Co-op Documents and Board Packages

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Purchasing a New York City cooperative is not a real estate transaction in the traditional sense; it is an acquisition of corporate stock intertwined with a highly scrutinized application to a private micro-community. When a client transfers millions of dollars to close on a cooperative, they are not buying bricks, mortar, or a deed. Rather, a cooperative buyer purchases shares of stock in a corporation rather than purchasing real property.

To navigate this market successfully, a real estate salesperson must fundamentally understand the legal and financial machinery that makes a cooperative function. You are not just selling an apartment; you are guiding a buyer through a corporate merger of one. Your ability to anticipate the board's financial parameters, curate an airtight application, and shepherd the transaction through closing will be the defining metric of your professional competence.

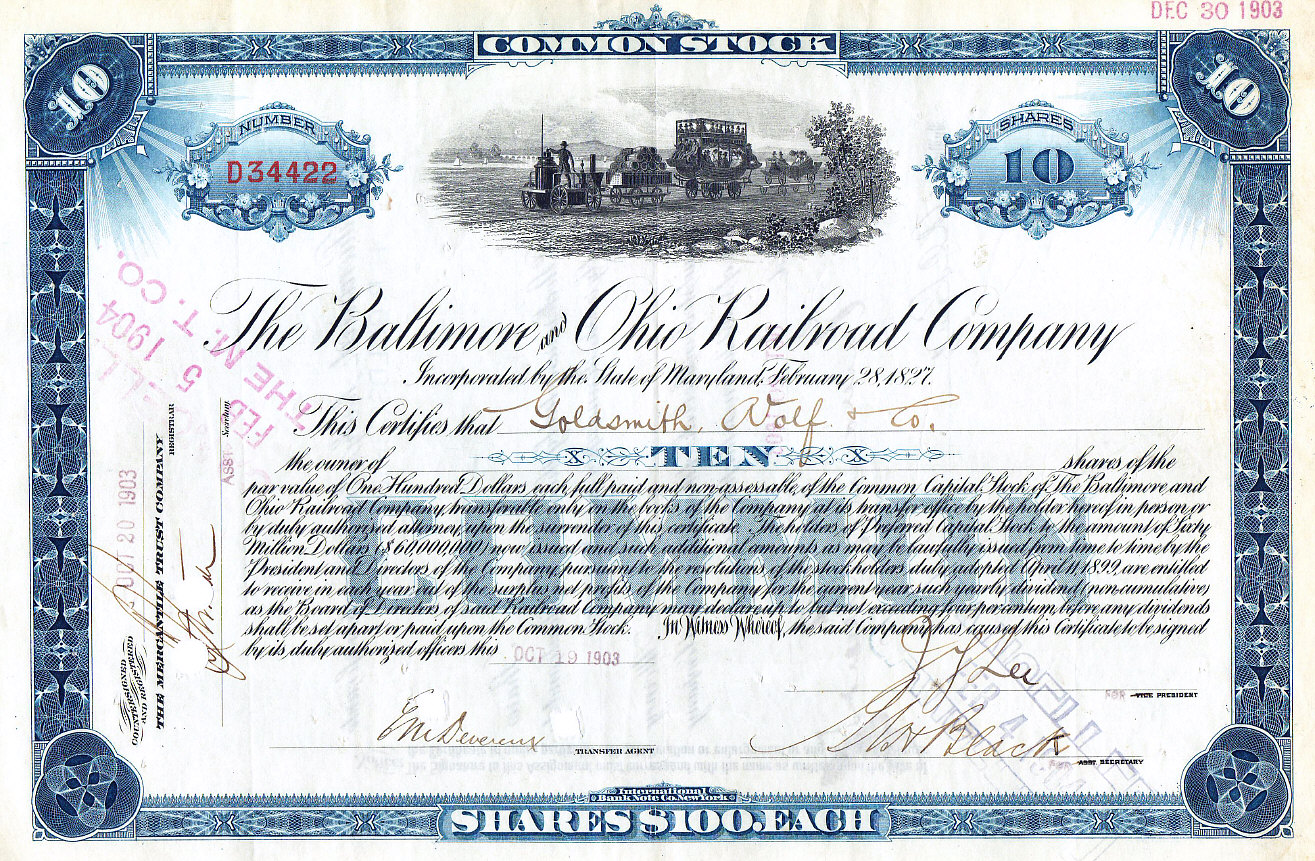

To understand the cooperative closing process, we first have to understand what exactly your client is buying.

Because the entire building is owned by a single cooperative corporation, ownership of shares in a cooperative corporation grants the shareholder a proprietary lease. This is the vital link between corporate stock and physical habitation: a proprietary lease gives a cooperative shareholder the right to occupy a specific apartment unit.

At the closing table, you will not see a deed. Instead, a stock certificate serves as proof of ownership of shares in a cooperative corporation.

Once inside, the shareholder's financial obligation to the building takes the form of monthly maintenance. Cooperative maintenance fees cover the shareholder's portion of the building's operating expenses and the building's underlying mortgage. This dual structure—funding both the boiler repairs and the massive mortgage the corporation holds on the building itself—is why cooperative boards are obsessively protective of their financial stability.

The Role of the Sponsor

Not every unit in a building is subject to the standard board gauntlet. When a building is originally transitioned from rentals to a co-op, there is a sponsor, which is the developer or entity that converts a building into a cooperative corporation. Often, the sponsor retains ownership of units occupied by rent-stabilized tenants. The entities that hold these specific shares are known as holders of unsold shares, and they are generally exempt from board approval for apartment sales or subleases. For your day-to-day practice, identifying a "sponsor unit" means identifying a transaction with significantly less friction for your buyer.

A cooperative is a self-governing ecosystem. Before a client even submits an offer, their legal counsel must dissect the building's governing documents.

Due Diligence Directive: A buyer's attorney reviews the cooperative corporation's audited financial statements to assess the building's financial health. If the reserve fund is depleted or the underlying mortgage is ballooning, the buyer is purchasing a liability, not an asset.

The daily and structural governance of this ecosystem is split into two primary documents:

| Document Type | Function and Scope |

|---|---|

| Cooperative By-laws | Dictate the governance of the corporation, including board member elections and shareholder voting rights. This is the constitutional framework of the building. |

| Cooperative House Rules | Dictate daily living policies such as pet ownership, noise restrictions, and trash disposal. This is the behavioral framework of the building. |

Altering the Space

If your buyer plans to knock down a wall or update a kitchen, they cannot simply hire a contractor and start swinging a hammer. They must execute an alteration agreement, which is a contract between a cooperative corporation and a shareholder regarding renovations to an apartment.

00087_Rear_Gut_JUNE_1971(37507228366).jpg)

This agreement protects the building's structural integrity and the peace of the neighbors. Specifically, an alteration agreement establishes allowable construction hours for a cooperative apartment renovation and strictly mandates that a shareholder provide proof of contractor insurance before commencing apartment renovations.

If the buyer’s offer is accepted, the real work begins. You must compile the cooperative board package, a comprehensive application detailing a prospective buyer's financial and personal background.

Think of the board package as a financial x-ray. The board is looking for any hidden fractures that might cause the buyer to default on their maintenance payments. A typical cooperative board package requires multiple years of the buyer's federal and state tax returns, alongside employment verification letters detailing the applicant's salary and bonus structures.

The board also demands a psychological profile, which is why packages generally require both personal and professional letters of reference. They are looking for assurance that the applicant is financially solvent and will be a harmonious neighbor.

The Crucial Financial Parameters

As an agent, you must act as an underwriter before the board ever sees the file. Cooperative boards heavily evaluate a prospective buyer's debt-to-income ratio during the application process.

Debt-to-Income Ratio (DTI): The debt-to-income ratio measures a buyer's monthly debt obligations against the buyer's gross monthly income.

If your buyer makes $10,000 a month gross, and their projected mortgage, maintenance, and student loans total $2,500, their DTI is 25%. This is critical because many New York cooperative boards strictly require a debt-to-income ratio of 25 to 30 percent or lower. If your client is at 35%, submitting the package is often a waste of time.

Furthermore, the board wants to know what happens if the buyer loses their job the day after closing. This is measured by post-closing liquidity, which refers to the amount of cash reserves a buyer must have remaining after paying the down payment and closing costs. Cooperative boards often require buyers to have post-closing liquidity equal to one to two years of monthly maintenance and mortgage payments.

Cooperative board members review the complete board package before inviting the prospective buyer to an interview. If the package is weak, there is no interview—just a rejection.

If invited, the board interview is the final step in the cooperative application process. Real estate agents prepare cooperative buyers for board interviews by conducting mock interviews and reviewing the submitted application. Your job is to ensure the buyer knows their own financial statement inside out and understands the unspoken etiquette of the interview (e.g., answer questions directly, do not over-volunteer information, and never demand building upgrades).

The Ultimate Veto

Co-op boards wield extraordinary power. A cooperative board holds the legal right to reject any applicant for any reason except for legally prohibited discriminatory reasons (such as race, religion, or familial status, as outlined by Fair Housing laws).

Perhaps more startling to new agents: a cooperative board is not legally required to disclose the reason for rejecting a prospective buyer. You may spend months curating a deal, only to receive a one-sentence rejection letter with zero explanation. This absolute authority is why pre-qualifying your buyers against the building's historical standards is the most important service you provide.

When you finally reach the closing table, several unique mechanics come into play that differ wildly from a condominium or townhouse closing.

The Aztech Recognition Agreement

If your buyer is taking out a mortgage to buy their shares, the bank faces a unique risk. Because the buyer is purchasing shares, not real property, the bank's collateral is the stock. But if the buyer stops paying their co-op maintenance, the co-op corporation has a first lien on the shares and could foreclose, wiping out the bank's collateral.

To solve this standoff, the parties utilize a recognition agreement, which is a three-way contract between a cooperative corporation, a shareholder, and the shareholder's lender. Specifically, the Aztech Recognition Agreement is the standard document used in New York to formalize a lender's rights in a cooperative loan.

This document protects the bank by ensuring the cooperative notifies the lender if the shareholder falls behind on maintenance. Ultimately, a recognition agreement outlines the lender's rights in the event a shareholder defaults on cooperative maintenance payments, often allowing the bank to step in and pay the maintenance to protect its underlying collateral.

The Flip Tax

During the closing, capital must be collected to secure the building's future. You will frequently encounter a flip tax, which is a fee imposed by a cooperative board on the sale of a cooperative apartment to build the building's reserve fund. Despite the name, it is a transfer fee, not a government tax. Historically and customarily, a flip tax is typically paid by the seller at the closing of a cooperative apartment transaction, though this is occasionally negotiated.

The Delivery of Shares

The culmination of the transaction relies on the transfer of physical paper. Cooperative closing transactions require the physical delivery of the original stock certificate to the new shareholder or their lender.

If it is an all-cash deal, your buyer walks out with their stock certificate and proprietary lease. However, if a cooperative buyer requires a mortgage, the original stock certificate and proprietary lease are held by the lender until the loan is fully repaid. The bank locks these documents in a vault; they are the ultimate proof of collateral.

By mastering these layers—from the microscopic review of the board package to the structural mechanics of the Aztech agreement—you transform yourself from a tour guide into a true real estate advisor. You are not just opening doors; you are orchestrating the legal and financial transfer of shares within New York's most exclusive corporate structures.