the flu. Therefore, the waiver of premium rider usually includes a waiting period of six months before the premium waiver takes effect. The policyowner must continue paying premiums during this time.

If the insured remains totally disabled after the six-month waiting period, the insurer retroactively waives the premium and refunds the premiums paid during those six months.

- Impact on Cash Value: This is a vital point for the exam—premiums waived under a waiver of premium rider do not reduce the cash value accumulation of the policy. The insurer essentially pays the premium on the insured's behalf, meaning dividends and cash value continue to grow exactly as if the policyowner were writing the checks.

- Expiration: The risk of disability naturally climbs as we age. To contain costs, the waiver of premium rider typically expires when the insured reaches age 60 or 65. If they become disabled after this age, the premiums are not waived.

The Waiver of Monthly Deductions Rider

If your client owns a whole life policy, they pay a fixed premium. But what if they own a Universal Life policy, where premiums are flexible? You cannot "waive" a flexible premium, because there is no required fixed amount.

Instead, Universal Life policies utilize a waiver of monthly deductions rider. Rather than paying a fixed premium into the policy, this rider pays the exact mortality and expense costs for a disabled insured on a Universal Life insurance policy, preventing the policy from lapsing while the insured cannot work.

The Payor Benefit Rider

Suppose a grandparent buys a policy on a newborn child. If the grandparent dies, the infant obviously cannot pay the premium. The payor benefit rider is specifically designed for juvenile life insurance policies.

This rider waives policy premiums if the adult premium payor dies or becomes totally disabled. The payor benefit rider usually waives premiums until the insured child reaches a financially independent age—typically age 21 or 25—at which point the adult child assumes responsibility for the premiums.

As time passes, a client's financial liabilities grow. A death benefit that seemed immense to a 25-year-old might be completely inadequate for a 35-year-old with a mortgage and three children.

Guaranteed Insurability Rider

Imagine developing a chronic heart condition at age 30. You suddenly realize you need more life insurance, but no underwriter will approve you. The guaranteed insurability rider eliminates this trap. It allows the policyowner to purchase additional life insurance without providing evidence of insurability.

The insurer manages this immense risk by strictly controlling when you can buy the additional coverage:

- Specific Dates/Ages: Additional coverage under a guaranteed insurability rider can only be purchased on specific dates or at specific ages (e.g., every 3 years starting at age 25).

- Life Events: Major life changes instantly trigger a need for more coverage. Life events such as marriage or the birth of a child create a special option date under the guaranteed insurability rider, allowing an immediate purchase of more coverage.

When the client exercises this option, the premium for the additional coverage purchased under a guaranteed insurability rider is based on the insured's attained age at the time of purchase. Because the statistical likelihood of developing life-threatening conditions skyrockets in middle age, the guaranteed insurability rider typically expires when the insured reaches age 40.

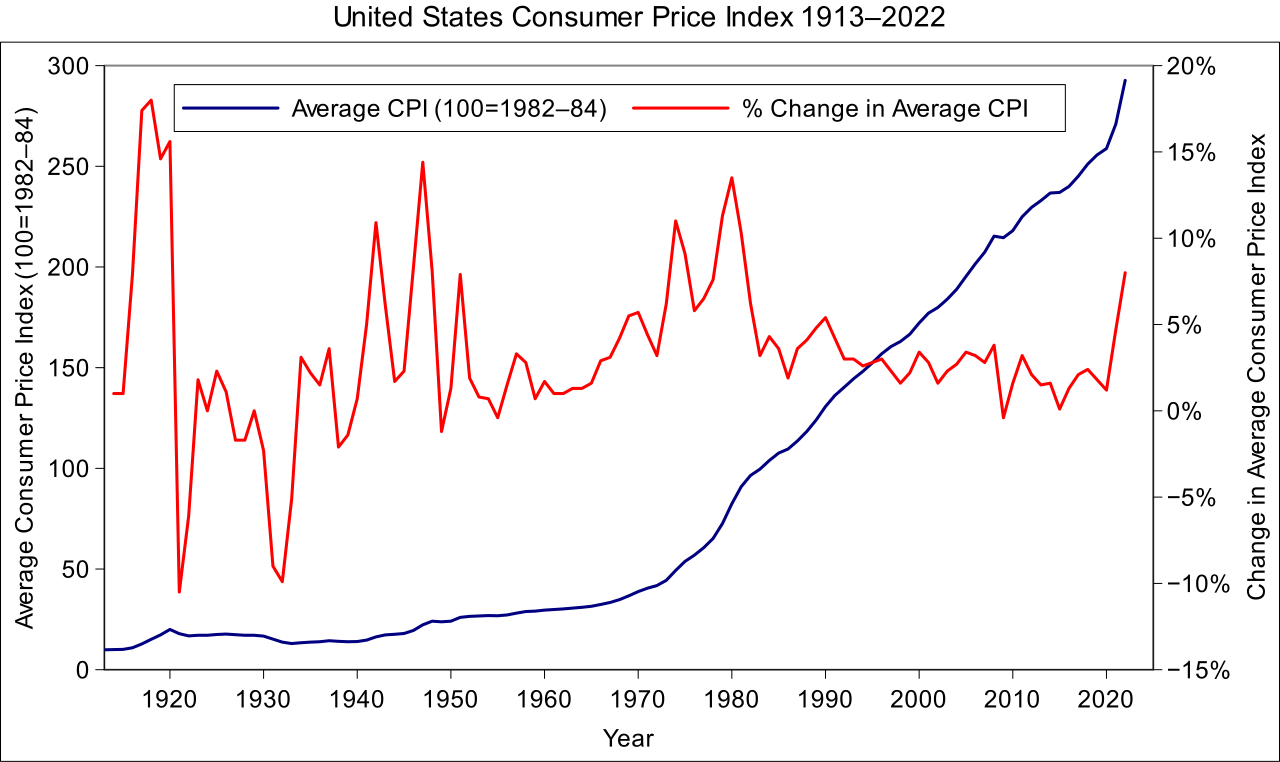

Cost of Living Rider

A $500,000 death benefit purchased in 1990 is worth significantly less in purchasing power today. The cost of living rider increases the policy death benefit annually to offset inflation.

To ensure the increase is objective, the cost of living rider typically ties the death benefit increase to the Consumer Price Index (CPI).

Because the insurance company is taking on greater risk each year, the policyowner must pay an additional premium for the increased death benefit provided by the cost of living rider. However, a cost of living rider provides this increasing death benefit coverage without requiring the insured to prove insurability, ensuring inflation protection regardless of their declining health.

Historically, life insurance only paid out upon death. Today, a suite of living benefit riders allows policyowners to access their death benefit early to manage catastrophic late-in-life expenses.

Accelerated Death Benefit Rider

If a doctor tells a client they have six months to live, the financial burden of end-of-life care can bankrupt their family before the death benefit ever pays out. The accelerated death benefit rider allows early payment of a portion of the death benefit if the insured is diagnosed with a terminal illness.

Terminal Illness Definition: For exam purposes, a terminal illness under an accelerated death benefit rider is typically defined as a condition expected to result in death within one to two years.

Long-Term Care (LTC) Rider

With modern medicine, people are surviving illnesses that used to be fatal, only to require years of assisted living. The long-term care rider allows the policyowner to access a portion of the death benefit early to pay for nursing home or home health care.

To prevent abuse, this rider requires a specific medical trigger. To trigger a long-term care rider, the insured must typically be:

- Unable to perform at least two activities of daily living (ADLs)—such as bathing, dressing, eating, or transferring.

- OR, experiencing severe cognitive impairment (such as Alzheimer's or dementia) which can also trigger the benefit payments of a long-term care rider.

The Golden Rule of Early Access: Whether a client utilizes the Accelerated Death Benefit or the Long-Term Care rider, the underlying mathematics are identical. Receiving an accelerated death benefit directly reduces the ultimate death benefit paid to the policy beneficiary upon the insured's death. Similarly, funds paid out to the insured under a long-term care rider directly reduce the final death benefit payable to the beneficiaries. You are simply emptying the bucket before you die; you do not get a second bucket.

Finally, there are riders that either multiply the payout under specific violent circumstances or alter the fundamental outcome of a term policy.

Accidental Death Benefit Rider

The accidental death benefit rider pays an additional sum if the insured dies as the direct result of an accident (often doubling the payout, colloquially known as "double indemnity").

Insurance companies are highly precise about the definition of an accident:

- Exclusions: The accidental death benefit rider does not pay an additional sum for deaths resulting from illness or disease. If a heart attack causes a driver to crash their car and die, the proximate cause of death was illness, not an accident. The base policy pays out, but the rider does not.

- Time Limit: To qualify for an accidental death benefit payout, the insured must typically die within 90 days of the triggering accident. This prevents disputes over whether an accident from three years ago caused a present-day death.

- Expiration: Like the waiver of premium, this rider becomes too risky for insurers as the client ages and becomes frail. The accidental death benefit rider normally expires when the insured reaches age 65.

Accidental Death and Dismemberment (AD&D) Rider

While the rider above only triggers upon death, the AD&D rider offers a two-tiered safety net:

| Payout Type | Triggered By | Amount Paid |

|---|---|---|

| Principal Sum | Accidental Death | 100% of the rider's face value. |

| Capital Sum | Accidental loss of limbs or eyesight | Typically 50 percent of the principal sum. |

Think of it logically: "Principal" refers to the ultimate loss (death), whereas "Capital" is a partial payout for the severe impairment of the insured's physical capabilities.

Return of Premium Rider

Term life insurance is like renting an apartment: it is cheap, but when the term is over, you walk away with zero equity. Some clients despise the idea of "wasting" their premiums if they don't die.

Enter the return of premium rider, which refunds all premiums paid if the insured outlives the specified term of a term life insurance policy.

How does the insurance company pull off this magic trick? They aren't doing it for free. A return of premium rider functions by attaching an increasing term insurance rider to the base policy. You are paying a significantly higher premium from day one, which buys an increasing block of coverage precisely matched to equal your total premiums paid. If you survive, that rider matures and pays you back.

Because you are simply being handed back your own after-tax money that you overpaid throughout the term, the premiums refunded by a return of premium rider are distributed to the policyowner tax-free. It is a return of principal, not an investment gain.

Summary for the Producer: Every rider represents a specific actuarial problem solved by a specific contractual tool. When you sit across the table from a healthy 30-year-old, you aren't just looking at a base policy. You are looking at a future that might include disability (Waiver of Premium), inflation (Cost of Living), the birth of a child (Guaranteed Insurability), or a severe accident (AD&D). Understanding these modular attachments is the difference between selling a generic policy and architecting a comprehensive financial shield.