Consequences of Non-Compliance

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Examine the legal foundation of a New York real estate brokerage, and you will find a delicate balance of autonomy and liability. In the vast majority of cases, a New York real estate salesperson is typically classified as a statutory non-employee for tax purposes. This classification is the bedrock of the real estate industry’s financial structure, allowing agents the freedom of entrepreneurs while sparing brokers the heavy administrative machinery of traditional employment. However, this status is not a natural law; it is a legally engineered privilege granted under specific conditions. When a broker misunderstands the mechanics of this relationship and crosses the line into employer territory, the resulting structural collapse brings catastrophic financial, tax, and regulatory consequences for both parties.

To navigate real estate law effectively, you must understand not only the rules of the independent contractor relationship but the precise, cascading penalties that trigger when those rules are violated.

Under federal tax law, Internal Revenue Code Section 3508 provides a "safe harbor" for classifying real estate agents as independent contractors. When a broker anchors their business practices within this safe harbor, the IRS will not challenge the worker’s classification.

To maintain this safe harbor, the relationship requires strict, ongoing documentation. Under New York law, a written independent contractor agreement must be executed at least every fifteen months to maintain a salesperson's non-employee status. This is not mere bureaucratic friction; it is a rigid legal timer. Failure to maintain a current written independent contractor agreement exposes the real estate broker to automatic employee classification risks, stripping away the protections of the safe harbor instantly.

When the safe harbor holds, the financial reporting is straightforward: an independent contractor real estate salesperson receives an IRS Form 1099-NEC at the end of the tax year for income reporting, representing gross commissions paid without any taxes withheld.

The most common way a broker accidentally torpedoes their safe harbor protection is by exerting too much operational dominance over an agent.

Worker Misclassification occurs when a real estate broker treats a salesperson as an independent contractor on paper, while exercising the behavioral control of an employer in reality.

The law looks at the reality of the relationship, not just the title on the contract. If you treat someone like an employee, the government will tax you like an employer.

How does this happen in a real estate office? Often, it stems from a well-meaning broker trying to increase office productivity or enforce brand standards. However, a real estate broker loses independent contractor safe harbor protection if the broker mandates attendance at sales meetings. Similarly, a real estate broker loses independent contractor safe harbor protection if the broker dictates the specific hours a salesperson must work (such as forcing an agent to sit at the front desk for specific "floor time" shifts under threat of penalty). Autonomy is the price the broker pays for tax relief; if the broker reclaims that autonomy, they must pay the taxes.

If a labor board or tax authority audits a brokerage and legally deems a salesperson an employee, the financial repercussions for the sponsoring broker are immediate, retroactive, and severe.

1. Retroactive Tax Withholding

In a standard independent contractor setup, agents pay their own taxes. If a real estate salesperson is legally deemed an employee, the sponsoring broker must retroactively withhold federal income taxes from the salesperson's earnings. Furthermore, the sponsoring broker must retroactively withhold state income taxes from the salesperson's earnings. Because the money has already been paid out to the agent as commission, the broker is often left footing this massive bill directly to the tax authorities.

2. The Burden of Payroll Taxes

Employment is a shared tax burden. Reclassification of a real estate salesperson to an employee requires the sponsoring broker to pay the employer portion of Social Security taxes, as well as the employer portion of Medicare taxes. These are not forward-looking requirements; they apply backward to every dollar earned during the misclassified period.

3. Unemployment Insurance Costs

Independent contractors do not get unemployment benefits. Employees do. Therefore, upon reclassification, a real estate broker becomes liable for Federal Unemployment Tax Act (FUTA) contributions. Simultaneously at the state level, the real estate broker must pay New York State unemployment insurance premiums if salespersons are legally reclassified as employees.

4. Punitive Action and Regulatory Fines

The IRS does not look kindly upon misclassification, viewing it as a form of tax evasion. A real estate broker faces financial penalties from the Internal Revenue Service for failing to withhold payroll taxes due to worker misclassification. To compound the pain, tax authorities will charge a real estate broker interest on unpaid back taxes resulting from the misclassification of a salesperson. The longer the misclassification went unnoticed, the heavier the interest burden.

Beyond the IRS, the state licensing body will intervene. The New York Department of State (DOS) can impose disciplinary actions against a real estate broker for violating independent contractor regulations, which may include license suspension or revocation.

5. Labor Law and Civil Lawsuits

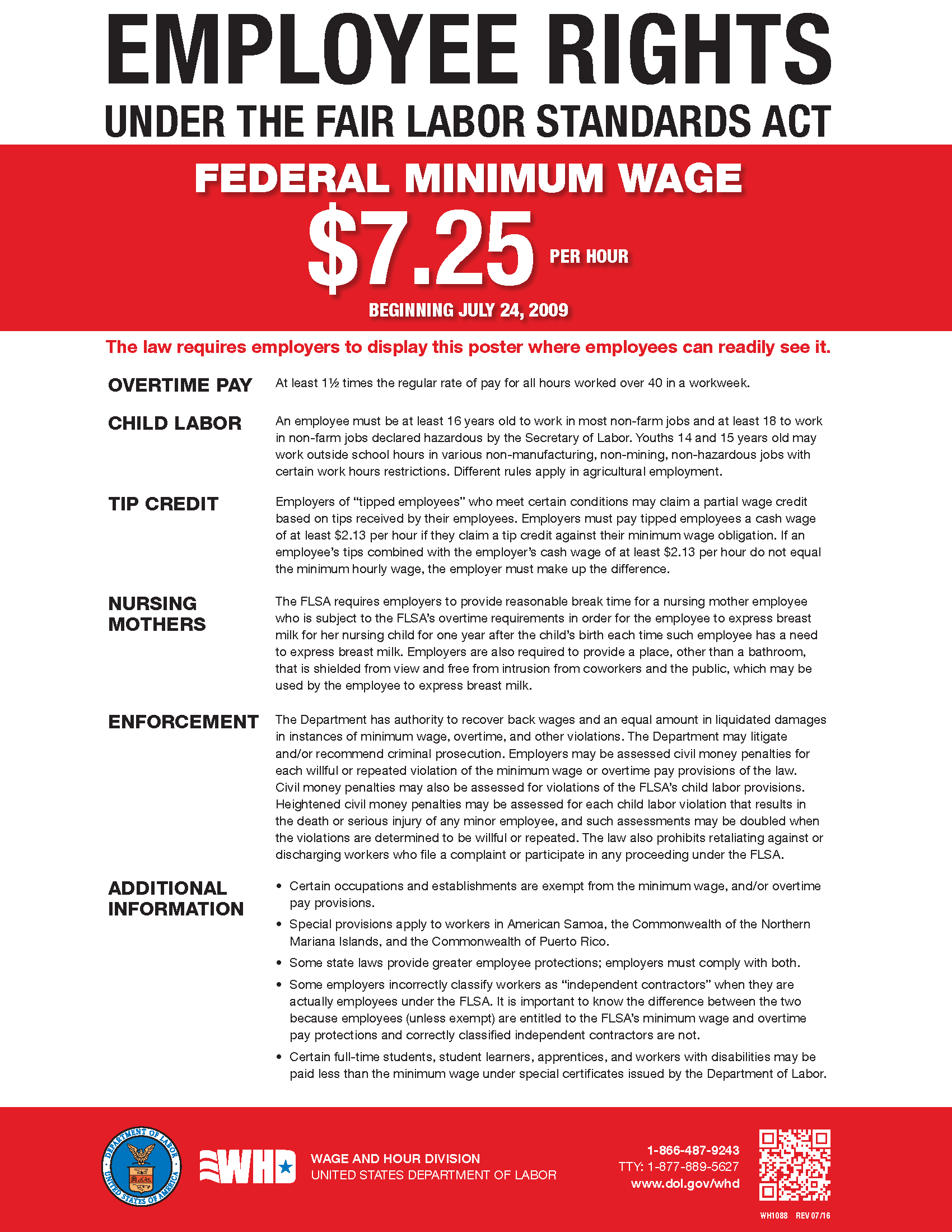

The moment an agent becomes an employee, the protective shield of the Fair Labor Standards Act (FLSA) applies.

- A real estate broker becomes subject to minimum wage requirements under the Fair Labor Standards Act if a salesperson is legally deemed an employee.

- A real estate broker must comply with overtime pay requirements under federal and state labor laws if a salesperson is legally deemed an employee.

This opens a devastating vector for litigation. A real estate broker may face civil lawsuits from misclassified salespersons seeking retroactive compensation for unpaid minimum wage and overtime for the hours they spent working on deals that perhaps never closed. Furthermore, under federal law, a real estate broker may be legally required to provide standard employee health and retirement benefits to a misclassified salesperson, matching whatever benefits are offered to the brokerage's actual administrative staff.

When a broker is audited and agents are reclassified, the agents often assume they are merely bystanders to their broker's misfortune. This is a profound misconception. The reclassification of a salesperson triggers a highly disruptive tax nightmare for the agent.

The Loss of the Entrepreneurial Tax Structure

As an independent contractor, an agent operates as a business. A real estate salesperson reclassified as an employee loses the ability to report business income on IRS Schedule C.

Why does this matter? Schedule C is where the magic of real estate tax strategy happens. By losing this form, a real estate salesperson reclassified as an employee loses the ability to deduct unreimbursed business expenses. Think about the daily reality of an agent: the thousands of dollars spent on staging, Zillow leads, gas mileage, client dinners, and professional photography. As an independent contractor, these expenses reduce taxable income. As a reclassified W-2 employee, these expenses are swallowed entirely by the agent with no tax relief, drastically increasing their effective tax burden.

Changes to Income Mechanics

Upon reclassification, the entire flow of money changes.

- A reclassified real estate salesperson must receive an IRS Form W-2 for wage reporting instead of a Form 1099.

- Instead of receiving a gross commission check at the closing table, a real estate salesperson reclassified as an employee will have income taxes automatically deducted directly from commission payments.

There is one minor financial offset for the agent: because they are now an employee, a real estate salesperson reclassified as an employee is no longer required to pay the self-employment tax (the roughly 15.3% tax that independent contractors pay to cover both the employer and employee halves of Medicare and Social Security). The broker is now forced to absorb the employer half.

The Bureaucratic Fallout

Finally, the IRS requires the historical record to be corrected. Both the real estate broker and the salesperson must file amended tax returns if the salesperson is retroactively reclassified as an employee. For an agent, this means paying an accountant to tear up years of previous tax filings, removing Schedule C deductions, altering income classifications, and potentially paying unexpected tax discrepancies.

| Feature / Responsibility | Valid Independent Contractor | Reclassified Employee (Non-Compliance) |

|---|---|---|

| Income Reporting | IRS Form 1099-NEC | IRS Form W-2 |

| Tax Deductions | Business income and expenses reported on Schedule C | Loses ability to deduct unreimbursed business expenses (No Schedule C) |

| Tax Withholding | Agent pays estimated taxes quarterly | Broker must automatically deduct federal and state income taxes from commissions |

| Social Security & Medicare | Agent pays full Self-Employment Tax | Agent no longer pays Self-Employment Tax; Broker pays employer portion |

| Broker Financial Burden | Pays gross commission only | Liable for retroactive FUTA, NYS unemployment premiums, IRS penalties, and interest |

| Labor Law Application | FLSA does not apply | Broker subject to FLSA minimum wage, overtime pay, and standard employee health/retirement benefits |

| NY Written Agreement | Must execute every 15 months | Failure to maintain exposes broker to automatic employee classification |

Understanding these mechanics is vital for any real estate professional. For a broker, it is the difference between a thriving business and catastrophic insolvency. For a salesperson, it is the difference between true financial autonomy and being caught in the gears of a legal reclassification that strips away the very tax advantages that make selling real estate so lucrative. Keep the contracts current, respect the boundaries of behavioral control, and ensure the safe harbor remains intact.