CO Additional Topics: Water Rights, Disclosures, Taxes & Foreclosure

The physical soil a client purchases in Colorado is entirely distinct from the legal rights that animate its value. When you look at a ranch in the Rockies or a subdivision in Denver, you are not merely observing land; you are looking at an intersecting web of invisible legal frameworks. As a Colorado real estate broker, your license grants you the authority to navigate this matrix of water rights, statutory disclosures, tax calendars, and foreclosure mechanics. The Colorado Real Estate Commission evaluates you on these statutes not to test your trivia recall, but because failing to understand the mechanics of this system will cost your clients their homes, their wealth, or their legal standing.

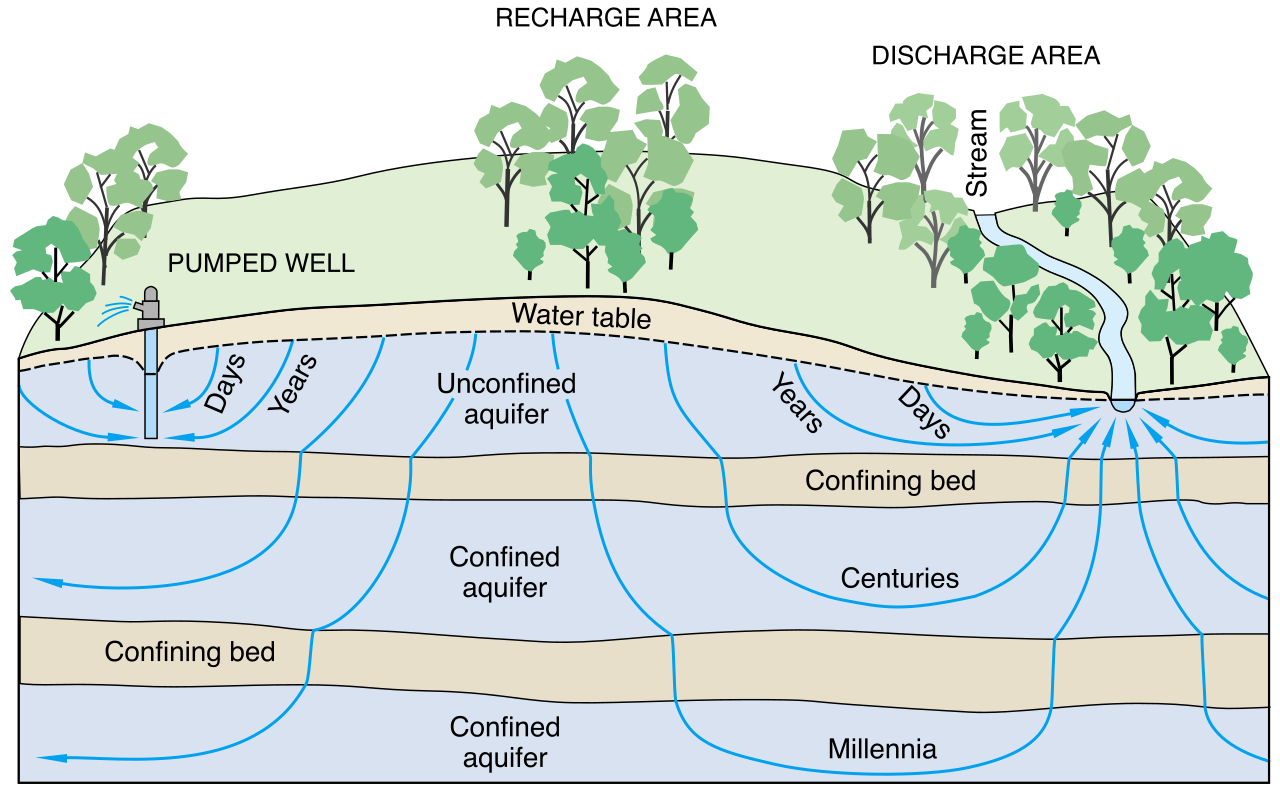

To understand Colorado real estate, you must completely separate the concept of water from the dirt it runs through. A water right in Colorado is distinct from the land. You can own the soil without owning the stream that cuts through it. Because it is severed from the physical earth, a water right in Colorado is a real property right conveyed by a deed, meaning it acts just like real estate and can be sold separately from the associated land.

Because water is often the most valuable invisible asset in a transaction, the Colorado Real Estate Commission requires the Source of Water Addendum in all residential real estate transactions. This mandatory form discloses whether the residential property's water source is a well, a water provider, or another source.

If the property relies on a well, the legal mechanics shift. A well permit in Colorado provides a legal right to use water, but nature does not read government documents: a well permit in Colorado does not guarantee the physical presence or continuous availability of water. If the aquifer runs dry, your legal permit cannot conjure water from dust.

When a property with a well changes hands, the State requires a precise chain of custody. Buyers of a property with a small capacity well must complete a Change in Owner Name form for the Division of Water Resources. The regulatory burden involves a coordinated dance between the buyer and the closing agent:

- A closing service provider (typically the title company) in a Colorado real estate transaction must submit the well ownership transfer form to the Division of Water Resources within 60 days after closing.

- However, the statutory duty ultimately falls on the new owners: buyers of a property with a well must file the Change in Owner Name form within 63 days after closing.

Information asymmetry destroys markets. Colorado levels the playing field through the doctrine of actual knowledge. Colorado sellers must disclose known material defects about the property under this doctrine, meaning they are only responsible for what they actually know, not what they should have known.

The Seller's Property Disclosure form must be completed based exclusively on the seller's current, actual knowledge. Because this document represents the seller's legal testimony about the physical state of the property, Colorado real estate brokers are prohibited from completing the Seller's Property Disclosure form on behalf of the seller. If you fill it out for them, you are practicing law and assuming their liability. Furthermore, honesty is not optional: a seller checking "don't know" on the Seller's Property Disclosure form when they possess actual knowledge of a defect constitutes fraud.

Specific Health, Safety, and Structural Disclosures

Beyond general defects, Colorado and federal law mandate highly specific disclosures:

- Methamphetamine: Colorado law requires a seller to disclose if the property was ever used as a methamphetamine laboratory. However, the law provides a logical off-ramp: a Colorado seller is exempt from disclosing a past methamphetamine laboratory if the property was properly remediated to state standards.

- Carbon Monoxide: To prevent tragic fatalities, Colorado law mandates that sellers assure the property has an operational carbon monoxide alarm installed within 15 feet of every bedroom entrance.

- Lead-Based Paint: Because of federal law, sellers of residential property built before 1978 must provide a federal lead-based paint disclosure.

- Square Footage: As a broker, you cannot take the seller's word for the size of the home. Colorado real estate brokers must verify and disclose the square footage of a residential property. A real estate broker cannot rely on a seller's own measurement for the Square Footage Disclosure. You must state the source of the measurement (such as county records or a prior appraisal) in the Colorado Square Footage Disclosure.

Financial and Community Disclosures

Buyers must also be warned about the invisible financial structures governing their new property. The Colorado residential real estate contract contains a mandatory disclosure regarding Special Taxing Districts. This disclosure warns buyers that the property may be subject to general obligation debt paid by annual tax levies—meaning the buyer could be footing the bill for local infrastructure through elevated tax bills.

If the property is bound by a Homeowners Association (HOA), the seller's duties expand. Colorado sellers of properties within a common interest community must provide the buyer with the homeowner association's governing documents and financial records. These communities do not operate in the wild west; the Colorado Common Interest Ownership Act (CCIOA) regulates the creation and operation of homeowner associations, providing statutory guardrails for how these micro-governments function.

Colorado property taxes operate on a mechanical delay. You pay for the snow after it melts: Colorado property taxes are paid in arrears for the previous calendar year.

The timeline is rigid and absolute. Colorado property tax notices are mailed to the property owner of record in January. The state allows flexibility in how you pay, but not when. Colorado property owners may pay annual property taxes in two equal halves or in one single full payment.

| Payment Method | Deadlines |

|---|---|

| Two Equal Halves | First half payment is due by the last day of February.<br>Second half payment is due by June 15. |

| Single Full Payment | Due by April 30. |

If a deadline falls on a weekend or legal holiday, Colorado property tax payment deadlines are extended to the next business day. But miss a deadline, and the financial penalty is immediate: delinquent interest accrues on unpaid Colorado property taxes immediately after the respective payment deadlines.

If a property owner simply refuses to pay, the county will recoup its money by selling the debt. Unpaid Colorado real property taxes result in a county tax lien sale typically held in October or November.

The federal government sets the floor for civil rights in housing; Colorado builds a higher ceiling.

The Colorado Fair Housing Act enforces all protections recognized under the federal Fair Housing Act. The federal baseline protected classes include race, color, religion, national origin, sex, disability, and familial status.

Colorado expands this umbrella significantly. The Colorado Fair Housing Act designates the following additional protected classes:

- Marital status

- Sexual orientation

- Ancestry

- Creed

- Source of income

- Veteran or military status

The inclusion of "source of income" drastically changes the rental landscape. Because of this protected class, Colorado fair housing laws prohibit landlords from discriminating against tenants utilizing housing subsidies to pay rent (such as Section 8 vouchers). If the money is legal, the landlord must accept it.

Furthermore, Colorado extends these protections beyond residential limits. While federal fair housing laws apply exclusively to residential properties, commercial properties are covered under the antidiscrimination provisions of the Colorado Fair Housing Act.

When a homeowner defaults, the process of separating them from their property is highly regulated. You cannot simply evict a mortgagor; you must follow the statutory clockwork of a Colorado foreclosure.

The Foreclosure Timeline

The countdown begins long before the public finds out. A Notice of Default must be sent to a Colorado borrower at least 30 days before filing a Notice of Election and Demand. Furthermore, a Colorado lender cannot file a Notice of Election and Demand until the borrower is at least 120 days delinquent.

A Colorado foreclosure officially begins when the lender's attorney files a Notice of Election and Demand (NED) with the county Public Trustee. Once filed, the Public Trustee must record the Notice of Election and Demand with the County Clerk and Recorder within 10 business days of receipt.

Recording the NED triggers the scheduling of the foreclosure sale. The timelines vary based on the nature of the property, granting agricultural properties significantly more time to resolve their complex financial structures:

Foreclosure Sale Scheduling (from the date the NED is recorded):

- Non-agricultural residential property: The public trustee sets the foreclosure sale date between 110 and 125 calendar days.

- Agricultural property: The public trustee sets the foreclosure sale date between 215 and 230 calendar days.

The Rule 120 Hearing

Because Colorado uses nonjudicial foreclosures for Deeds of Trust, lenders cannot simply auction a home without minimal judicial oversight. Nonjudicial foreclosures in Colorado require a Rule 120 hearing to obtain a court order authorizing the property sale.

The primary purpose of the Rule 120 hearing is to verify that the debtor is not protected by the Servicemembers Civil Relief Act before authorizing a foreclosure sale—ensuring we do not sell the homes of deployed military personnel. A Rule 120 hearing gives the borrower a deadline of 21 to 35 days to respond to the lender's motion to authorize the foreclosure sale.

The Right to Cure and Redemption

Before the gavel falls, the owner has one last lifeline. A property owner in a Colorado foreclosure holds a statutory Right to Cure the monetary default prior to the foreclosure sale. Curing means paying the past-due amount, plus fees and interest, to bring the loan current—not paying off the entire loan balance.

To execute this:

- A property owner must file a Notice of Intent to Cure with the Public Trustee at least 15 calendar days before the scheduled foreclosure sale date.

- Foreclosure cure funds must be received in the Public Trustee's office by noon on the day before the foreclosure sale.

Once the sale occurs, the owner's rights evaporate. Colorado law eliminates the post-foreclosure sale redemption period for property owners. When the sale is done, the owner is done. Currently, only junior lienholders possess a statutory right to redeem a property after a Colorado foreclosure sale, allowing them to protect their financial interests if the primary lender forecloses.

The Colorado Foreclosure Protection Act

Because distressed homeowners are highly vulnerable to predatory investors who promise to "save" them while stealing their equity, the state enacted strict consumer protection laws. The Colorado Foreclosure Protection Act protects financially distressed homeowners from deceptive equity skimming business practices.

To trigger the stringent requirements of this Act, four specific conditions must be met:

- The Act applies to the sale of a residential property currently in the foreclosure process.

- Applicability of the Colorado Foreclosure Protection Act requires the seller to occupy the foreclosed property as a primary residence.

- Applicability of the Colorado Foreclosure Protection Act requires that the buyer does not intend to occupy the foreclosed property as a primary residence (meaning the buyer is an investor).

- Transactions qualifying under the Colorado Foreclosure Protection Act must use the specialized Contract to Buy and Sell Real Estate form designated for foreclosure protection.

To prevent high-pressure tactics where investors coerce panicked homeowners into signing away their equity, the Colorado Foreclosure Protection Act grants the seller a statutory right to cancel the purchase contract before closing. This cooling-off period ensures that a homeowner standing on the brink of financial ruin cannot be cornered into an abusive contract without the ability to step back, assess the math, and walk away.