Auto and Property Regulatory Concepts

At its core, the modern insurance market is an ecosystem built on trust, predictability, and the statistical pooling of risk. But what happens when that trust is broken, or when a risk becomes statistically uninsurable in the private market? If an individual drives a two-ton vehicle at highway speeds without the means to pay for the damage they cause, or if a coastal town becomes entirely uninsurable due to hurricanes, the economic ecosystem collapses. Insurance regulation is not merely a collection of bureaucratic hurdles; it is the structural foundation that ensures systemic stability and public protection. We are examining the safety nets built beneath the primary safety nets—the mechanisms states use to force accountability and provide coverage when the standard market fails.

Every time an individual puts a key into an ignition, they are assuming a profound liability. State governments regulate this liability through two primary, intertwined legal frameworks.

Compulsory auto insurance laws dictate that vehicle owners must purchase liability insurance before legally driving a vehicle. This is a preventative measure. In contrast, financial responsibility laws require a driver to prove the ability to pay for damages after an auto accident.

For the vast majority of consumers, purchasing an auto liability insurance policy satisfies state financial responsibility requirements. However, a liability policy is not the only way to satisfy the law. Financial responsibility can often be demonstrated by depositing cash with the state motor vehicle department or by posting a surety bond with the state. Regardless of the method, the consequences for failing to meet these mandates are severe. Failing to maintain compulsory auto insurance can result in the suspension of a driver license and the revocation of a vehicle registration.

High-Risk Accountability: The SR-22

When a driver commits severe infractions—such as driving under the influence or driving without insurance—the state demands tighter supervision. This is where the SR-22 comes into play.

A common misconception is that an SR-22 is a type of insurance policy. It is not. An SR-22 is a certificate of financial responsibility required for certain high-risk drivers. An SR-22 form proves a driver carries the mandatory minimum auto liability limits.

When a driver’s license is suspended due to major violations, a state department of motor vehicles requires an SR-22 form to reinstate a suspended driver license. The driver cannot simply hand this form to the DMV themselves; to prevent fraud, an insurer files an SR-22 directly with the state motor vehicle department. If the policy cancels, the insurer immediately notifies the DMV, and the license is swiftly suspended again.

Even with compulsory laws, there will always be individuals who drive illegally without coverage. State regulators address this reality by forcing insurers to offer specialized coverages to protect responsible drivers.

Insurers are mandated in many states to offer uninsured motorist (UM) coverage and underinsured motorist (UIM) coverage to all auto liability policyholders.

| Coverage Type | How It Functions |

|---|---|

| Uninsured Motorist (UM) | Compensates an insured when an at-fault driver lacks any liability insurance. Crucially, uninsured motorist coverage treats an unidentified hit-and-run driver as an uninsured driver. |

| Underinsured Motorist (UIM) | Pays the difference between the insured's damages and the at-fault driver's inadequate liability limits. (e.g., Your damages are $100,000, but the at-fault driver only carries $25,000 in liability limits). |

Because regulators want maximum protection for the public, these coverages are usually built into standard auto quotes by default. However, policyholders can legally reject uninsured motorist coverage in most jurisdictions. Because this removes a critical layer of financial protection, rejecting uninsured motorist coverage typically requires the named insured to sign a written waiver, proving they made an informed, active choice to decline the coverage.

The standard insurance environment is known as the voluntary market—insurers voluntarily accept risks that meet their underwriting criteria. But what happens to consumers who have too many accidents, or properties located in high-crime or wildfire-prone areas? Standard insurers will decline them.

Enter residual markets, which provide insurance to high-risk consumers unable to obtain standard coverage. Because these state-mandated programs exist to serve those who have been universally rejected, residual markets are often referred to as markets of last resort.

Auto Assigned Risk Plans

If a driver is legally required to carry insurance to get to work, but no standard insurer will write the policy, state governments intervene. State auto assigned risk plans distribute high-risk drivers among licensed auto insurers.

An insurer cannot simply opt out. To maintain fairness, an insurer accepts a portion of assigned risk auto policies proportionate to its total auto market share in that state. If an insurer writes 20% of the voluntary auto policies in a state, they are required to take on 20% of the assigned risk applicants.

In some states, rather than randomly assigning individual policies, regulators utilize a Joint Underwriting Association (JUA). A Joint Underwriting Association is a statutory organization creating a residual market for specific insurance lines. In a JUA, participating insurers pool their premiums and losses to provide coverage collectively, rather than taking on individual high-risk drivers one by one.

Property FAIR Plans

Property owners face similar dilemmas. To ensure urban and coastal residents can secure mortgages and protect their homes, states created FAIR plans. FAIR stands for Fair Access to Insurance Requirements.

FAIR plans provide basic property insurance to applicants unable to secure coverage in the voluntary market. All licensed property insurers in a state must participate in that state's FAIR plan, and losses experienced by a FAIR plan are shared proportionately among all participating property insurers.

However, FAIR plans are not a free pass for negligent homeowners.

FAIR Plan Gatekeeping Rules:

- Geographic Limitation: FAIR plan eligibility typically requires a property to be located in a designated geographic area.

- Market Exhaustion: FAIR plan applicants must demonstrate an unsuccessful attempt to obtain standard property insurance.

- Safety Requirements: Properties must meet basic safety standards to qualify for a FAIR plan. The state will provide a safety net, but it will not insure a guaranteed loss. Therefore, FAIR plans refuse coverage for properties with uncorrected physical hazards (e.g., a collapsing roof or faulty, exposed wiring).

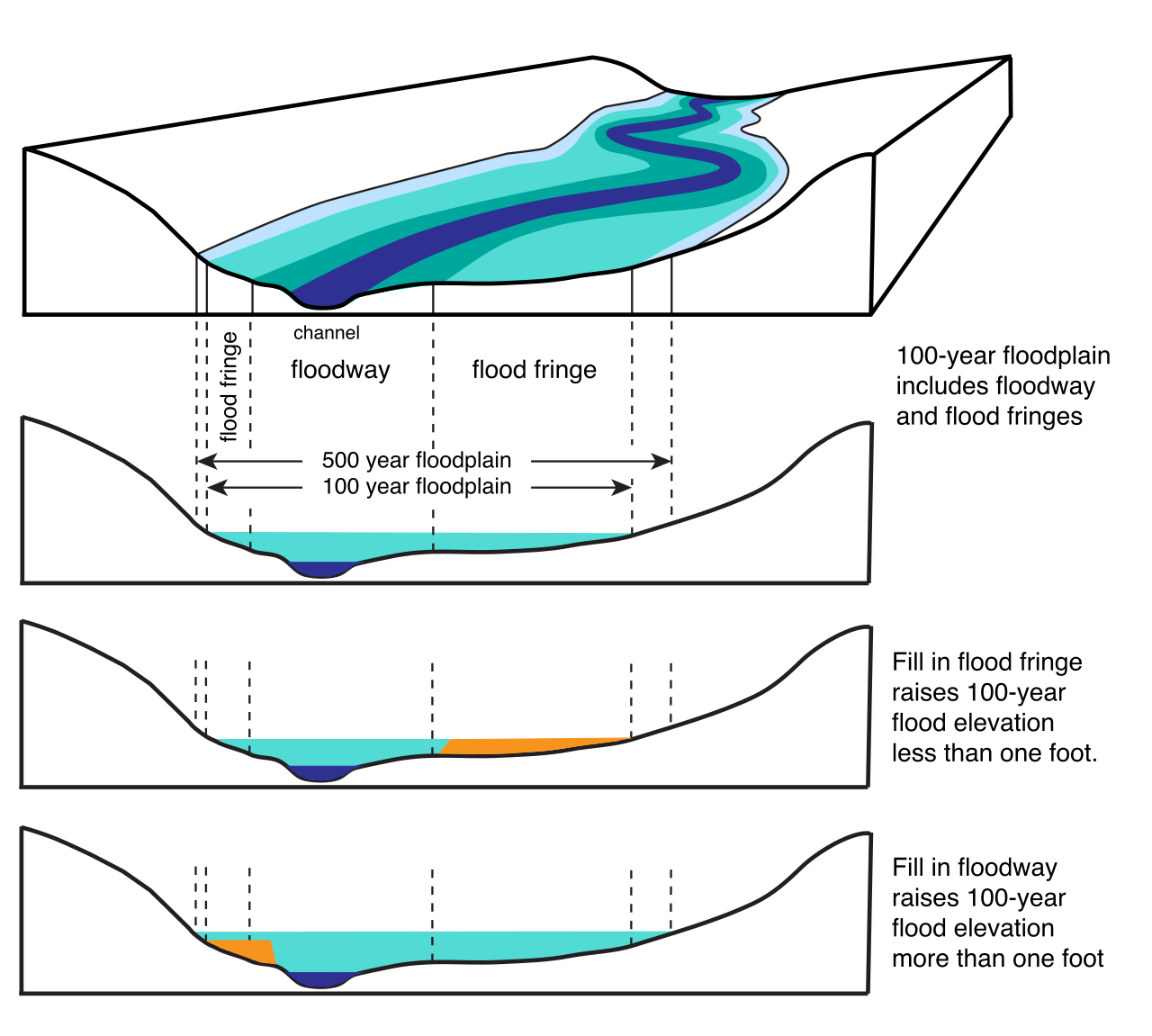

Private property insurers universally exclude flood damage from standard policies. Floods violate a fundamental law of insurability: they cause catastrophic, widespread losses affecting thousands of properties simultaneously. To solve this, the federal government stepped in.

The National Flood Insurance Program (NFIP) provides flood insurance to property owners in participating communities. It is critical to note that the National Flood Insurance Program is managed by the Federal Emergency Management Agency (FEMA), not by state insurance departments.

Because flood control is a communal effort, an individual cannot buy NFIP coverage if their town refuses to mitigate flood risks. A community must adopt approved floodplain management ordinances to participate in the National Flood Insurance Program.

The Write Your Own (WYO) Program

FEMA is a massive government agency, not an agile consumer-facing insurance brokerage. To handle the logistics of issuing millions of policies, FEMA created the Write Your Own (WYO) program.

Under this system, Write Your Own participating insurers sell National Flood Insurance Program policies directly to consumers, and these Write Your Own participating insurers service National Flood Insurance Program policies directly to consumers. If you buy flood insurance, your paperwork and claims adjusters will likely come from a familiar private insurance brand. However, this is essentially a "white-labeling" arrangement. The private insurers are merely administrative conduits; the federal government retains the actual underwriting risk for policies issued through the Write Your Own program.

Because insurance is a critical financial shield, insurers cannot simply revoke a policy on a whim. State regulators carefully monitor how and when an insurance contract can be severed. We must clearly distinguish between the two methods of severance:

- Cancellation is the termination of an insurance policy before the policy expiration date.

- Nonrenewal is the insurer's refusal to continue coverage after the current policy term expires.

The Right to Cancel

An insured has the right to cancel an insurance policy at any time. They do not need the insurer's permission.

In contrast, state insurance laws strictly limit an insurer's ability to cancel a property or casualty policy mid-term. To prevent consumers from abruptly losing coverage without cause, an insurer can cancel a policy mid-term only under severely restricted circumstances:

- An insurer can cancel a policy mid-term for nonpayment of premium.

- An insurer can cancel a policy mid-term if the insured commits fraud.

- An insurer can cancel a policy mid-term if the insured makes a material misrepresentation.

- An insurer can cancel a policy mid-term if a substantial increase in the insured hazard occurs.

The Discovery Period Exception: There is one brief window of leniency for insurers. An insurer has a specific discovery period at the beginning of a new policy to underwrite the risk (usually the first 60 days). An insurer can cancel a new policy for any valid underwriting reason during the initial discovery period.

Notice Requirements

You cannot cancel or nonrenew a policy in secret. Insurers must provide advance written notice to the insured before a mid-term cancellation takes effect, and insurers must provide advance written notice to the insured before nonrenewing an insurance policy.

State laws dictate the minimum number of days required for a cancellation notice and dictate the minimum number of days required for a nonrenewal notice. Because nonpayment of premium is a direct breach of contract by the insured, cancellation for nonpayment usually requires a very short notice (e.g., 10 days). However, state laws typically require more advance notice for a nonrenewal than for a cancellation due to nonpayment of premium (e.g., 30 to 60 days), giving the insured ample time to shop for a new policy.

Furthermore, these notices cannot be vague. A notice of cancellation must explicitly state the specific reason for terminating the policy, and a notice of nonrenewal must explicitly state the specific reason for refusing to renew the policy.

Premium Refunds: Pro-Rata vs. Short-Rate

When a policy is cancelled mid-term, unearned premiums must be returned. The method of calculation depends entirely on who initiated the cancellation.

| Cancellation Initiator | Refund Method | Rationale |

|---|---|---|

| Insurer Cancels | Pro-Rata Refund | An insurer cancelling a policy mid-term must provide a pro-rata premium refund to the insured. If exactly 50% of the policy term is left, the insured gets exactly 50% of their premium back. |

| Insured Cancels | Short-Rate Refund | An insured cancelling a policy mid-term typically receives a short-rate premium refund. A short-rate premium refund imposes a financial penalty on the insured for early cancellation. This penalty compensates the insurer for the non-refundable administrative overhead costs incurred when setting up the policy. |