Privacy, Consumer Protection, and Federal Compliance

When a client sits across from your desk to insure their home or business, they are handing you the keys to two entirely different structures. The first is physical—the bricks, mortar, and inventory they rely on you to protect from fire, wind, and liability. The second is invisible—a highly sensitive vault of personal data and a direct conduit into the United States financial system.

Federal regulation intersects with state insurance law precisely because a compromised data vault or a polluted financial stream can destroy a consumer's life or destabilize the national economy just as swiftly as a catastrophic natural disaster. To be an effective, legally compliant insurance producer, you must understand how to protect consumer privacy, recognize the footprints of financial crime, guard the solvency of the insurers you represent, and understand how the federal government backstops risks too massive for the private market to bear alone.

Insurance underwriting relies heavily on data. To price a risk accurately, an insurer needs to know who they are insuring. However, collecting a consumer's financial and personal data carries an immense regulatory responsibility. Two major federal laws govern this arena: the Fair Credit Reporting Act (FCRA) and the Gramm-Leach-Bliley Act (GLBA).

The Fair Credit Reporting Act (FCRA)

Credit history is statistically proven to correlate with insurance losses, making it a critical underwriting tool. The Fair Credit Reporting Act regulates the collection, dissemination, and use of consumer credit information. Its fundamental purpose is to ensure that consumer reporting agencies exercise their responsibilities with fairness, impartiality, and respect for the consumer's right to privacy.

Because credit reports dictate what a consumer pays for insurance, the FCRA demands absolute transparency from you, the producer.

- The Advance Notice: An insurance company must inform an applicant in advance that a consumer credit report may be requested as part of the underwriting process.

- The Notice of Information Practices: As an insurance producer, you must provide an applicant with a Notice of Information Practices when collecting personal information for an insurance application. This establishes exactly what information you are gathering and how it will be used.

When the Data Hurts the Consumer: Adverse Action

If a consumer's credit report negatively impacts their insurance application, they have a right to know. An adverse action notice must be provided to a consumer if an insurance company denies coverage based on information found in a consumer credit report. Furthermore, an adverse action notice must be provided to a consumer if an insurance company increases premiums based on information found in a consumer credit report.

This notice is not just a simple rejection letter. Under federal law, an adverse action notice must include the name, address, and toll-free telephone number of the reporting agency that supplied the consumer credit report.

The Consumer's Right to Fight Back If a client receives an adverse action notice, the FCRA arms them with specific rights to ensure fairness:

- Consumers have the right to request a free copy of their credit report from the consumer reporting agency if subjected to an adverse action.

- Consumers have the right to dispute incomplete or inaccurate information found in their consumer credit report.

- Consumer reporting agencies are legally required to investigate disputed credit information reported by a consumer.

Because consumer data is so powerful, accessing it unlawfully is heavily punished. A person who knowingly obtains a consumer credit report under false pretenses is subject to federal criminal fines and imprisonment.

The Gramm-Leach-Bliley Act (GLBA)

While the FCRA governs pulling credit reports to make decisions, the GLBA governs how you protect and share the data you already have. Under the GLBA, nonpublic personal information includes any personally identifiable financial information provided by a consumer to a financial institution.

The GLBA rests on two pillars: Disclosure and Security.

- Security: The Gramm-Leach-Bliley Act requires financial institutions to implement security programs to safeguard sensitive consumer data from hackers, breaches, or physical theft.

- Disclosure: The Gramm-Leach-Bliley Act requires financial institutions to fully disclose their information-sharing practices to their customers.

When you onboard a new client, you must follow strict timing and content rules for privacy notices. Under the Gramm-Leach-Bliley Act, an insurer must provide a clear privacy notice to a consumer at the time a customer relationship is established. This isn't a one-and-done requirement; an insurer must provide an updated privacy notice to all policyholders at least once per year.

A compliant GLBA privacy notice must explicitly detail what nonpublic personal information the insurer collects about the consumer. It must also explicitly identify the types of affiliated and nonaffiliated third parties with whom the insurer shares consumer information.

Crucially, consumers control their data. The Gramm-Leach-Bliley Act gives consumers the right to opt out of having their nonpublic personal information shared with nonaffiliated third parties. To make this reality, an insurer must provide a consumer with a reasonable and simple method to exercise the opt-out right regarding information sharing (e.g., a toll-free number or a prepaid opt-out mailer).

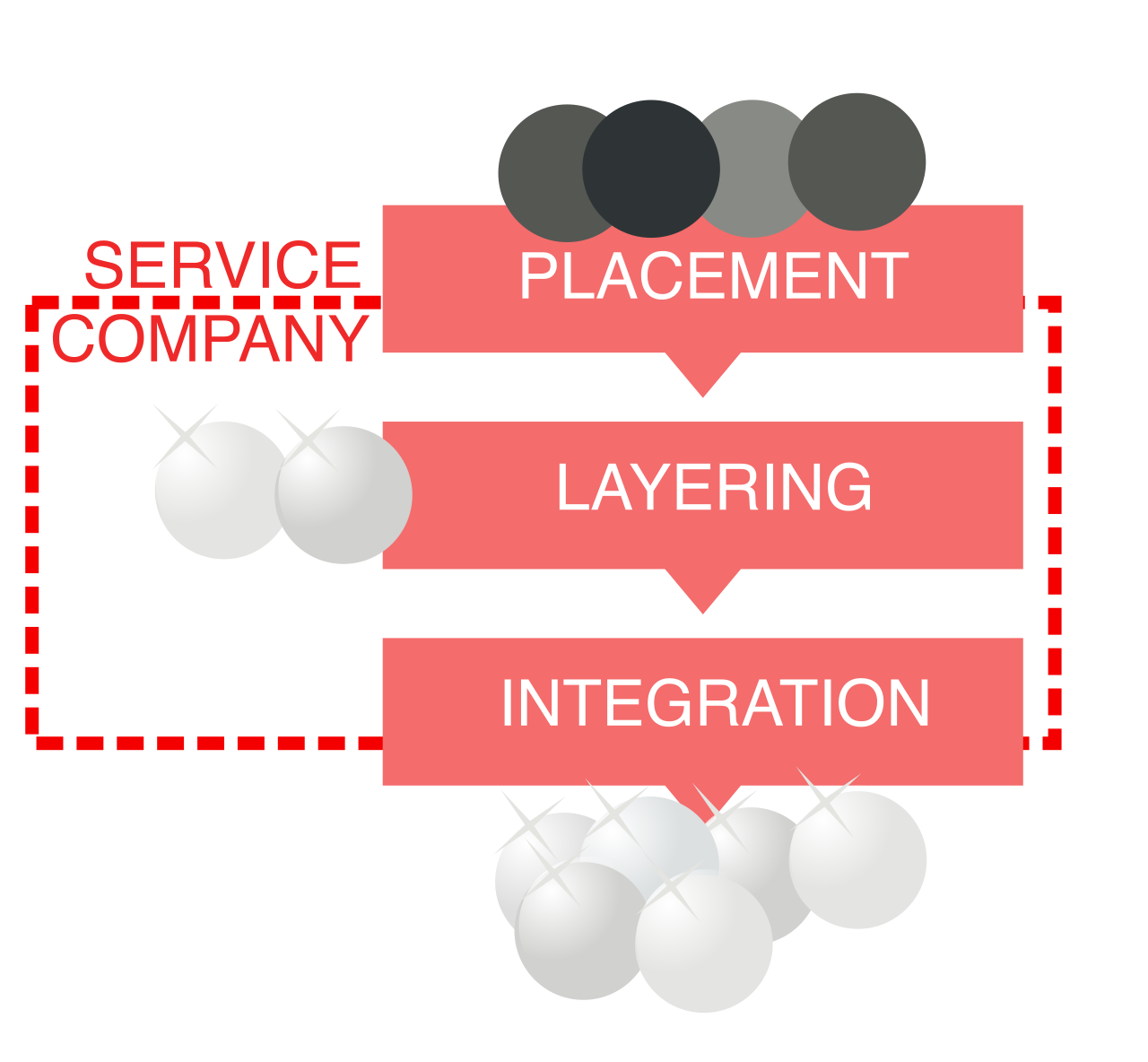

An insurance policy is a financial instrument, and like any financial instrument, it can be abused by bad actors seeking to wash dirty money.

Money laundering is the illegal process of concealing the origins of illegally obtained money by passing the money through a complex sequence of banking or commercial transfers. To combat this, Congress expanded federal oversight over the financial sector through the USA PATRIOT Act.

A primary objective of the USA PATRIOT Act is to detect and deter the funding of domestic and international terrorist organizations. To achieve this, the USA PATRIOT Act requires financial institutions to establish and maintain anti-money laundering programs.

Detecting the Red Flags

Because criminals constantly evolve their tactics, static rules are not enough. Therefore, insurance companies are required to implement ongoing training programs to teach employees how to recognize red flags indicative of money laundering—such as a client overpaying a massive premium on a commercial property policy only to cancel it weeks later and request a refund check from the insurer.

When you spot something illicit, you are legally bound to report it.

- Suspicious Activity Reports (SAR): Insurance companies must file a Suspicious Activity Report with the federal government for transactions that indicate potential money laundering or illegal activity.

- The "No Tipping" Rule: Federal law strictly prohibits insurance companies from informing a client that a Suspicious Activity Report has been filed regarding the client's transactions. Tipping off a criminal allows them to flee or destroy evidence.

Cash Transactions and Structuring

Cash leaves no digital footprint, making it the lifeblood of illicit finance. Consequently, an insurance professional must report the receipt of more than $10,000 in cash or cash equivalents for a single transaction to the Financial Crimes Enforcement Network (FinCEN).

Criminals know about this threshold and often try to circumvent it. Structuring is the illegal practice of breaking up a large cash transaction into multiple smaller amounts to evade mandatory federal reporting requirements. If a client attempts to pay a $12,000 premium using three successive cash payments of $4,000 on three different days, this is structuring—and it is a massive red flag.

An insurance policy is nothing more than a promise on a piece of paper. If the insurance company is hollowed out by internal fraud, that promise is worthless, and catastrophic public harm follows. To protect the public, 18 U.S.C. Section 1033 establishes fierce federal penalties for fraud and restricts who is permitted to work within the insurance business.

Guarding the Vault

Under Section 1033, federal insurance fraud that severely jeopardizes the safety and soundness of an insurer is punishable by up to 15 years in federal prison.

Specifically, federal law under 18 U.S.C. Section 1033 makes it a crime for any person in the insurance business to make false material statements regarding the financial condition of an insurer. Furthermore, any person engaged in the insurance business who intentionally embezzles funds from an insurer commits a federal felony under 18 U.S.C. Section 1033.

The Section 1033 Waiver

Because honesty is the foundational bedrock of the insurance contract, federal law places strict guardrails on industry employment. It is a federal offense for an individual with a felony conviction involving dishonesty to engage in the business of insurance without prior written consent from a state regulator.

If a prospective agent has a tainted past, they cannot simply quietly apply for a job. An individual with a felony conviction for a breach of trust must successfully obtain a Section 1033 waiver to legally work in the insurance industry.

What is a 1033 Waiver? A Section 1033 waiver is a formal written consent document issued by an authorized state insurance regulator. It operates as official permission for a convicted felon to work in the industry despite their record.

The burden of compliance does not just fall on the individual; the agency or carrier is also on the hook. An insurance company commits a federal offense if it knowingly employs an individual who possesses an unpardoned felony conviction for dishonesty without a valid Section 1033 waiver.

Insurance relies on the "Law of Large Numbers" to predict accidental, naturally occurring losses over time. Acts of war or terrorism defy these statistical laws. They are intentional, geographically concentrated, and capable of inflicting financially ruinous damage that private insurers simply do not have the capital to absorb.

Following the attacks of September 11, 2001, reinsurers abandoned the terrorism market, leaving businesses dangerously exposed. Congress intervened. The Terrorism Risk Insurance Act (TRIA) established a temporary federal program to share the financial risk of loss from certified foreign and domestic terrorist attacks.

TRIA Requirements and Scope

Under TRIA, the federal government acts as a massive reinsurer of last resort, but only for the commercial sector.

- The Mandate: The Terrorism Risk Insurance Act requires all commercial property and casualty insurers to offer terrorism coverage to their commercial policyholders.

- The Exemption: The Terrorism Risk Insurance Act does not mandate the offering of terrorism coverage for personal lines of insurance such as personal auto or homeowners policies.

- The Disclosure: Because it must be offered, commercial policyholders must be given clear, written disclosure of the specific premium amount charged for coverage under the Terrorism Risk Insurance Act.

The Anatomy of a "Certified" Act

A catastrophic explosion at a commercial facility is not automatically covered by TRIA. For a catastrophic event to trigger federal backstop coverage, the event must be officially certified as an act of terrorism by the Secretary of the Treasury.

The Secretary of the Treasury does not make this determination in a vacuum. By law, the Secretary of Homeland Security and the Attorney General of the United States must concur with the Secretary of the Treasury to certify an event as an act of terrorism.

| TRIA Certification Criteria | Description |

|---|---|

| Nature of the Act | An act of terrorism under the Terrorism Risk Insurance Act must involve violent acts or acts that are dangerous to human life, property, or infrastructure within the United States. |

| Financial Threshold | The Terrorism Risk Insurance Act requires an event to cause at least $5 million in aggregate property and casualty insurance losses to be certified as an act of terrorism. |

The Ultimate Ceiling: The $100 Billion Cap

Even the federal government has a budget. To ensure the financial survival of the nation in the face of an apocalyptic event, TRIA contains a built-in mathematical ceiling. The Terrorism Risk Insurance Act establishes a strict cap on total annual liability for certified acts of terrorism at $100 billion.

If the unthinkable happens and total insured losses skyrocket past that mark, the law is absolute: if the $100 billion annual cap under the Terrorism Risk Insurance Act is met, neither the federal government nor the insurers are liable for any portion of losses that exceed the cap. Prorated formulas dictate how the $100 billion is divided, but beyond that threshold, the insurance mechanism stops.

Understanding these federal parameters separates a mere salesperson from a true insurance professional. As you step into your role as a P&C producer, remember that every application you take, every disclosure you provide, and every premium check you accept is governed by these foundational federal laws, working quietly in the background to stabilize both the consumer's life and the American economy.