Business Owners Policy (BOP) Liability Section

When a small enterprise opens its doors to the public, it simultaneously exposes itself to a mathematically staggering array of liability vectors. A delivery driver slips on a freshly mopped entryway; a competitor alleges a stolen marketing slogan; a defective product causes catastrophic property damage weeks after its purchase. The modern commercial apparatus requires a mechanism to transfer these predictable, localized risks away from the business's balance sheet. By automatically packaging commercial property and commercial liability coverages together into a single, indivisible contract, the Businessowners Policy (BOP) provides an elegant, highly efficient risk transfer vehicle strictly designed for eligible small to medium-sized low-risk businesses. Understanding the liability section of this policy is not simply an exercise in memorizing coverages—it is an exercise in mastering the financial physics that keep commercial enterprises solvent in a highly litigious environment.

At the heart of the Businessowners Policy liability section is a promise to shield the insured from the financial fallout of third-party claims. The policy structurally divides this protection into a few fundamental pillars of coverage.

First, the policy covers third-party bodily injury (when someone is physically hurt on the premises or by the business's operations) and third-party property damage (when the business inadvertently destroys or damages someone else's property).

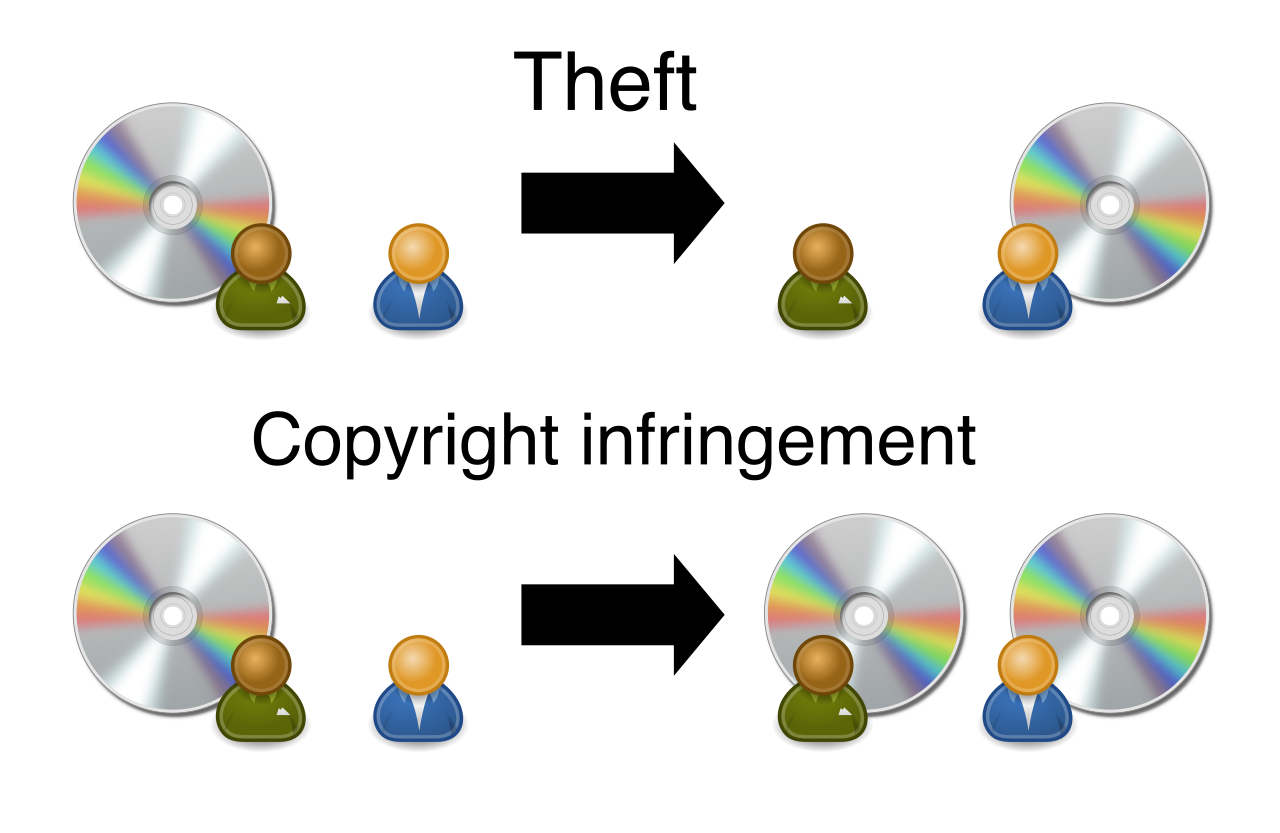

However, physical injury is only one dimension of commercial risk. The policy also covers personal and advertising injury offenses. This deals with the intangible harm a business can inflict while operating or promoting itself. Specifically, personal and advertising injury coverage includes protection against claims of libel (written defamation), slander (spoken defamation), and copyright infringement (using protected intellectual property in an advertisement without permission).

Why this matters for your clients: If a local bakery owner vents on a podcast that a rival bakery uses "rancid ingredients," they have just committed slander. If they use a local photographer’s image on their flyer without permission, that is copyright infringement. The BOP’s personal and advertising injury provision is the structural net that catches these everyday entrepreneurial mistakes.

In addition to traditional liability, the Businessowners Policy liability section includes Medical Expenses coverage for third parties. Think of this as the "goodwill" clause of the insurance contract.

Businessowners Policy Medical Expenses coverage pays for necessary medical care regardless of fault. If a customer trips over their own shoelaces in the insured's store and breaks a wrist, the policy will pay the medical bills even though the business did nothing wrong. The underlying logic here is preventative: covering minor medical bills promptly without a legal battle often prevents a frustrated customer from hiring an attorney and filing a massive bodily injury lawsuit.

To trigger this coverage, the policy enforces a strict timeline constraint: Businessowners Policy Medical Expenses coverage requires the medical expenses to be both incurred within one year of the accident and reported within one year of the accident.

Because this coverage is meant specifically for third-party guests and customers, it applies strict boundaries. Businessowners Policy Medical Expenses coverage excludes:

- Bodily injury to the named insured.

- Bodily injury to the insured's employees (who must look to Workers Compensation).

- Bodily injury to tenants of the insured's premises (who should carry their own insurance).

Note: The one-year validity window for Medical Payments is an industry standard; both Businessowners Policies and Commercial General Liability policies provide Medical Payments coverage valid for one year from the date of the accident.

When an insured is sued, the financial bleeding begins long before a judge issues a verdict. Attorneys bill by the hour, and legal discovery is exhaustingly expensive. Consequently, the Businessowners Policy liability section promises to defend the insured against covered suits.

Crucially, both Businessowners Policies and Commercial General Liability policies provide defense costs outside of the policy limits. This means the insurer can spend $1 million on lawyers to defend a claim without draining a single dollar from the insured's actual limit of liability coverage. However, this protection is not infinite. The insurance company's duty to defend ends immediately when the applicable Businessowners Policy limit of insurance has been exhausted by the payment of judgments or settlements.

Beyond standard legal fees, Businessowners Policy Supplementary Payments are provided in addition to the policy limits. If a covered lawsuit forces the insured to incur peripheral costs, these payments act as a vital buffer. Supplementary Payments cover:

- The cost of bail bonds required because of covered accidents (such as an employee causing a traffic accident resulting in a violation).

- The insured's loss of earnings up to $250 per day for time taken off work to assist the insurance company in the investigation or defense of the claim.

- Pre-judgment interest awarded against the insured.

- Post-judgment interest awarded against the insured while an appeal is pending or before the judgment is paid.

Liability policies utilize a system of interlocking limits to cap the insurer's total exposure. Under a BOP, these limits are stacked hierarchically.

The fundamental building block is the Liability and Medical Expenses limit, which is a combined single limit per occurrence. This single bucket of money caps the payout for all bodily injury, property damage, and medical expenses arising from one single occurrence.

Beneath that umbrella sits the Medical Expenses limit, which operates on a per-person basis. If five people are injured in a store collapse, each person’s medical payments are capped by this per-person limit, and the sum total of those payments is subject to the overall Liability and Medical Expenses per-occurrence limit.

To prevent an accumulation of claims from draining an insurer over a year, the policy also utilizes aggregate limits—caps on the total amount paid during the entire 12-month policy period.

- The General Aggregate Limit: This caps the total amount paid during the policy period for standard premises and operations claims (e.g., slip-and-falls in the store). The General Aggregate Limit is typically twice the Liability and Medical Expenses occurrence limit.

- The Products-Completed Operations Aggregate Limit: The General Aggregate Limit does not apply to claims falling under the products-completed operations hazard (e.g., food poisoning from a sold pastry, or a deck collapsing weeks after a contractor finished building it). Instead, the Businessowners Policy includes a distinct Products-Completed Operations Aggregate Limit, which is also typically twice the Liability and Medical Expenses occurrence limit.

Finally, the policy addresses real estate fire risk. The Businessowners Policy includes a Damage to Premises Rented to You limit, which applies on a per-fire basis. If the insured leases a retail space and negligently leaves a space heater on, causing a fire that guts the building, this specific limit covers the fire damage to the leased premises caused by the insured's negligence.

No insurance policy covers everything. A critical part of mastering the BOP is knowing exactly where the coverage stops.

The Territorial Boundary

Businessowners Policy liability coverage applies only to occurrences taking place within the standard policy territory. This territory is geographically confined; the standard policy territory for a Businessowners Policy includes the United States and its territories, Puerto Rico, and Canada. If your insured operates a pop-up shop in Paris or Tokyo, standard BOP liability will not respond to claims arising there.

The Operational Exclusions

The standard Businessowners Policy liability section heavily restricts high-risk or separately-insured hazards:

- Workers Compensation: The BOP liability section completely excludes Workers Compensation obligations. Employees injured on the job are entirely outside the scope of this policy.

- Intentional Acts: Both Businessowners Policies and Commercial General Liability policies strictly exclude liability for expected or intended injuries.

- Professional Services: The policy excludes damages arising from the rendering of professional services. A pharmacist making an error in filling a prescription or an architect drawing faulty blueprints needs separate Professional Liability (Errors & Omissions) insurance.

- Pollution: A Businessowners Policy incorporates pollution exclusions similar to those found in a Commercial General Liability policy. Toxic spills or slow environmental leaks are largely carved out.

- Liquor Liability: The policy excludes liquor liability entirely only for insureds in the business of manufacturing or selling alcoholic beverages (like bars or breweries). However, host liquor liability is covered under a Businessowners Policy for insureds who are not in the alcoholic beverage business. If an accounting firm hosts a holiday party and serves wine, they are protected if an inebriated guest causes an accident.

Vehicles and Vessels

Because autos and large vehicles present massive, distinct liability profiles, the Businessowners Policy liability section excludes bodily injury arising out of the ownership or use of aircraft. Similarly, it excludes bodily injury arising out of the ownership or use of most watercraft.

There is one notable exception to the marine exclusion: The policy does cover liability arising from the use of non-owned watercraft less than 51 feet long.

For the state licensing exam, you must clearly distinguish the Businessowners Policy (BOP) from a Commercial General Liability (CGL) policy. While they share similar DNA—and practically identical policy language regarding general liability—their application in the marketplace is fundamentally different.

| Feature | Businessowners Policy (BOP) | Commercial General Liability (CGL) |

|---|---|---|

| Policy Structure | Automatically packages commercial property and commercial liability coverages together. | A standard CGL policy provides standalone liability coverage without built-in property protection. |

| Target Market | Strictly designed for eligible small to medium-sized low-risk businesses. | Can accommodate large enterprises and businesses with high-risk operations. |

| Newly Acquired Organizations | Does not automatically provide coverage for newly acquired or formed organizations. | Automatically covers newly acquired or formed organizations for up to 90 days. |

| Auto Liability | Often provides Hired and Non-Owned Auto (HNOA) liability coverage through a standard endorsement (vital for businesses that have employees run errands in personal cars). | Standard CGL policies generally exclude auto liability entirely, requiring a separate Commercial Auto policy. |

Understanding these distinctions allows an insurance producer to properly underwrite a client. If you have a massive manufacturing plant generating heavy pollution risk, or a rapidly expanding corporation buying out smaller companies every month, the rigid, pre-packaged BOP will legally and structurally fail them. They require the modularity and vast capacity of a standalone CGL. But for the local florist, the neighborhood bookstore, or the corner bakery, the Businessowners Policy offers an unparalleled, cost-effective synthesis of property and liability defense.