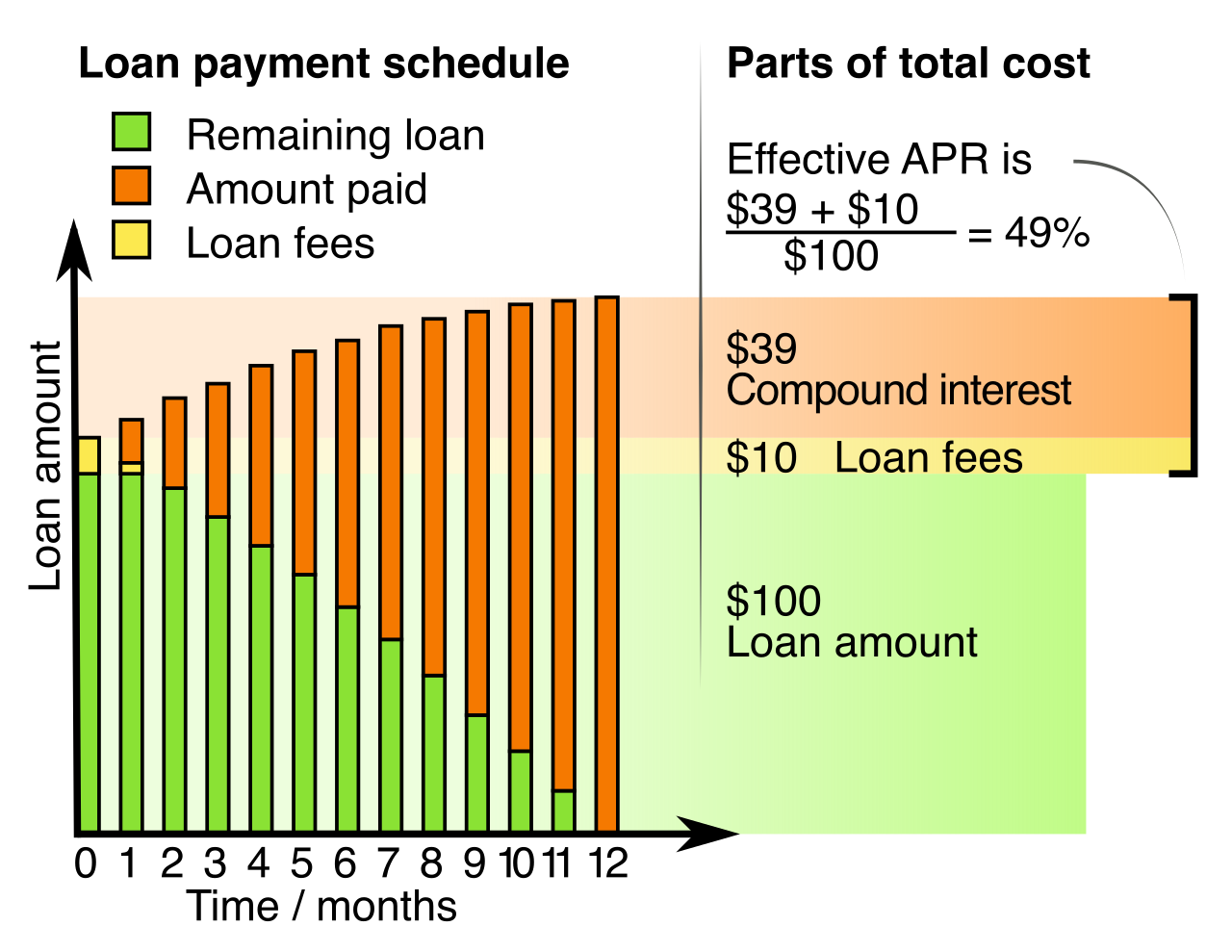

Truth in Lending (Regulation Z)

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Before 1968, the American credit market operated largely in the dark. A prospective homebuyer could sit across a desk from two different lenders, receive two entirely different sets of loan terms, and possess absolutely no mathematical way to compare them. One lender might quote a low interest rate but bury exorbitant fees in the fine print; another might offer a seemingly flat fee but structure the repayment to heavily penalize the borrower over time. The true cost of borrowing was obscured by a labyrinth of institutional jargon.

This asymmetry of information was fundamentally corrected when the Consumer Credit Protection Act was enacted in 1968. Designed to level the playing field, the Truth in Lending Act is Title I of the Consumer Credit Protection Act, functioning as the bedrock of modern real estate finance. The Truth in Lending Act promotes the informed use of consumer credit by forcing absolute transparency. It requires lenders to provide standardized disclosures about loan costs, ensuring that every consumer can evaluate the true weight of the debt they are assuming.

To translate this broad legislative mandate into enforceable, day-to-day operations, the Federal Reserve Board originally drafted the specific set of rules issued to implement the Truth in Lending Act, known universally in the real estate industry as Regulation Z. Today, the Consumer Financial Protection Bureau enforces the rules of Regulation Z.

As a real estate professional in New York, you are the crucial bridge between a buyer's aspirations and the strict realities of mortgage finance. Understanding Regulation Z is not merely about passing an exam; it is about guiding your clients safely through the most heavily regulated financial transaction of their lives.