Secondary Markets

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Imagine a local bank in Upstate New York that has just issued fifty mortgages to new homebuyers. The bank's vault is now effectively empty; the depositors' funds have been transformed into thirty-year promissory notes. If a fifty-first buyer walks through the door tomorrow, the bank cannot help them without fresh capital. This is the fundamental bottleneck of real estate finance: local lenders have a finite supply of deposits, yet the demand for home loans is continuous. The solution to this bottleneck is a vast, unseen financial ecosystem that operates relentlessly behind the scenes of every real estate transaction.

In real estate finance, the primary market is where loans are born—where you, as a real estate agent, see your clients sign the initial paperwork with their chosen lender. But what happens to the loan after the closing table?

The secondary mortgage market is a financial market where previously originated promissory notes and mortgages are bought and sold.

The primary purpose of the secondary mortgage market is to provide liquidity to primary mortgage market lenders. Secondary market participants replenish the capital available for new real estate loans by purchasing existing mortgages from primary lenders. Because the bank receives a lump sum of cash for the loan it just sold, a primary lender can originate more loans than the lender's deposit base would otherwise allow by selling originated loans into the secondary market.

On a macroeconomic scale, this mechanism does more than just keep a single bank operational. The secondary mortgage market stabilizes local real estate markets by smoothing out regional imbalances in mortgage funds. If New York experiences a massive surge in homebuying but lacks sufficient local bank deposits to fund the loans, while a state in the Midwest has an excess of banking deposits but fewer buyers, the secondary market bridges the gap, allowing capital to seamlessly flow where it is needed most.

How does the secondary market actually absorb trillions of dollars in residential mortgages? They use a process called securitization.

Once institutional buyers acquire these loans, secondary market participants pool purchased mortgages together to create investment products. Rather than holding individual promissory notes, secondary market participants sell shares of pooled mortgages to investors across the globe. These investment securities backed by pools of mortgages are known as mortgage-backed securities (MBS).

The Profit Motive for Local Lenders

If a local bank sells its loans almost immediately, how does it stay in business? The answer lies in the front-end and back-end fees.

First, primary lenders generate income from loan origination fees when selling loans on the secondary market. Second, the bank that originates the loan rarely steps out of the picture entirely. Primary lenders often retain the servicing rights to mortgage loans sold in the secondary market. Retaining servicing rights allows primary lenders to collect monthly payments on behalf of the secondary market investor in exchange for a servicing fee.

This is highly relevant to your clients. A buyer may close with a familiar local bank and continue writing their monthly check to that exact same bank, completely unaware that an international pension fund actually owns their debt via a mortgage-backed security.

Two monumental entities dominate the secondary market. They dictate the underwriting rules of modern real estate finance.

Fannie Mae (FNMA)

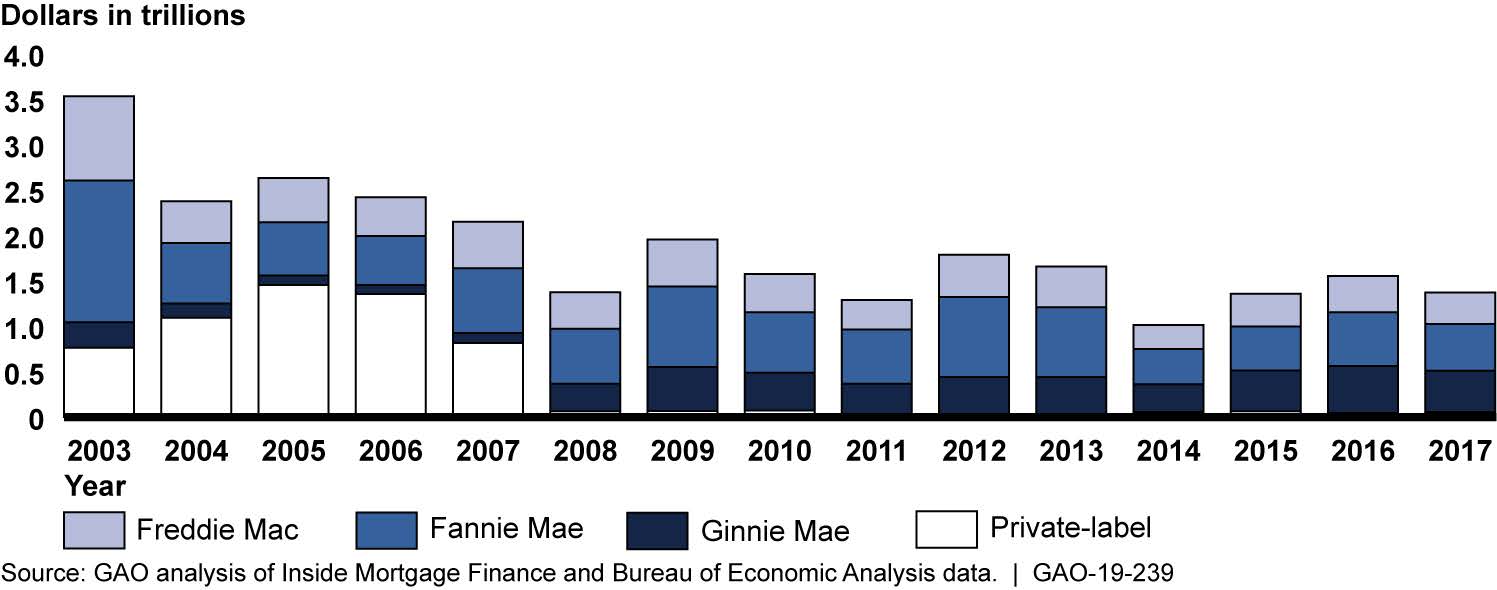

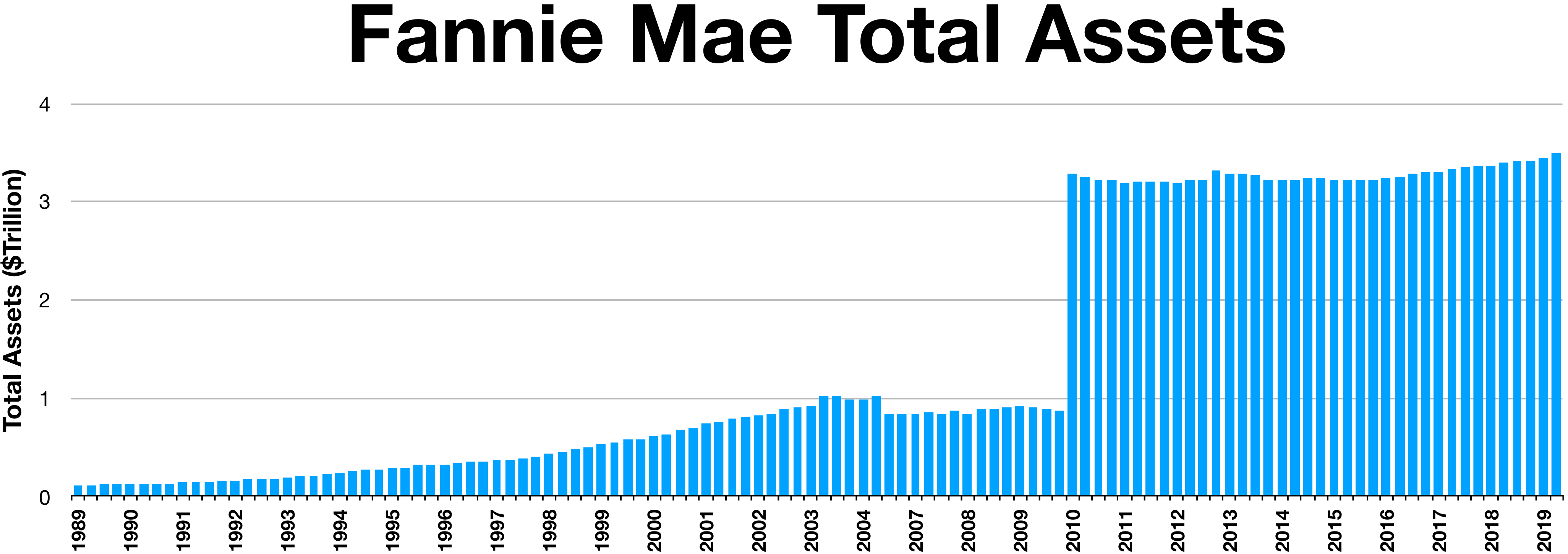

FNMA stands for the Federal National Mortgage Association, commonly referred to as Fannie Mae. Fannie Mae is a government-sponsored enterprise (GSE). Its mandate is to ensure capital continues flowing to homebuyers reliably. Fannie Mae purchases conventional, FHA-insured, and VA-guaranteed loans from primary lenders. Once purchased, Fannie Mae packages purchased mortgages into mortgage-backed securities, which are then traded on the open market.

Freddie Mac (FHLMC)

FHLMC stands for the Federal Home Loan Mortgage Corporation, commonly referred to as Freddie Mac. Like its sibling, Freddie Mac is a government-sponsored enterprise. However, Freddie Mac was originally created to provide a secondary mortgage market specifically for savings and loan associations. Today, its scope has broadened, and Freddie Mac primarily purchases conventional mortgage loans.

Conforming Limits and Jumbo Loans

To keep the mortgage-backed securities market standardized and predictable, these GSEs will not buy just any loan. A conforming loan is a mortgage loan that meets the purchasing criteria and guidelines established by Fannie Mae and Freddie Mac.

Crucially, Fannie Mae and Freddie Mac establish maximum loan limits for conforming loans. For example, in 2026, the baseline limit for a single-unit property in most areas is $832,750, while high-cost markets like New York City allow for limits up to $1,249,125.

Mortgage loans that exceed the maximum loan limits set by Fannie Mae and Freddie Mac are called jumbo loans. Because they break the size threshold, jumbo loans are classified as non-conforming loans.

This distinction dictates the closing reality for luxury properties. Primary lenders must sell non-conforming loans to private secondary market investors because government-sponsored enterprises will not purchase non-conforming loans. This is precisely why your clients seeking a $2 million mortgage for a Manhattan penthouse will face vastly different, often stricter underwriting requirements than a client buying a conforming home in Albany.

While Fannie and Freddie are GSEs, GNMA operates under an entirely different structure. GNMA stands for the Government National Mortgage Association, commonly referred to as Ginnie Mae.

Unlike the GSEs, Ginnie Mae is a wholly owned government corporation. Furthermore, Ginnie Mae operates within the United States Department of Housing and Urban Development (HUD).

Critical Distinction:

- Ginnie Mae does not buy or sell mortgage loans.

- Ginnie Mae does not issue mortgage-backed securities.

If it doesn't buy, sell, or issue, what is its purpose? Ginnie Mae guarantees the timely payment of principal and interest on specific mortgage-backed securities. It serves as an absolute backstop, essentially lending the full faith and credit of the U.S. government to investors to eliminate credit risk. Ginnie Mae exclusively guarantees mortgage-backed securities backed by federally insured or guaranteed loans, such as FHA and VA loans.

Finally, the broader secondary market accounts for the unique needs of America's agricultural sectors. The Federal Agricultural Mortgage Corporation is known as Farmer Mac. Much like Fannie and Freddie serve residential housing, Farmer Mac provides a secondary market specifically for agricultural real estate and rural housing mortgage loans.

| Entity | Full Name | Status | Primary Function & Characteristics |

|---|---|---|---|

| Fannie Mae | Federal National Mortgage Association (FNMA) | Government-Sponsored Enterprise | Purchases conventional, FHA, and VA loans; packages them into MBS. |

| Freddie Mac | Federal Home Loan Mortgage Corporation (FHLMC) | Government-Sponsored Enterprise | Originally for savings & loan associations; primarily purchases conventional loans. |

| Ginnie Mae | Government National Mortgage Association (GNMA) | Wholly Owned Gov't Corporation (HUD) | Does not buy/sell loans or issue MBS. Guarantees FHA/VA-backed MBS. |

| Farmer Mac | Federal Agricultural Mortgage Corporation | Government-Sponsored Enterprise | Provides a specialized secondary market for agricultural real estate and rural housing. |

Understanding these titans of finance allows you, as a New York real estate salesperson, to confidently guide your clients. When a buyer asks why mortgage rates have shifted, why a luxury loan requires a larger down payment, or why they are suddenly sending their payments to a different institution, you now know the answer: it is the relentless engine of the secondary mortgage market at work.