Equipment Breakdown and Completed Operations Liability

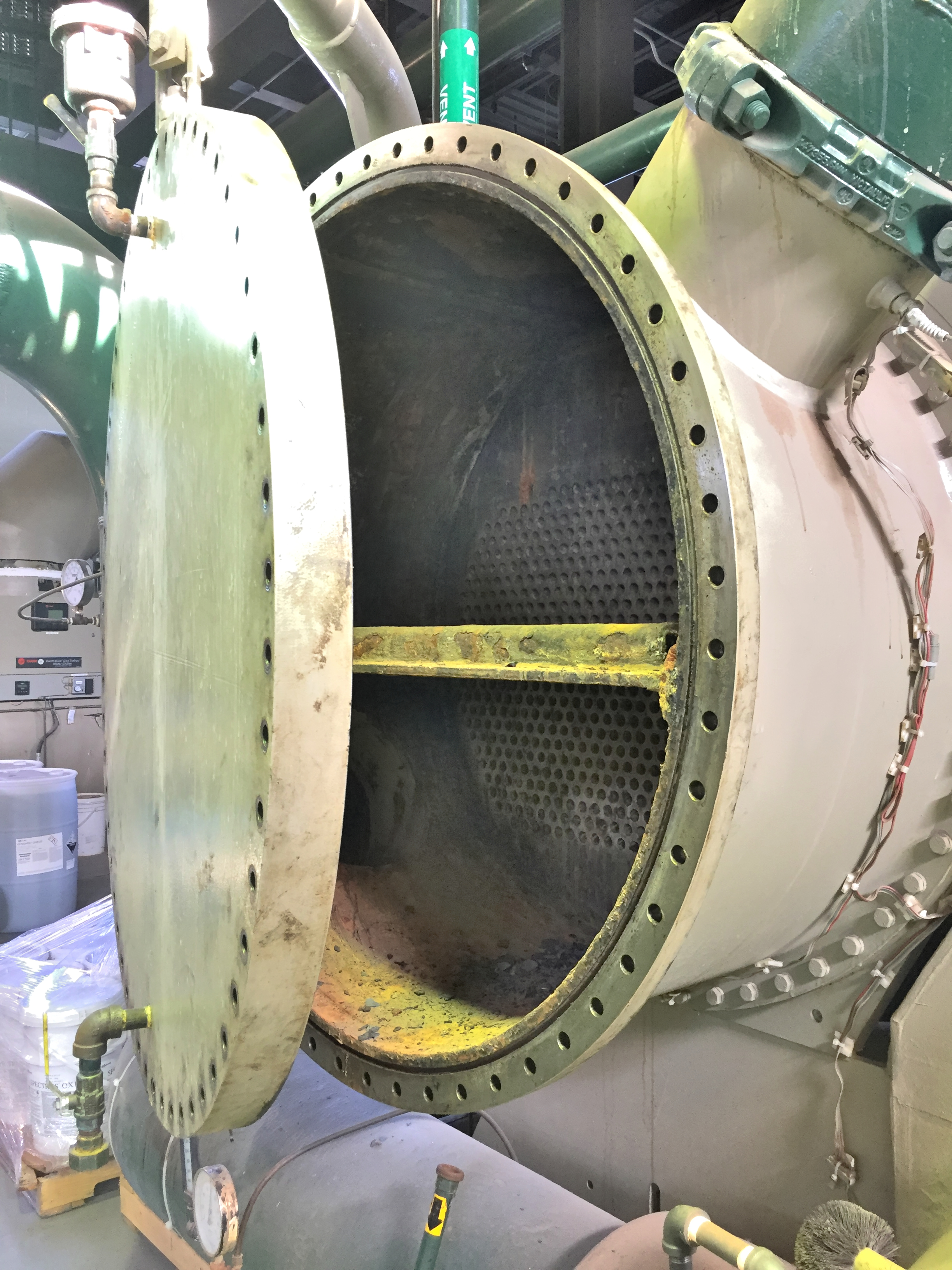

Consider the physical forces harnessed inside a commercial manufacturing plant: immense pressure vessels generating steam, industrial refrigeration units maintaining strict thermal gradients, and electrical panels managing massive voltage. If a pressure valve fails, the resulting explosion is a violent release of kinetic energy. Now consider the plumbing contractor who installed that valve and packed up their tools three months ago. Standard commercial property insurance will not pay for the exploded boiler, and standard premises liability will not protect the absent plumber when the dust settles. The architecture of commercial insurance requires specialized mechanisms to address failures generated from within a machine, and liabilities that awaken long after a contractor has walked away.

As an insurance producer, you will quickly learn that nature abhors a vacuum, and the insurance industry abhors a coverage gap. Understanding exactly where standard policies end and these specialized coverages begin is the difference between a fully protected client and catastrophic uninsured ruin.

To understand equipment breakdown insurance—which was formerly known as boiler and machinery coverage—you must first understand the limitations of a standard commercial property policy.

Standard commercial property policies are designed to handle external forces. They cover damage caused by external perils such as fire or wind. However, standard commercial property policies exclude coverage for mechanical breakdown, they exclude coverage for electrical arcing, and they exclude coverage for steam boiler explosions.

If a hurricane tears the roof off a factory, the property policy responds. But if a centrifugal chiller tears itself apart from the inside out due to a mechanical fault, the standard property policy provides nothing. Equipment breakdown coverage fills the coverage gaps created by standard commercial property policy exclusions. Conversely, it respects the boundaries of the property policy: equipment breakdown policies do not cover damage caused by external perils such as fire or wind.

The Anatomy of a Breakdown

Equipment breakdown insurance covers financial loss resulting from the accidental breakdown of covered equipment. Notice the word accidental. This is not a maintenance contract. To trigger this policy, there must be a sudden, unexpected event. Specifically, an equipment breakdown policy requires direct physical loss or damage to the equipment to trigger coverage.

What exactly constitutes "covered equipment" and the perils that threaten it? The scope is vast but highly specific to machinery that generates, transmits, or consumes energy.

- Covered equipment in an equipment breakdown policy includes boilers.

- Covered equipment... includes pressure vessels.

- Covered equipment... includes refrigeration systems.

- Covered equipment... includes mechanical equipment.

- Covered equipment... includes electrical systems.

When we examine the perils that this policy insures against, we are looking at the internal physics of these machines. Equipment breakdown coverage insures against perils such as electrical arcing, mechanical breakdown, motor burnout, and boiler explosions (specifically steam boilers, which carry massive explosive potential).

Because insurance protects against the accidental, not the inevitable march of entropy, there are strict exclusions. Equipment breakdown insurance excludes coverage for damage caused by normal wear and tear. It also excludes coverage for equipment deterioration, and critically, it excludes coverage for equipment breakdowns caused by a lack of maintenance. You cannot neglect to oil a heavy industrial lathe for five years and expect the insurer to buy you a new one when it seizes.

Financial Recovery and Expediting Expenses

When an accidental breakdown occurs, the financial impact ripples outward. At a baseline, equipment breakdown policies typically pay for the cost to repair or replace the damaged equipment.

However, in the real world of commercial operations, waiting weeks for a specialized part can bankrupt a company. Therefore, equipment breakdown policies often include coverage for expediting expenses.

Expediting Expenses These are the rush costs associated with getting a business back online.

- They cover the reasonable extra cost to make temporary repairs to damaged equipment (e.g., renting a portable generator while the main panel is fixed).

- They cover the extra cost to expedite permanent repairs to damaged equipment (e.g., paying a $5,000 premium to overnight-freight a replacement motor from Germany).

The damage from a breakdown often extends beyond the machine itself. Equipment breakdown coverage can include business income insurance if operations are suspended due to a covered breakdown, replacing lost revenue while the business is paralyzed. It can include extra expense insurance if operations are suspended due to a covered breakdown, paying for costs like leasing temporary workspace. Finally, for businesses like grocery stores or pharmaceutical distributors, the policy can provide spoilage coverage for perishable goods damaged by a covered breakdown (such as a massive refrigeration failure).

The Power of the Inspector

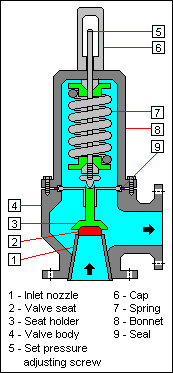

Equipment breakdown is unique in the insurance world because it pairs financial indemnity with rigorous loss prevention. A steam boiler is effectively a stationary bomb if poorly maintained; therefore, insurers have a vested interest in safety.

Equipment breakdown policies give the insurance company the right to inspect the insured equipment at any reasonable time. This is not merely an adversarial audit; it is a vital service. In fact, insurance company inspectors often conduct state-mandated safety inspections of insured boilers and pressure vessels on behalf of the policyholder. This saves the business owner from having to hire separate municipal inspectors to satisfy state safety laws.

If an inspector discovers a severe hazard—say, a pressure relief valve that has been welded shut—the response is immediate. Insurance companies have the right to immediately suspend equipment breakdown coverage if the equipment is found to be in a dangerous condition. To enforce this, the suspension of equipment breakdown coverage due to dangerous conditions requires written notice delivered or mailed to the insured.

Now we shift our focus from the physics of machinery to the timeline of a contractor’s legal liability.

When a contractor is actively working on a job site, their liability for causing bodily injury or property damage falls under the premises and operations liability coverage of their Commercial General Liability (CGL) policy. But what happens when the contractor finishes the job and goes home?

Enter Completed Operations Liability. This is a specialized component of the commercial liability framework. Completed operations liability is a component of the Commercial General Liability policy, and it specifically falls under the Products-Completed Operations Hazard section of a Commercial General Liability policy.

Its purpose is foundational to construction and service industries: Completed operations liability protects contractors from liability arising after a job is finished. More precisely, it protects contractors from liability arising after they have left the job site permanently.

The Triggers of Coverage

Timing and location are everything here. Completed operations liability does not apply to work that is currently in progress. As a producer, you must remind your clients that uncompleted work in progress falls under the premises and operations liability coverage of a Commercial General Liability policy.

So, when exactly does the coverage transition? Completed operations liability is triggered only after the contractor's operations have been completed OR after the contractor's operations have been abandoned.

The definition of "complete" in an insurance contract is strictly defined by three scenarios. An operation is considered complete when:

- All work called for in the contract has been finished.

- All work to be done at a specific job site has been completed. (Even if the contractor has other contracts with the same client elsewhere).

- The work has been put to its intended use by a customer or property owner. (If a homeowner starts cooking in a newly renovated kitchen, the kitchen operation is complete, even if the contractor still needs to install one piece of trim).

There is a vital caveat to this definition: work that requires further service or correction is still considered complete under the Products-Completed Operations hazard. Likewise, work that requires further maintenance or repair is still considered complete under the Products-Completed Operations hazard. A contractor cannot claim a job is "incomplete" simply because they have to go back to fix a loose screw.

What Is Covered, and Where?

Once triggered, completed operations liability covers bodily injury caused by the contractor's completed work, and it covers property damage caused by the contractor's completed work.

Geographically, this coverage acts as a protective tail that follows the contractor's footprint. Completed operations liability applies to bodily injury or property damage occurring away from premises owned or rented by the insured contractor. (If a client is injured at the contractor's own office, that is standard premises liability).

The "Your Work" Exclusion: A Crucial Distinction

This is where many new producers—and veteran contractors—misunderstand the policy. General liability insurance is not a warranty for poor craftsmanship.

Completed operations liability does not cover the cost to repair the contractor's defective work itself. Furthermore, it does not cover the cost to replace the contractor's defective work itself.

This specific limitation is formally known in the industry: The exclusion for damage to the contractor's own work is known as the "Your Work" exclusion. Essentially, the "Your Work" exclusion in completed operations liability eliminates coverage for property damage to the work performed by the insured contractor.

To illustrate this, let us look at a classic claims scenario:

- If a contractor installs a faulty pipe that later bursts and damages a customer's floor, completed operations liability covers the damaged floor. (The floor is resulting property damage).

- However, if a contractor installs a faulty pipe that later bursts and damages a customer's floor, completed operations liability does not cover the replacement of the faulty pipe. (The pipe is the contractor's own work, and its replacement is excluded).

The insurance company will pay $15,000 to replace the ruined hardwood floors, but the contractor must pay the $500 out-of-pocket to buy and install a new pipe.

The Subcontractor Exception

In modern construction, a general contractor rarely does all the work themselves; they hire subcontractors. The CGL policy recognizes this reality.

Completed operations liability policies often include an exception to the "Your Work" exclusion for work performed on behalf of the insured by subcontractors.

Why does this matter? If an electrician (a subcontractor) wires a house improperly, and a month later the house burns down, the entire house was technically the general contractor's "work." Under a strict reading of the exclusion, the general contractor would have no coverage for the destroyed house. But because of this exception, if a subcontractor's faulty work damages the general contractor's completed project, the general contractor's completed operations liability will cover the resulting damage. This exception is what allows large general contractors to sleep at night.

Aggregate Limits

Finally, how much will the policy pay over time? Liability policies cap their payouts.

The Products-Completed Operations aggregate limit is the maximum amount an insurer will pay for all claims arising from the Products-Completed Operations hazard during the policy period.

If a contractor has a $2,000,000 Products-Completed Operations aggregate limit, and three separate completed roofs collapse in one year resulting in $1,000,000 claims each, the insurer will only pay up to the $2,000,000 aggregate limit for the year, leaving the contractor exposed for the remaining $1,000,000.

As an aspiring producer, grasping the mechanics of Equipment Breakdown and Completed Operations Liability is paramount. You are not just selling paper; you are analyzing the kinetic reality of your client's business. You must foresee the machine that fails from within, and the liability that emerges long after the tools are put away.