Imagine a heavy steelvault suspended above the ground by two distinct cables. If you cut just one cable, the vault instantly plummets to the floor. Now, imagine a different vault, suspended by those same two cables, but engineered with a failsafe so that it only drops when both cables are severed. In the architecture of life insurance, these two mechanical triggers represent the fundamental divide in combination policies. Instead of steel cables, we are dealing with human lifespans.

The mechanical triggers of combination life insurance policies can be likened to a heavy steel bank vault suspended by cables: the payout executes either when the first cable snaps, or only after all cables give way.

A combination life insurance plan is a specialized financial instrument that covers two or more lives under a single contract. By tying multiple lives to a single payout trigger, insurers can design products that precisely match specific temporal needs—whether that is instantly replacing the income of whichever spouse dies first, or waiting to pay estate taxes that only come due after a married couple has passed away. For an insurance producer, mastering combination plans requires understanding not just who is covered, but exactly when the coverage executes and how that timing alters the underlying mathematics of the premium.

Before separating combination plans into their two primary categories, we must understand why they exist at all. Why buy one policy on two people instead of two individual policies?

The answer lies in both administrative friction and actuarial probability. At the basic operational level, combination life insurance plans offer distinct administrative convenience by requiring only a single policy fee. Because there is only one contract to underwrite, issue, and maintain, combination life insurance plans require only one regular premium payment to maintain coverage for multiple insureds.

More importantly, the premium for these policies is not calculated by simply adding the standalone cost of Person A to the standalone cost of Person B. Instead, the premium is calculated using a joint average age of the insured individuals. By blending the mortality risks of the applicants and guaranteeing only one ultimate death benefit payout, the insurer can price the coverage highly competitively compared to purchasing separate individual policies.

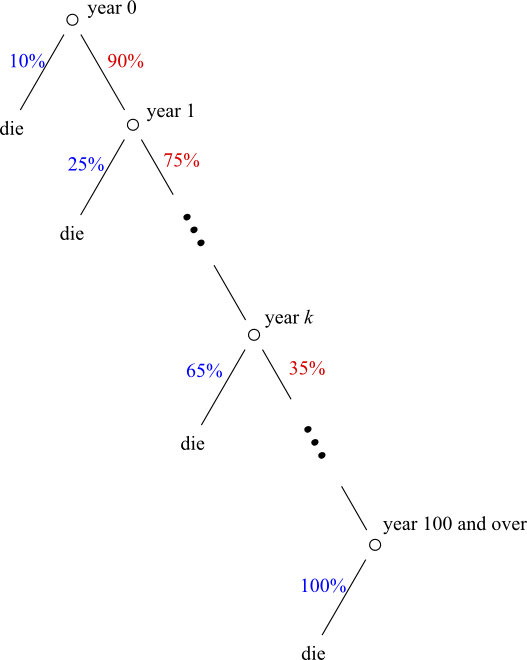

Actuaries utilize mathematical mortality models, such as survival trees, to blend the probability of death for multiple applicants, allowing insurers to calculate a competitive premium based on a joint average age.

A Joint Life insurance policy is a type of combination plan covering multiple insured individuals where the temporal trigger is set to the absolute earliest point of mortality. Consequently, a Joint Life policy is commonly referred to as a first-to-die policy.

Mechanics of the Payout

The mechanics are absolute: the death benefit of a Joint Life policy is paid upon the death of the first insured person.

Critical Concept: Because the contract is designed to execute upon the first death, a Joint Life policy terminates immediately after the first insured dies.

This creates a vital consideration that you must clearly explain to future clients: the surviving insured of a Joint Life policy loses life insurance coverage under that specific contract after the first insured dies. If the survivor still needs life insurance at that point, they will have to apply for a new policy at their older, attained age—assuming they are still medically insurable.

Cost and Application

Despite the loss of coverage for the survivor, a Joint Life policy costs less in premium than two separate individual policies of the exact same death benefit. If a couple needs a $500,000 payout upon the death of either partner, buying one $500,000 Joint Life policy is mathematically cheaper than buying two separate $500,000 individual policies, because the insurance company is only on the hook to pay out exactly once, rather than potentially twice.

This structure dictates its two primary real-world applications:

Income Replacement for Couples: Married couples often use Joint Life insurance to replace lost household income upon the death of the first spouse. If two spouses rely heavily on each other's salaries to pay the mortgage and feed their children, the financial crisis occurs the moment the first paycheck disappears. The Joint Life payout perfectly intercepts this crisis.

Business Buy-Sell Agreements: Joint Life insurance is frequently used to fund business buy-sell agreements between partners. If a business has two equal partners, they need a mechanism to buy out the shares of whichever partner dies first. A Joint Life policy guarantees that the surviving partner instantly receives the exact liquidity needed to purchase the deceased partner's share from their heirs, keeping the business intact.

If Joint Life triggers at the very first sign of mortality, Survivorship Life insurance is the exact opposite. A Survivorship Life insurance policy covers two or more lives under a single insurance contract, but it delays the payout until the final biological cable snaps. Therefore, a Survivorship Life policy is commonly referred to as a second-to-die policy.

Mechanics of the Payout

A Survivorship Life policy pays the death benefit only upon the death of the last surviving insured. Consequently, a Survivorship Life policy does not pay any death benefit upon the death of the first insured person. When the first spouse passes away, the policy continues in force, and premiums must typically continue to be paid by the survivor (unless the policy is fully paid up).

The Actuarial Discount

Like Joint Life, the premium for a Survivorship Life policy is based on a joint average age of the insureds. However, the pricing dynamics are fascinating when we compare the two combination plans against one another.

A Survivorship Life policy generally features a lower premium than a Joint Life policy with an identical death benefit. To understand why, we must look at the mathematics of mortality probability. The life expectancy of the last survivor on a multi-life policy is statistically longer than the life expectancy of the first person to die.

Think of rolling a pair of dice, waiting to roll a one. You will roll a one on either of the dice much sooner than you will wait for both dice to land on a one simultaneously. Because the insurer does not have to pay out until the second death, they have a much longer runway to collect premiums and earn interest on their reserves. This longer expected premium-paying timeline lowers the overall cost for a Survivorship Life policy relative to a first-to-die policy.

Just as waiting for two dice to simultaneously land on a specific number takes statistically longer than waiting for either single die to do so, insurers anticipate a much longer premium-paying timeline before a second-to-die policy pays out.

Because the payout is deliberately delayed until both insureds are gone, Survivorship Life insurance is primarily utilized in strategic estate planning.

In the United States, the "unlimited marital deduction" allows a deceased person to pass an unlimited amount of assets to their surviving spouse without triggering federal estate taxes. Therefore, when the first spouse dies, there is usually no estate tax problem. The hammer falls when the second spouse dies, and the combined wealth is passed down to the children or non-spouse heirs. At that precise moment, the estate tax bill comes due.

With top federal estate tax rates historically taking a substantial percentage of transferred wealth, Survivorship policies are precisely timed to provide the liquidity necessary to satisfy the IRS upon the second spouse's death.

Survivorship Life insurance is designed to provide funds to pay estate taxes after both insured spouses have died. By matching the precise timing of the tax liability to the execution of the policy, the death benefit from a Survivorship Life policy provides immediate cash liquidity to the beneficiaries of an estate.

Why does this matter? Many high-net-worth estates are "asset rich but cash poor"—composed of family farms, commercial real estate, or private businesses. Without life insurance, heirs might be forced to sell a beloved $10,000,000 family farm at a fire-sale discount just to generate the cash to pay the IRS. The cash liquidity from a Survivorship Life policy helps prevent the forced liquidation of valuable estate assets to cover settlement costs.

To crystallize these differences for your exam and your future practice, rely on this structural breakdown:

Feature

Joint Life (First-to-Die)

Survivorship Life (Second-to-Die)

Covered Lives

Two or more under a single contract

Two or more under a single contract

Payout Trigger

Death of the first insured

Death of the last surviving insured

First Death Event

Pays death benefit; policy terminates immediately

No death benefit paid; policy continues

Survivor's Status

Loses coverage under the contract

Remains insured; waits for payout

Premium Cost

Less than two separate individual policies

Lower than a Joint Life policy for the same amount

Actuarial Basis

Premium based on joint average age

Premium based on joint average age

Primary Use Case

Income replacement; Business Buy-Sell agreements

Strategic estate planning; Estate tax liquidity

As a producer, your job is not merely to sell a product, but to match the architecture of a contract to the vulnerability of your client. If the financial threat is triggered by the loss of the first life—such as a disrupted mortgage or a vulnerable business partnership—you deploy Joint Life. If the financial threat is a tax liability that only crystallizes after the final life is extinguished, you deploy Survivorship Life, leveraging actuarial patience to secure a massive benefit at a minimized cost.