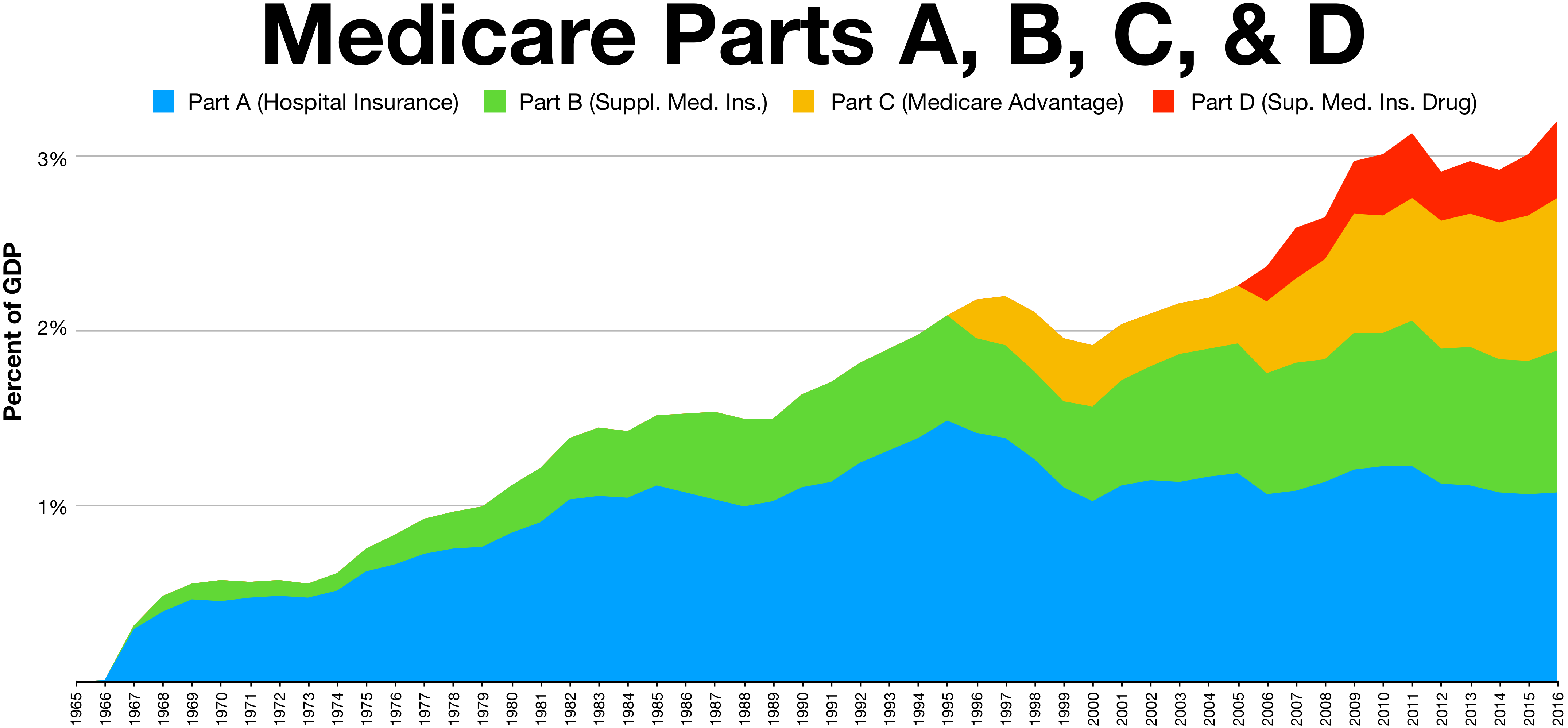

Medicare (Parts A, B, C, D)

A standard private health insurance policy operates like a single locked door: your client pays one premium, meets one calendar-year deductible, and the entire house of medical benefits opens to them. Medicare, the federal health insurance program administered by the Centers for Medicare and Medicaid Services (CMS), abandons this monolithic approach. Instead, it is structurally modular. It divides human healthcare into distinct categories—hospitals, physicians, and pharmacies—and insures them under entirely different rule sets, funding mechanisms, and cost-sharing models.

For an aspiring insurance producer, mastering Medicare means understanding how these separate moving parts—Parts A, B, C, and D—interlock to form a safety net primarily designed to provide health insurance for individuals aged 65 and older.

Before we can dissect the parts of Medicare, we must understand who is allowed into the system and when. While Medicare is primarily an age-based program for those 65 and older, biological reality dictates that severe medical catastrophe can strike earlier. Consequently, the federal government opens the Medicare gates to specific individuals under age 65.

If a younger client has End-Stage Renal Disease (ESRD), they are eligible for Medicare. If they are diagnosed with Amyotrophic Lateral Sclerosis (ALS), they are automatically eligible for Medicare without a waiting period. For other severe, long-term disabilities, individuals under age 65 who have received Social Security Disability benefits for 24 months become eligible.

For the vast majority turning 65, entry is dictated by the Medicare Initial Enrollment Period. This is not a single date, but a window that lasts for a total of seven months. It begins three months prior to the month of an individual's 65th birthday, includes their birthday month, and extends for three months afterward.

Producer Tip: If a client misses this critical 7-month window, they are not locked out forever, but they must wait for the Medicare General Enrollment Period, which runs from January 1 through March 31 of each year. Delaying enrollment, as we will see, often triggers permanent financial penalties.

If Medicare is a modular house, Medicare Part A is the physical structure. Commonly referred to as Hospital Insurance, Part A exists to cover the heavy, facility-based costs of a medical crisis. It provides coverage for inpatient hospital care, care received in a skilled nursing facility (SNF), hospice care for terminally ill patients, and limited coverage for home health care services.

Most eligible individuals receive Medicare Part A without paying a monthly premium. This is not a "free" benefit; it is prepaid. Medicare Part A is premium-free for individuals who have paid Medicare taxes for at least 40 calendar quarters (roughly 10 years of working life).

The Benefit Period Concept

To understand Part A cost-sharing, you must unlearn how standard private insurance works. Private health plans reset deductibles on January 1st. Medicare Part A ignores the calendar. Instead, Medicare Part A utilizes a benefit period system rather than a calendar year to measure the use of hospital and skilled nursing facility services.

Think of a benefit period as a stopwatch tied to the patient's immediate health event. A Medicare Part A benefit period begins on the first day a patient enters a hospital as an inpatient. The stopwatch keeps ticking until the patient has achieved a sustained recovery. Specifically, a Medicare Part A benefit period ends when the patient has been out of the hospital or skilled nursing facility for 60 consecutive days.

Because the system is event-based, Medicare Part A requires the patient to pay a deductible for each new benefit period. If a client goes to the hospital in February, recovers fully by May, and goes back in October, they will pay that Part A deductible twice in one year.

Inpatient and Lifetime Reserve Days

Once a patient is admitted, Medicare covers the room and board on a sliding scale.

| Days in Single Benefit Period | Patient Responsibility |

|---|---|

| Days 1–60 | $0 patient coinsurance (after the benefit period deductible is met). |

| Days 61–90 | Medicare Part A requires a daily patient copayment. |

| Days 91+ | The patient must begin using "Lifetime Reserve Days." |

What happens if a devastating illness keeps a patient in the hospital past 90 days? Lifetime reserve days are utilized when a Medicare patient exceeds 90 days of inpatient hospital care during a single benefit period. Medicare Part A provides 60 non-renewable lifetime reserve days for inpatient hospital care. During this phase, Medicare Part A requires a daily patient copayment for each lifetime reserve day used. Because these are "lifetime" reserve days, once a patient uses them, they are gone forever.

Skilled Nursing and the Custodial Trap

After a severe hospitalization, a patient often needs rehabilitation. Medicare Part A provides coverage for this, but with strict caveats. First, Medicare Part A requires a prior inpatient hospital stay of at least three consecutive days to qualify for skilled nursing facility coverage.

If they meet this requirement, Medicare limits skilled nursing facility coverage to a maximum of 100 days per benefit period. The cost-sharing looks like this:

- Days 1–20: Medicare covers the first 20 days of skilled nursing facility care with zero patient coinsurance.

- Days 21–100: Medicare Part A requires a daily patient copayment for skilled nursing facility days 21 through 100.

Here is the most critical conversation you will have with clients regarding Part A: Medicare Part A completely excludes coverage for custodial care. If a client simply needs help with the activities of daily living (bathing, dressing, eating) due to aging or cognitive decline, Medicare will not pay for their nursing home stay. Medicare pays to rehabilitate (skilled nursing); it does not pay to babysit (custodial care).

(Note: There is also a quirky historical rule in Part A regarding transfusions. To encourage blood donation, Medicare Part A requires the patient to pay for the first three pints of blood received during a calendar year.)

If Part A is the hospital building, Medicare Part B pays for the professionals walking the halls and running the clinics. Commonly referred to as Medical Insurance, Part B is the engine of routine and specialized healthcare.

Part B provides coverage for physician and surgeon services, outpatient medical services, durable medical equipment (DME, like wheelchairs and oxygen tanks), and many preventive care services.

Unlike Part A, enrollment in Medicare Part B is optional for eligible individuals. Because it is optional, it is not prepaid via payroll taxes. Medicare Part B requires enrollees to pay a standard monthly premium. While most pay the standard rate, the government applies a means test to the wealthy: the standard Medicare Part B monthly premium is subject to an income-related adjustment amount (IRMAA) for higher earners.

The 80/20 Rule and the Infinite Risk

Part B finances operate on a simple mechanism. It features an annual deductible that the enrollee must satisfy before coverage begins. After the annual deductible is met, Medicare Part B requires a coinsurance amount of 20 percent for most covered services.

On its face, an 80/20 split sounds excellent. But as an insurance professional, you must instantly recognize the mathematical danger here. Original Medicare Part A and Part B do not include an annual out-of-pocket maximum limit for patient costs.

Twenty percent of a $500 doctor's visit is highly affordable. Twenty percent of a $250,000 outpatient chemotherapy regimen will bankrupt a retiree. This limitless 20% exposure is the exact reason the private insurance market for Medicare Supplements and Medicare Advantage plans exists.

Furthermore, Original Medicare has blind spots for routine aging issues. Medicare Part B completely excludes coverage for routine dental care, routine eye exams and eyeglasses, and hearing aids.

Recognizing the unlimited financial risk and the excluded benefits of Original Medicare, the government created an alternative path. Medicare Part C is formally known as Medicare Advantage.

Medicare Part C plans are offered by private insurance companies approved by the federal government. To step onto this private track, an individual must be actively enrolled in both Medicare Part A and Medicare Part B to join a Medicare Part C plan. They do not leave the federal system; rather, they allow a private company to administer their federal benefits.

By law, Medicare Part C plans must provide all the equivalent medical benefits of Original Medicare Part A and Part B. But private insurers compete for clients by offering more. Medicare Part C plans frequently include bundled prescription drug coverage, and they often offer supplementary benefits such as dental, vision, and hearing coverage—precisely the items Part B excludes.

The Trade-off: Networks and Caps

Why doesn't everyone choose Part C? Because to offer these extra benefits while keeping costs down, Medicare Part C plans are typically structured using managed care networks like Health Maintenance Organizations (HMOs) or Preferred Provider Organizations (PPOs).

When a client chooses Part C, they trade the absolute freedom of Original Medicare for network restrictions. Medicare Part C plan networks may require enrollees to receive non-emergency care strictly from contracted doctors and hospitals.

Financially, clients must understand two things. First, Medicare Part C enrollees must continue to pay their regular Medicare Part B monthly premium to the government (plus any premium the Advantage plan itself charges). Second, and most importantly, Medicare Part C plans are legally required to establish an annual maximum out-of-pocket limit for covered medical services. This caps the limitless 20% exposure of Part B, giving retirees financial peace of mind.

The final module of the Medicare architecture handles the pharmacy. Medicare Part D provides specific coverage for prescription medications.

Like Part C, Medicare Part D plans are exclusively offered by private insurance companies approved by Medicare. If a client decides to stay with Original Medicare (Parts A & B) rather than moving to an Advantage plan, they will need a drug plan. An individual must possess either Medicare Part A or Medicare Part B to enroll in a standalone Medicare Part D prescription drug plan.

Because this is a separate private policy, Medicare Part D requires enrollees to pay a monthly premium separate from Part B premiums, and it features an annual deductible for prescription drug costs.

Formularies, Tiers, and Cost-Sharing

No single Part D plan covers every medication in existence. Instead, Medicare Part D plans utilize a formulary document to list all covered prescription drugs. To manage costs, Medicare Part D plan formularies place medications into different pricing tiers that determine the patient copayment amount (e.g., Tier 1 for cheap generics, Tier 4 for expensive specialty drugs).

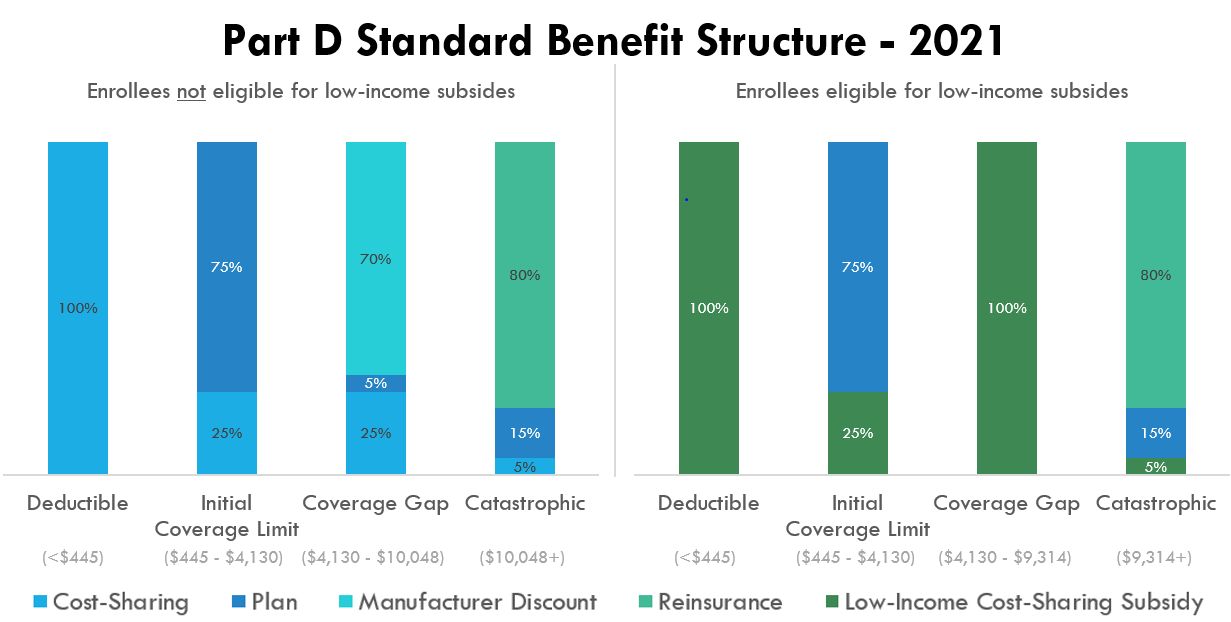

Navigating the Donut Hole

Part D features a unique, multi-phase cost-sharing structure designed to balance government subsidies with consumer responsibility.

- Initial Phase: After the deductible, the patient pays their standard tier copays until the total cost of their drugs (what the patient paid + what the plan paid) hits a federally defined threshold.

- The Coverage Gap: A Medicare enrollee enters the Part D coverage gap phase after total prescription drug costs reach a federally specified initial limit. The Medicare Part D coverage gap phase is commonly referred to as the "donut hole." During the Medicare Part D coverage gap phase, the enrollee pays a maximum of 25 percent of the cost for covered prescription drugs.

- Catastrophic Phase: If a patient is taking highly expensive medications, they will eventually spend their way out of the gap. Medicare Part D catastrophic coverage begins after an enrollee's total out-of-pocket spending reaches a specified annual threshold. During the Medicare Part D catastrophic coverage phase, the enrollee pays only a small copayment or coinsurance for covered drugs for the remainder of the calendar year.

The Penalty for Waiting

Insurance relies on the law of large numbers. If healthy people refused to buy Part D until they developed a condition requiring expensive medication, the risk pool would collapse.

To prevent this adverse selection, the government instituted a strict consequence: Medicare Part D imposes a late enrollment penalty on individuals who go 63 continuous days without creditable prescription drug coverage after their Initial Enrollment Period.

This is not a temporary slap on the wrist. The Medicare Part D late enrollment penalty is permanently added to the monthly premium for as long as the individual maintains Medicare drug coverage. As a producer, ensuring your clients do not accidentally trigger this lifelong penalty is one of the most vital services you will provide.