Predatory Lending Overview

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

A mortgage is a mathematical instrument of leverage, allowing an individual to control a high-value physical asset using a fraction of the necessary liquid capital. When structured correctly, it is the primary engine of wealth creation in American households. However, when the parameters of this financial instrument are intentionally engineered to fail, it ceases to be a tool of leverage and becomes a mechanism for wealth extraction. This is the realm of predatory lending. For a real estate professional, understanding the mechanics of these loans is not merely academic; it is vital to protecting the integrity of your transactions and the financial survival of your clients.

To understand predatory lending, we must first isolate it from legitimate risk-based financing. A common misconception in real estate is that any expensive loan is predatory. This is mathematically false.

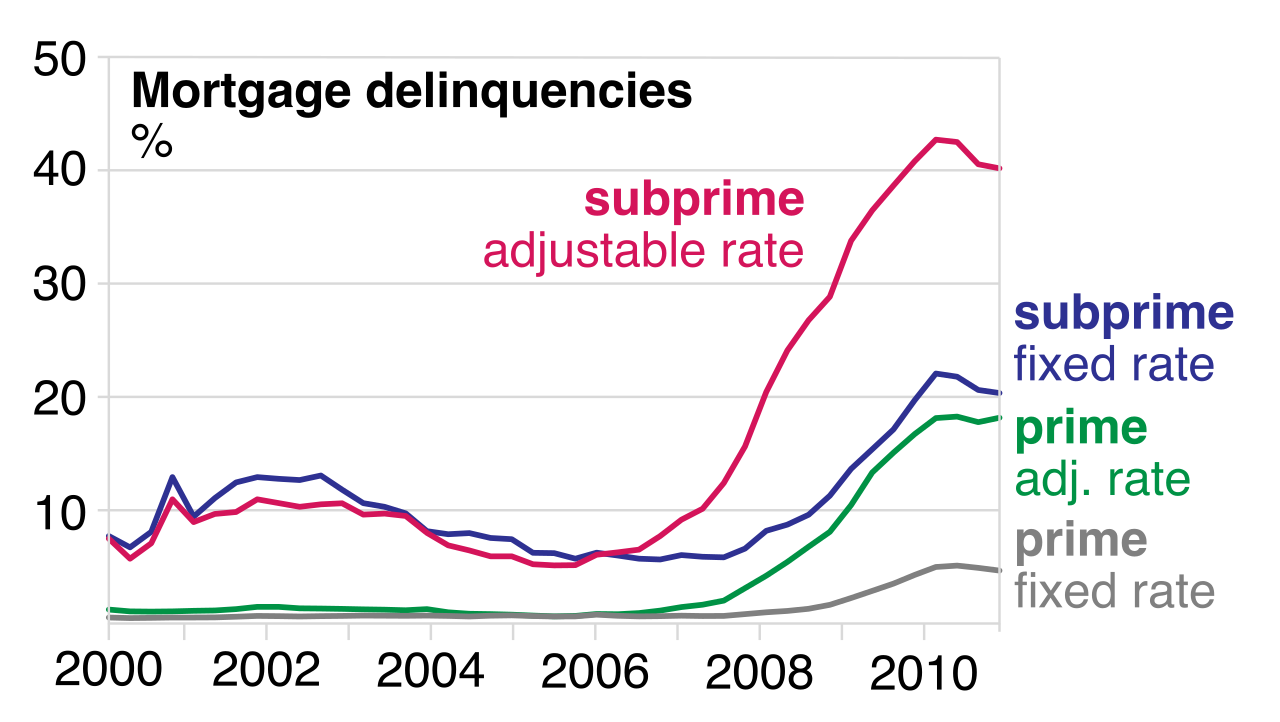

A subprime loan is a mortgage issued to borrowers with low credit scores or limited credit histories. Because these borrowers present a statistically higher risk of defaulting on their payments, capital is more expensive for them to acquire. Consequently, subprime loans carry higher interest rates to compensate lenders for increased default risk.

Think of this in terms of physical insurance: a property built in a known flood zone costs more to insure than one sitting on high ground. The premium reflects the probability of a structural failure. In the same way, subprime lending is a legitimate financial practice and is not inherently predatory. It provides a necessary bridge to homeownership for individuals who do not fit the pristine parameters of conventional, prime lending.

However, a critical vulnerability exists here: Predatory lending heavily occurs within the subprime mortgage market. Because subprime borrowers often lack financial literacy, have fewer borrowing options, or are desperate to secure housing, they are easily exploited.

Predatory lending is the practice of imposing unfair or abusive loan terms on a borrower.

Rather than pricing a loan to manage risk, a predatory lender structures a loan to guarantee extraction. To achieve this, predatory lenders frequently target vulnerable populations such as the elderly or low-income individuals, utilizing their lack of market leverage against them.

Predatory lending is not a single act; it is a sequence of strategic deceptions engineered to trap the borrower. As a real estate salesperson, you will often see the symptoms of these mechanics before closing.

Origination Tactics: Steering and Bait-and-Switch

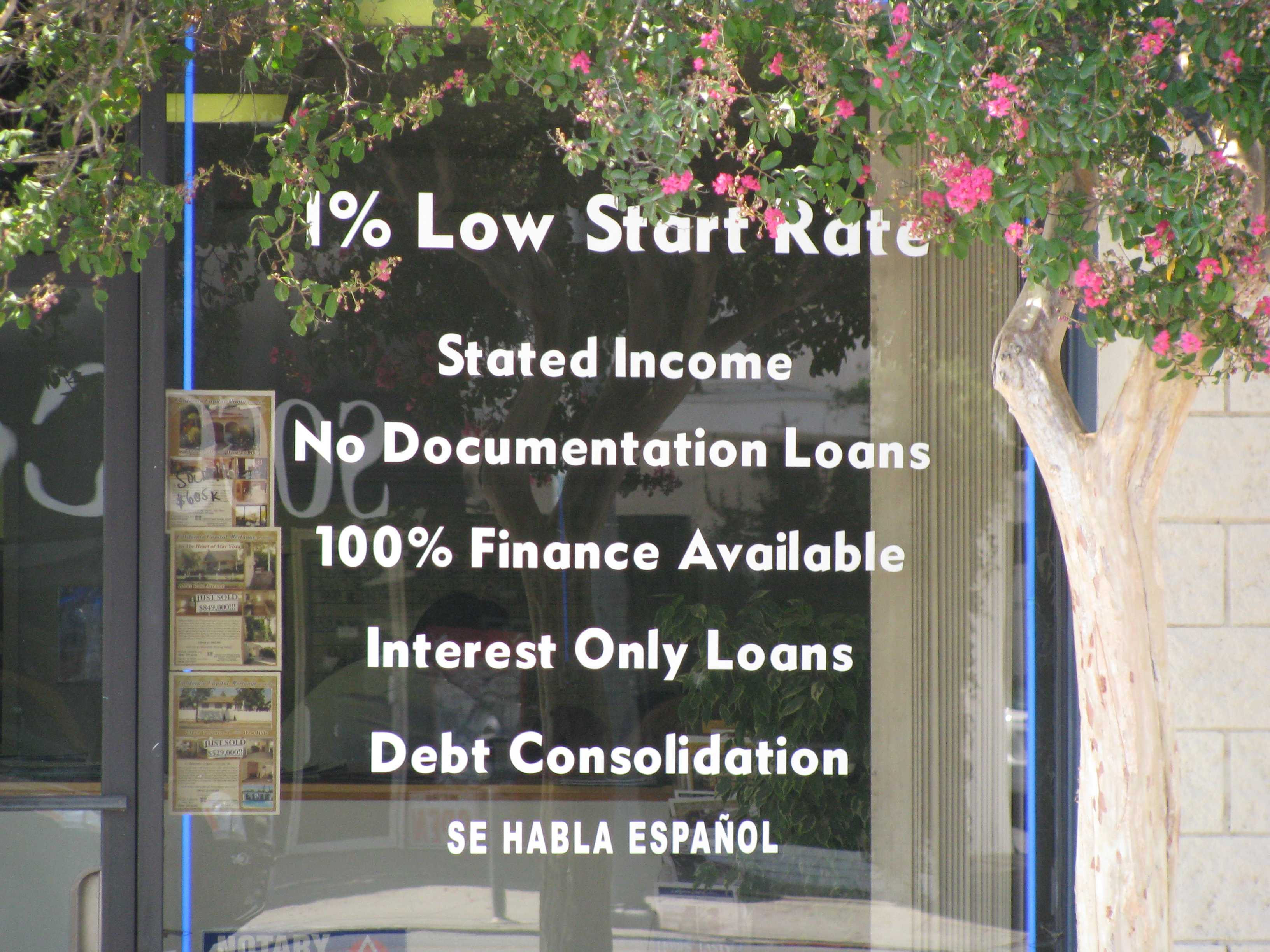

The trap often opens at the loan application phase. Steering in mortgage finance occurs when a lender directs a borrower into a more expensive loan product than the borrower actually qualifies for. Imagine a buyer who qualifies for a standard 30-year fixed-rate mortgage at a fair market rate, but the loan officer convinces them to take a complex, high-interest adjustable-rate mortgage because it yields a higher commission for the broker.

This is frequently coupled with another deceptive tactic at the closing table. Bait-and-switch lending occurs when a lender offers a low interest rate initially and changes the terms to a much higher rate at closing. When your client is sitting at the closing table, boxes packed in moving trucks outside, the psychological pressure to sign the paperwork—even if the numbers have mysteriously inflated—is immense. The lender relies on this exact pressure.

Bloating the Balance: Packing, Hidden Fees, and Negative Amortization

Once the borrower is committed, the lender inflates the cost of the loan from the inside out.

- Hidden fees are undisclosed costs secretly added to the principal balance of a mortgage.

- Loan packing is the practice of adding unnecessary products like credit life insurance into the mortgage balance without the borrower's full understanding.

By burying these costs into the financed amount, the borrower pays interest on fraudulent charges for decades.

The most mathematically destructive tool in the predatory arsenal, however, is the manipulation of the amortization schedule. In a normal mortgage, every payment chips away at the principal. Negative amortization occurs when monthly mortgage payments do not cover the full amount of interest due.

If a borrower owes $1,500 a month in interest, but the lender allows a "minimum payment" of only $1,000, the remaining $500 does not disappear. It is added to the total debt. Predatory lenders use negative amortization to continuously increase the borrower's principal debt balance over time. The borrower pays diligently every month, only to watch the amount they owe grow larger, effectively trapping them in the property.

The ultimate goal of a predatory lender is not simply to collect interest; it is to harvest the equity of the home and extract continuous fees through a manufactured crisis. This is executed through a three-part mechanical sequence: the balloon payment, the flip, and the strip.

1. The Catalyst: The Unwarranted Balloon Payment

A balloon payment is an unusually large lump sum due at the end of a mortgage term. While balloon payments have legitimate uses in commercial real estate or short-term bridge loans, they are weaponized in the residential sector. Predatory lenders use unwarranted balloon payments to force a borrower into defaulting or refinancing the loan. The borrower reaches the end of a short loan term and suddenly owes a $250,000 lump sum they cannot possibly pay.

2. The Extraction: Loan Flipping

Faced with imminent default due to the balloon payment, the borrower panics. The lender graciously offers to "help" by refinancing the debt. However, refinancing a balloon payment loan generates additional closing costs and fees for the predatory lender.

This creates a vicious, perpetual cycle. Loan flipping involves a lender repeatedly refinancing a borrower's mortgage. Every time the loan is flipped, new origination fees, appraisal fees, and administrative costs are financed into the new loan balance. Loan flipping generates high fee income for the lender without providing any financial benefit to the borrower.

3. The End Game: Equity Stripping

As the loan is flipped and the balance artificially inflates through negative amortization and packed fees, the borrower's equity—the true ownership of the home—is systematically erased. Equity stripping occurs when a lender issues a mortgage based solely on the equity of the property rather than the borrower's ability to repay the debt.

The lender does not care that the borrower's income cannot sustain the new, inflated mortgage payments. They know the home itself holds the value. The mathematical conclusion is inescapable: Equity stripping leads to foreclosure when the borrower inevitably defaults on the unaffordable loan payments. The lender seizes the asset, sells it, and keeps the stripped equity.

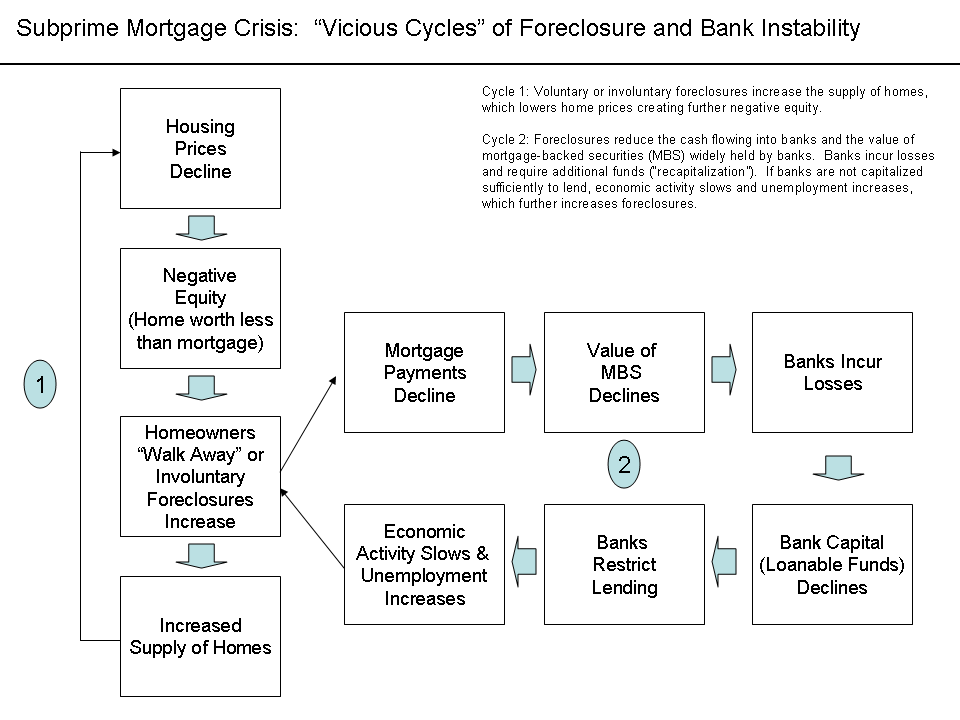

Real estate operates in a strictly interconnected ecosystem. The devastation of predatory lending does not stop at the property line of the victim.

Predatory lending practices directly contribute to higher regional foreclosure rates. When a concentrated area is targeted by predatory institutions, multiple homes default simultaneously. For a real estate salesperson, the implications of this are severe: Foreclosures resulting from predatory lending decrease surrounding neighborhood property values.

A foreclosed, vacant home becomes a blight. It attracts vandalism, deteriorates structurally, and most importantly, serves as a toxic "comparable sale" (comp) that appraisers must use when evaluating neighboring homes. A single predatory loan can suppress the appraisal values of an entire block, halting healthy real estate transactions and eroding the generational wealth of the community.

Because the free market cannot self-regulate predatory extraction without catastrophic economic consequences, specific legislative shields have been enacted at both the federal and state levels.

Federal Defenses

| Legislation | Core Function against Predatory Practices |

|---|---|

| Truth in Lending Act (TILA) | Operates on the principle of transparency. The Truth in Lending Act requires lenders to accurately disclose the annual percentage rate and total financial costs of a mortgage. It forces the true cost of capital out of the shadows. |

| Home Ownership and Equity Protection Act (HOEPA) | The Home Ownership and Equity Protection Act is a federal law enacted to combat abusive practices in refinances and closed-end home equity loans. Because equity stripping happens during refinancing, HOEPA targets this vulnerability. Furthermore, the Home Ownership and Equity Protection Act establishes strict disclosure requirements for high-cost mortgages, ensuring borrowers are heavily warned before signing. |

New York State Defenses

In New York, the regulatory environment is particularly hostile to predatory lenders, providing robust defenses that real estate professionals must understand.

New York Banking Law Section 6-l This is the primary state-level mechanism designed to dismantle the predatory machine. New York Banking Law Section 6-l restricts abusive practices in high-cost home loans. It neutralizes the lender's ability to extract wealth through fees by setting strict mathematical caps: New York Banking Law Section 6-l prohibits the financing of points and fees exceeding six percent of the total loan amount.

Furthermore, to stop the endless cycle of refinancing fees, New York Banking Law Section 6-l explicitly forbids loan flipping. If a refinance provides no tangible net benefit to the borrower, it is illegal in the State of New York.

The Home Equity Theft Prevention Act (HETPA) Predatory behavior often attracts secondary scavengers. When a borrower goes into foreclosure, they are publicly exposed to "equity purchasers" who offer to "save" them, often tricking the homeowner into signing over the deed for pennies on the dollar. The Home Equity Theft Prevention Act is a New York law protecting distressed homeowners from predatory equity purchasers. To prevent panic-induced exploitation, the Home Equity Theft Prevention Act requires specific disclosures and cancellation rights in contracts involving homes currently in foreclosure. This provides a legally mandated cooling-off period for the distressed seller.

As a New York real estate salesperson, you sit at the intersection of the buyer, the property, and the capital. You will review loan estimates. You will sit at closing tables. You will watch the body language of clients who are suddenly faced with numbers they do not understand.

While you are an expert in real estate, you are not a licensed attorney, nor are you a mortgage underwriter. Attempting to legally dissect a fraudulent loan on behalf of your client crosses the boundary into the unauthorized practice of law.

However, your fiduciary duty of reasonable care requires vigilance. When you observe the architectural markers of a trap—a sudden, unexplained spike in the interest rate at closing, unwarranted balloon payments, or aggressive pressure to refinance a distressed property—you must act. Real estate licensees must advise clients to consult a real estate attorney if predatory loan terms are suspected.

Your value as a real estate professional is not just in opening doors and negotiating purchase prices. Your ultimate value is safely guiding your client through an intricate, sometimes dangerous financial ecosystem. By recognizing the mechanics of predatory lending, you transition from a simple salesperson into an indispensable guardian of your client's financial future.