Crime, Fidelity Bonds, and Surety Bonds

The fundamental paradox of commerce is that to grow a business, an owner must systematically hand over the keys to their assets. They must trust cashiers with money, accountants with ledgers, and contractors with multimillion-dollar blueprints. Traditional property insurance protects the physical structures where business happens, and liability insurance shields against the accidents that occur along the way. But neither of these covers the most unpredictable exposure of all: human deception and the failure to fulfill a promise. When a client's own bookkeeper embezzles funds, or a hired construction firm abandons a half-built warehouse, standard property and casualty policies fall entirely silent. To protect the vital, invisible web of trust that allows a business to operate, the insurance industry relies on the highly specific mechanisms of Crime Insurance and Surety Bonds.

If a client calls you to say, "We were robbed last night," your immediate instinct as an insurance producer must be to translate their colloquial panic into the strict definitions of an insurance contract. In the legal architecture of a Commercial Crime policy, words like theft, burglary, and robbery are not interchangeable synonyms. They describe entirely different mechanical actions, requiring different proofs of loss.

Theft Crime insurance defines theft as any act of stealing. It is the broadest of the crime definitions. If an item was there yesterday and is gone today because someone took it with unlawful intent, it is theft. This includes everything from shoplifting to embezzlement.

However, because theft is so broad, insurers carve out specific, narrower perils to price risk accurately.

Burglary Crime insurance defines burglary as the taking of property from inside the premises by a person unlawfully entering or leaving the premises. Crucially, the definition of burglary in crime insurance strictly requires visible signs of forced entry or forced exit.

If a thief walks through an unlocked back door, steals a laptop, and walks out, that is theft, but it is definitively not burglary because there is no smashed glass, no jimmy marks on the door frame, and no wrecked padlock. The insurer requires those visible marks to prove that the perimeter was actually breached.

When dealing with highly secured assets, this concept tightens further into Safe Burglary. This requires visible marks of forced entry upon the exterior of a locked safe. If a thief simply guesses the combination or finds the combination written on a sticky note under the manager's keyboard, there is no safe burglary coverage because the exterior of the safe remains unmarred.

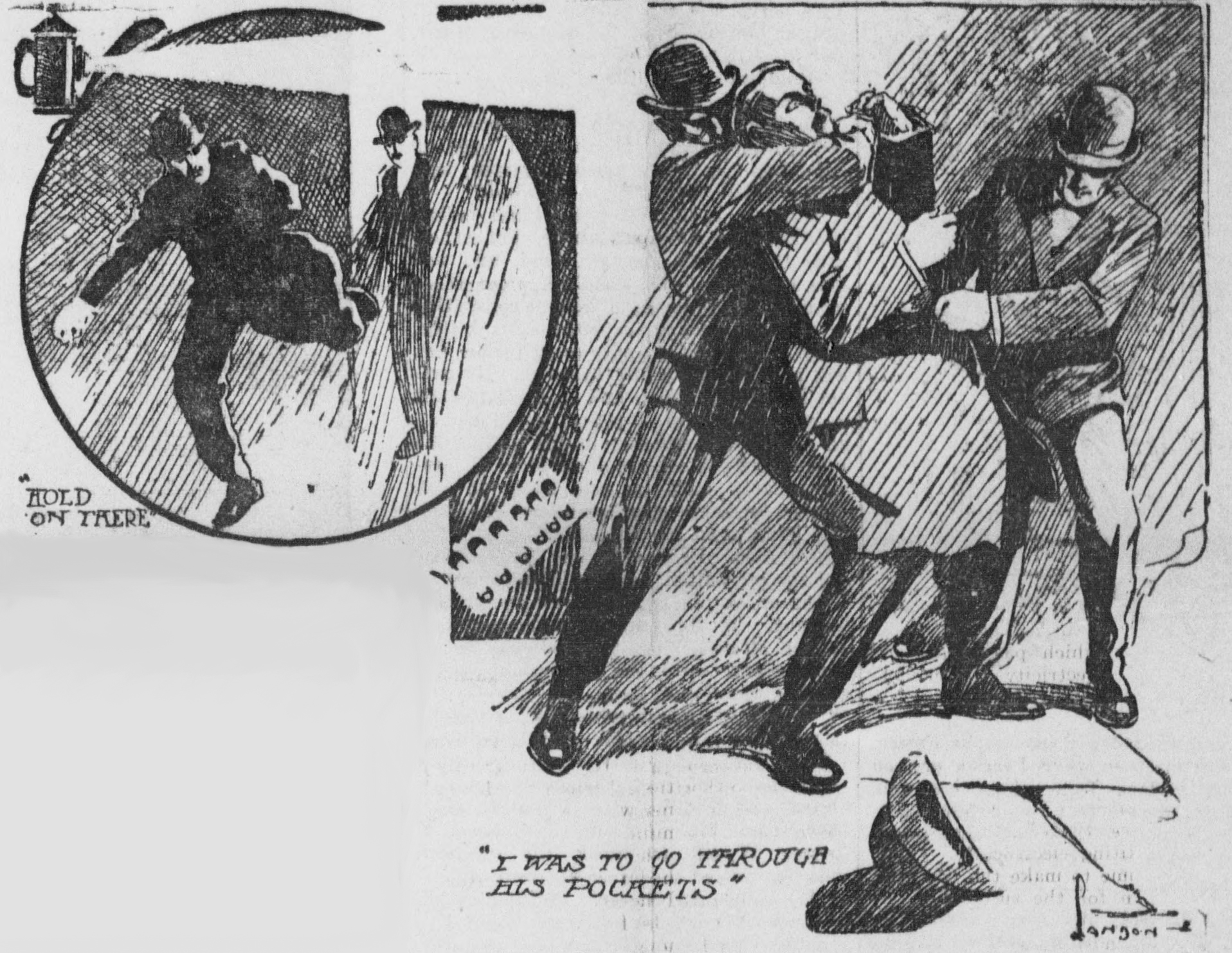

Robbery Crime insurance defines robbery as the taking of property from the care and custody of a person by threatening bodily harm. The definition of robbery in crime insurance requires an act of violence or the threat of violence against a person.

A pickpocket bumping into someone and swiping a wallet is theft. A mugger holding a weapon and demanding the wallet is robbery. Robbery is a crime against a person; burglary is a crime against property.

Crime is secretive by nature. An employee might siphon $500 a week from the cash register for five years before the auditor finally catches on. This temporal delay forces us to ask: which policy pays the claim? The one in effect when the theft occurred, or the one in effect when the theft was uncovered?

Commercial crime policies manage this dilemma through two distinct policy forms:

- The Discovery Form: A Discovery crime form covers losses discovered during the policy period. More importantly, a Discovery crime form covers losses regardless of when the actual loss occurred. If your client buys a Discovery form today and tomorrow uncovers a massive embezzlement scheme that began a decade ago, the current Discovery policy responds.

- The Loss Sustained Form: In contrast, a Loss Sustained crime form covers losses that actually occur during the policy period. If a theft happened three years ago but is found today, today's Loss Sustained policy will not pay. However, because businesses need time to audit their books, a Loss Sustained crime form allows the insured to discover the loss within one year after the policy expiration.

Crime policies carefully define exactly who is holding the property when it vanishes. Location and authorization matter immensely.

- Custodian: Crime insurance defines a custodian as the insured or an employee having care and custody of property inside the premises. However, the policy is exceedingly strict about who qualifies. The definition of a custodian in crime insurance strictly excludes a watchperson or a janitor. Why? Because while a janitor or night watchman is physically inside the building, the business owner has not authorized them to have care and custody of the daily receipts or inventory.

- Messenger: Crime insurance defines a messenger as the insured or an employee having care and custody of property outside the premises. When the store manager puts the daily cash drop in a bank bag and drives to the local bank branch, that manager transitions from a custodian to a messenger the moment they step off the premises.

Commercial Crime policies are modular. A business owner selects specific insuring agreements based on their unique operational exposures.

Employee Theft

The most devastating losses often come from within. Employee Theft coverage pays for the loss of money resulting directly from theft committed by an employee. But it does not stop at cash; it also pays for the loss of securities resulting directly from theft committed by an employee, and it pays for the loss of property other than money and securities resulting directly from theft committed by an employee (for instance, a warehouse worker fencing stolen electronics).

The "One Strike" Rule: Trust is a strict binary in insurance. Employee Theft coverage automatically terminates for a specific employee immediately after the insured discovers a dishonest act committed by that employee. If a manager catches a cashier stealing $20, decides to be merciful, and keeps them on staff without telling the insurer, the policy will not cover the $10,000 that same cashier steals six months later.

Inside and Outside the Premises

Theft of liquid assets requires special handling.

- Inside the Premises - Theft of Money and Securities coverage protects against the disappearance of money inside the insured premises. Notice the word disappearance—this is incredibly broad. If a stack of cash is simply missing from the register and no one knows how, this coverage applies.

- Inside the Premises - Robbery or Safe Burglary of Other Property coverage, however, has a vital limitation: it applies only to property other than money and securities. It is designed to cover the theft of inventory or equipment via violence (robbery) or forced entry (safe burglary).

- Outside the Premises crime coverage protects against the theft of money in the care of a messenger outside the premises. If your client's bookkeeper is mugged while walking the bank deposit down the street, this insuring agreement steps in.

Forgery and Paper Fraud

Despite the digital age, paper financial instruments remain highly vulnerable. Forgery or Alteration coverage protects against losses from the forgery of checks drawn by the insured. It also protects against losses from the alteration of promissory notes drawn upon the insured. If a thief steals a company checkbook, writes a check to themselves, and forges the owner's signature, this coverage makes the business whole.

Digital and Specialty Crime

Modern crime moves at the speed of the internet.

- Computer Fraud coverage applies when a computer is used to fraudulently transfer property from inside the premises to a person outside the premises. (Think of a hacker breaching the system to route inventory shipments to a dummy address).

- Funds Transfer Fraud coverage pays for losses resulting from fraudulent instructions directing a financial institution to transfer money from the insured's account. This frequently happens via phishing, where a thief impersonates a vendor and tricks the bank into wiring funds overseas.

- Money Orders and Counterfeit Money coverage pays for losses resulting from the insured accepting counterfeit currency in good faith.

- Extortion coverage is a highly specific, intense peril. It pays for the surrender of property away from the premises as a result of a threat to do bodily harm to an abducted person. If a criminal kidnaps an executive's spouse and demands ransom, extortion coverage responds.

We now pivot from Crime to Surety. While both are handled by Property & Casualty producers, they operate on entirely different philosophical foundations. Insurance anticipates that a certain percentage of people will suffer unavoidable losses (fires, car accidents, thefts). A surety bond, however, is a financial credit instrument.

A surety bond is written with the underwriting expectation that no losses will occur.

Because of this zero-loss expectation, a surety bond is a three-party contract, fundamentally unlike the two-party contract of traditional insurance (Insured and Insurer). A surety bond guarantees the performance of a specific obligation.

The Three Parties

The three parties in a surety bond are the principal, the obligee, and the surety.

- The Principal: The principal in a surety bond is the party who promises to perform the obligation. (e.g., A construction company promising to build a school).

- The Obligee: The obligee in a surety bond is the party who requires the bond. They are the beneficiary. The obligee in a surety bond receives the benefit of the bond if the principal fails to perform. (e.g., The school district requiring the construction company to be bonded).

- The Surety: The surety in a surety bond is the party who guarantees the principal's performance. (The insurance/bonding company backing the promise with their capital).

Penalty and Indemnification

If the principal defaults—say, the contractor walks off the job half-finished—the surety must step in and financially make the obligee whole. The maximum amount the surety will pay—the limit of liability in a surety bond—is called the penalty.

But the transaction does not end there. Because this is a credit relationship (like a co-signed loan), the principal must indemnify the surety for any loss the surety pays on behalf of the principal. The surety will pursue the defaulting contractor for every penny they paid out to the school district.

Contract Bonds

In commercial construction, specialized surety bonds—collectively known as Contract bonds—guarantee that a contractor will fulfill the terms of a construction contract. They follow the life cycle of a project:

- Bid bonds guarantee that a contractor bidding on a project will enter into the contract if awarded the bid. It prevents frivolous bidding.

- Performance bonds guarantee that a contractor will complete the work in accordance with the contract terms. If they go bankrupt midway, the surety funds the completion.

- Payment bonds guarantee that a contractor will pay all labor and material bills associated with a project. This ensures that unpaid subcontractors do not place a mechanic's lien on the obligee's newly built property.

Finally, we arrive at Fidelity Bonds, which represent a hybrid between the worlds of crime insurance and suretyship. Historically structured as bonds but frequently functioning like insurance policies today, fidelity bonds are used to protect employers from dishonest acts committed by their employees.

When a business wants to bond its employees, it must choose exactly how to schedule (list) the coverage. The structure determines the payout.

Scheduled Fidelity Bonds

For businesses that only want to bond specific high-risk individuals (like the CFO or head cashier), they use schedules.

- Name Schedule: A Name Schedule fidelity bond lists the specific names of the employees covered by the bond. (e.g., "John Doe and Jane Smith"). If John steals, there is coverage. If unlisted Bob steals, there is no coverage.

- Position Schedule: A Position Schedule fidelity bond lists the specific job titles covered by the bond (e.g., "Head Cashier"). Because turnover is high in many industries, a Position Schedule fidelity bond covers any individual holding a listed job title regardless of the employee's name.

Blanket Fidelity Bonds

For comprehensive protection, employers purchase blanket bonds, which cover the entire workforce. Both types below cover all employees, but they calculate limits drastically differently.

| Feature | Commercial Blanket Bond | Blanket Position Bond |

|---|---|---|

| Who is covered? | A Commercial Blanket fidelity bond covers all employees of an organization. | A Blanket Position fidelity bond covers all employees of an organization. |

| How is the Limit Applied? | A Commercial Blanket fidelity bond provides a single limit of liability for each loss. | A Blanket Position fidelity bond provides a separate limit of liability for each employee involved in a single loss. |

| The Payout Math | The limit of liability in a Commercial Blanket bond applies per loss regardless of the number of employees involved. | If 3 employees collude to steal, the limit is effectively multiplied by 3. |

Why this matters: Imagine your client has a $100,000 bond. Three warehouse workers collude to steal $300,000 worth of inventory. If the client holds a Commercial Blanket Bond, the maximum payout is $100,000, because it is viewed as one single loss event, regardless of how many employees colluded. If the client holds a Blanket Position Bond, the policy looks at the individuals. Because three employees were involved, each triggers their own 100,000limit,providingatotalpayoutof300,000.

As a producer, understanding the math behind these limits, the legal definitions of a crime, and the rigid obligations of a surety bond is how you move from being a salesperson to a vital risk advisor. You are not just selling paper; you are engineering the financial safety nets that catch a business when human nature fails.