IL Ownership, Taxes & Special Laws: Land Trusts, Homestead, Transfer Stamps & Liens

To master real estate in Illinois, one must recognize that a parcel of land is not merely a physical coordinate of dirt and bricks; it is a highly regulated bundle of rights, heavily modulated by state law. From the moment title is transferred, to the mechanisms of property taxation, down to how the land is physically subdivided and eventually inherited, Illinois applies a highly specific, statutory framework. For a real estate broker, this framework is not abstract legal trivia. It is the operating system of your daily transactions. Misunderstanding a transfer tax calculation or a broker’s lien timeline does not just cost a client money—it can entirely derail a closing.

When you look at public property records, you expect to see the name of the owner. But in Illinois, you will frequently see a bank or a trust company listed instead. This is the Illinois land trust, a unique legal instrument that allows a trustee to hold legal title to real estate while a beneficiary retains the true rights of ownership.

Think of an Illinois land trust like a safe deposit box for real estate. The bank (trustee) holds the box, but the beneficiary holds the key. The beneficiary of an Illinois land trust retains full control to manage the property, collect rents, and direct its sale. The trustee of an Illinois land trust can only act upon the written direction of the beneficiary.

Why would a property owner do this? Because it triggers a profound legal transformation: the beneficiary's interest in an Illinois land trust is legally classified as personal property, not real property.

This classification yields tremendous practical advantages:

- Privacy: An Illinois land trust creates privacy by keeping the beneficiary's name off public real estate records.

- Simplified Conveyance: Transferring the beneficial interest in an Illinois land trust does not require recording a new deed. The interest is transferred via assignment, just like selling shares in a company.

- Probate Avoidance: Beneficial interests in an Illinois land trust can be transferred outside of probate court upon the beneficiary's death.

- Asset Protection: If a judgment creditor files a lien against an individual, it typically attaches to all their real estate. However, an Illinois land trust protects the property title from automatic liens caused by judgments against a single beneficiary, because the title is held by the trustee, and the beneficiary merely owns personal property.

If a homeowner falls into severe debt, creditors will naturally seek to liquidate the homeowner’s assets to satisfy the judgments. Illinois homestead rights exist to prevent a family from being left entirely destitute by protecting a portion of home equity from attachment and forced sale by judgment creditors.

Crucial Distinction: A homestead claim does not protect an Illinois homeowner against foreclosure by the primary mortgage lender. If a borrower stops paying the mortgage that financed the home itself, the lender can and will foreclose. Homestead protects against unsecured judgment creditors (like medical debt or credit card judgments).

To claim an Illinois homestead exemption, a homeowner must reside on the property as a primary residence. An Illinois homeowner is not required to file a homestead declaration to claim the homestead exemption; the protection is automatic by virtue of occupying the property. This protection even extends beyond traditional houses—Illinois homestead rights extend to personal property used as a primary residence, such as a mobile home.

The Math of Homestead (2026 Limits):

- Effective January 1, 2026, the Illinois homestead exemption protects up to $50,000 of equity per single person.

- Married couples filing jointly can double the Illinois homestead exemption to protect up to $100,000 of equity as of 2026.

If the exempt property is sold, Illinois homestead rights protect the proceeds from the sale of an exempt property for up to one year after the sale, giving the seller time to reinvest that money into a new primary residence. Furthermore, Illinois statutes allow a surviving spouse to retain homestead protection while continuing to occupy the deceased spouse's home.

In Illinois, transferring title requires paying a toll, known as the real estate transfer tax. Payment of the Illinois real estate transfer tax is evidenced by affixing physical revenue stamps to the deed. An Illinois county recorder will reject a deed for recording unless the required transfer tax stamps are affixed, rendering the transaction incomplete.

The state and the county both take a piece of this tax, and the math is strictly standardized based on the "taxable value" of the property:

- The Illinois state real estate transfer tax rate is $0.50 per $500 of taxable value.

- Illinois counties charge a real estate transfer tax rate of $0.25 per $500 of taxable value.

- Therefore, the combined standard state and county real estate transfer tax in Illinois is $0.75 per $500 of taxable value.

The standard Illinois real estate transfer tax is customarily paid by the seller. However, calculating the taxable base requires attention to financing. The taxable base for the Illinois transfer tax is calculated by subtracting any assumed mortgage balance from the final sale price. If a buyer assumes a $50,000 mortgage on a $200,000 house, the transfer tax is only calculated on $150,000.

Local Additions and Exemptions: Home rule municipalities in Illinois can impose an additional local real estate transfer tax. Unlike the state/county tax, an Illinois municipal transfer tax can legally require payment from either the buyer or the seller depending on local ordinance.

Certain transactions—like transferring a deed to a land trust without money changing hands—are exempt from these taxes. However, exempt real estate transactions require a specific exemption statement on the face of the Illinois deed before the recorder will accept it.

In Illinois, property taxes operate on a delay: Illinois property taxes are paid in arrears. The tax bill a homeowner pays in 2026 is actually paying for the property's assessed value from 2025.

To lessen the burden on homeowners, the state offers several equalized assessed value (EAV) reductions:

- The Illinois General Homestead Exemption reduces the equalized assessed value of an owner-occupied primary residence.

- The Senior Citizens Homestead Exemption provides an equalized assessed value reduction for property owners aged 65 and older.

- The Senior Citizens Assessment Freeze Homestead Exemption freezes the assessed value for seniors meeting specific low-income limits, shielding them from rising property values.

- Furthermore, Illinois provides permanent property tax exemptions for qualifying disabled persons, and provides property tax exemptions for qualifying returning military veterans.

The Tax Sales: When Owners Don't Pay

When a homeowner fails to pay their property taxes, the local government does not immediately evict them. Instead, it sells the debt. The Illinois Annual Tax Sale auctions the right to pay the prior year's delinquent property taxes to an investor. In exchange, a tax buyer at an Illinois Annual Tax Sale receives a tax certificate representing a lien on the property.

If a property is severely delinquent, the state escalates the process. The Illinois Scavenger Sale auctions taxes on properties with three or more years of delinquent property taxes.

Can the homeowner save their property after a tax sale? Yes. Properties purchased at an Illinois tax sale can be redeemed by the original owner within a statutory redemption period by paying the back taxes plus high interest.

- The standard statutory redemption period for an Illinois residential property with six or fewer units is 30 months from the tax sale date.

- The statutory redemption period for Illinois commercial properties and vacant lots is heavily accelerated, lasting only six months from the tax sale date.

When a property owner decides to subdivide a large tract of land into smaller parcels, they cannot simply draw lines on a napkin and start selling. The Illinois Plat Act strictly regulates the subdivision of land into smaller parcels to ensure boundaries, roads, and utilities are mapped properly.

A survey and subdivision plat are required when an owner divides Illinois land into two or more parts with any part being less than five acres. This mapping is a highly technical process; an Illinois subdivision plat must be prepared by a Registered Land Surveyor.

There are exceptions to this rule. Subdividing Illinois land into parcels of five acres or larger does not require a subdivision plat. However, this loophole comes with a strict condition: the five-acre Plat Act exemption only applies if the subdivision does not involve any new streets or easements of access. If the developer needs to build a new road to reach those 5-acre lots, a full plat is triggered regardless of parcel size.

To enforce this, county recorders require a paper trail. A Plat Act Affidavit must accompany deeds submitted for recording to verify compliance with the Illinois Plat Act, confirming whether the transaction falls under the Act or an exemption.

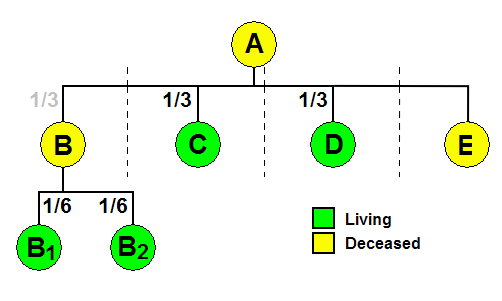

When an Illinois resident dies without a valid will, their property does not evaporate; it passes according to statutory rules. Intestate succession applies when an Illinois resident dies without a valid will.

Illinois law mandates a rigid flow of inheritance:

- Under Illinois intestacy law, a surviving spouse inherits the entire estate if the decedent leaves no descendants.

- If an intestate Illinois decedent leaves both a surviving spouse and descendants, the spouse receives one-half of the estate, and the descendants receive one-half of the estate per stirpes (meaning by representation, where children step into the shoes of a deceased parent).

- If an intestate Illinois decedent leaves descendants but no surviving spouse, the descendants inherit the entire estate per stirpes.

Family Definitions: In the eyes of Illinois intestacy law, blood and legal paperwork are what matter. Adopted children receive the same intestate share as biological children under Illinois law. Conversely, stepchildren and foster children do not inherit under Illinois intestate succession laws unless legally adopted.

The Power of Ownership Structure: It is vital to remember that intestacy only governs the probate estate. Joint tenancy property passes outside of Illinois probate proceedings. If two people own a home in joint tenancy and one dies, the survivor absorbs the deceased's share automatically, bypassing the intestacy statutes entirely.

Brokers expend massive amounts of time and capital to execute transactions. In the residential world, commission disputes are generally settled in court after the fact. But in the commercial sector, the law provides a much heavier hammer.

The Illinois Commercial Real Estate Broker Lien Act allows a broker to place a lien on property for an unpaid commission. This gives the broker immense leverage, as a lien clouds the title and effectively halts the sale or refinancing of the property.

Limitations and Scope: The Illinois Broker Lien Act applies exclusively to commercial real estate transactions. It explicitly excludes two major categories:

- The Illinois Broker Lien Act excludes residential properties containing one to six units.

- The Illinois Broker Lien Act excludes real estate classified as farmland for assessment purposes.

The Mechanics of the Lien: To wield this power, a broker must adhere to strict procedural rules. First, a commercial broker must possess a written agreement signed by the owner to file a valid lien in Illinois. A handshake agreement will not suffice.

Second, the timing is unforgiving:

- An Illinois commercial broker lien must be recorded before the actual conveyance or transfer of the real estate.

- A commercial broker must record a notice of lien in the county recorder's office where the real estate is located.

- If the commission involves a lease rather than a sale, an Illinois broker's claim for lien on a commercial lease must be recorded within 90 days after the tenant takes possession.

Attachment and Enforcement: When does this lien actually take effect? An Illinois commercial broker's lien attaches to the real estate on the exact date the notice of lien is recorded. Crucially, an Illinois commercial broker's lien does not relate back to the date of the written brokerage agreement. If another lien (like a mortgage) is recorded between the signing of the broker's agreement and the recording of the broker's lien, the mortgage takes priority.

Once recorded, the broker must actively enforce it. An Illinois broker must mail a copy of the recorded commercial lien to the property owner within 10 days of recording. Finally, the lien does not last forever; an Illinois broker must commence a lawsuit to foreclose a commercial real estate lien within two years of recording the lien, or the right is forever extinguished.