Appraisal Process and Regulations

To assign a definitive monetary value to real property is to freeze a highly dynamic system in time. A property is not inherently worth a fixed number of dollars; its value is constantly driven by macroeconomic currents, municipal zoning laws, human psychology, and physical decay. Therefore, an appraisal is not a simple observation or a wild guess. It is a professional, unbiased opinion of a property's market value based on established valuation methods. It represents a property's estimated market value as of one specific effective date—because the value of a property today might be drastically different tomorrow if a major employer leaves town or interest rates double overnight. Most importantly, an appraisal provides an estimate of a property's market value rather than a guarantee of the property's ultimate sale price. The ultimate sale price is decided by the market; the appraisal is the rigorous, scientific translation of market forces into a precise, defensible financial figure.

As an aspiring real estate salesperson, your daily reality will involve discussing property values with clients. However, there is a rigid, legally enforced firewall between the valuation tools you use as an agent and a formal appraisal.

When a homeowner asks you, "What should we list our house for?", you will prepare a Comparative Market Analysis (CMA). A CMA is an informal estimate of market value performed by a real estate licensee to help a client determine a listing price.

Similarly, banks and lenders will frequently ask real estate agents to provide a Broker Price Opinion (BPO). A BPO is a real estate licensee's estimate of property value frequently requested by lenders for short sales or foreclosures, usually because it is faster and less expensive than a full appraisal.

Crucial Legal Warning: A real estate licensee violates the law by referring to a Comparative Market Analysis or a Broker Price Opinion as a formal appraisal. Performing a real estate appraisal without a proper state appraiser license or certification constitutes unauthorized appraisal practice.

Knowing exactly where your expertise ends and the appraiser's begins protects your license and your clients.

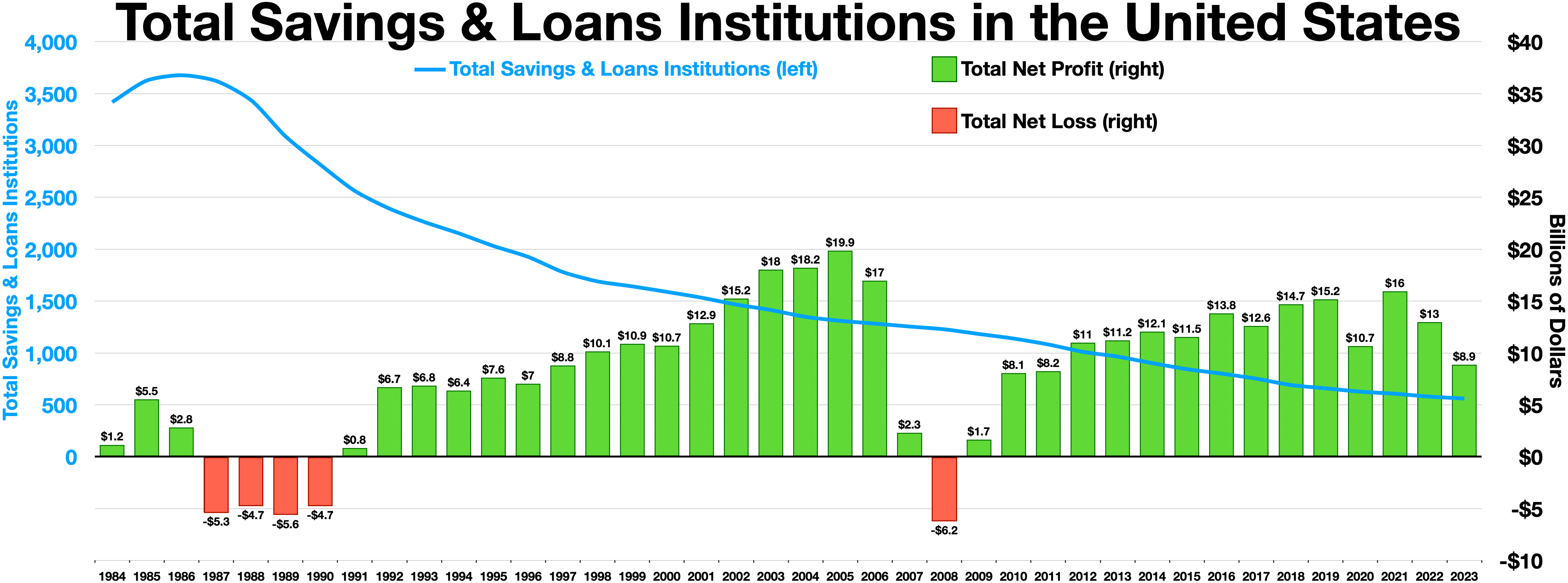

Why is the appraisal industry so strictly regulated? In the 1980s, wildly inflated and inaccurate appraisals contributed heavily to the Savings and Loan Crisis, costing taxpayers billions. In response, Congress stepped in to overhaul how real estate valuations were conducted.

The result was the Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA). This landmark legislation regulates the appraisal profession in the United States.

FIRREA requires a state-licensed or state-certified appraiser for all federally related real estate transactions. What does that mean in practice? A federally related transaction is any real estate-related financial transaction regulated by a federal financial institution regulatory agency. If a bank, credit union, or federal agency (like the FHA or VA) is involved in funding or backing the loan, federal rules apply.

However, Congress created practical exemptions to keep the real estate market moving for lower-priced properties. You do not strictly need a licensed or certified appraiser under federal law for:

- Residential federally related transactions valued at $400,000 or less.

- Commercial federally related transactions valued at $500,000 or less. (Note: Even below these thresholds, individual banks frequently require appraisals as part of their own risk-management policies).

Who Sets the Standards?

If FIRREA is the law, who writes the actual rulebook the appraisers must follow? The Appraisal Foundation is a national organization authorized by the United States Congress as the source of appraisal standards and appraiser qualifications.

The Appraisal Foundation authors the Uniform Standards of Professional Appraisal Practice (USPAP). These form the ethical and performance standards for the United States appraisal profession. State-licensed and state-certified appraisers must strictly adhere to the Uniform Standards of Professional Appraisal Practice when conducting real estate appraisals.

Appraiser Qualifications

Not all appraisers hold the same level of authority. The Appraisal Foundation establishes the baseline qualifications for two primary tiers you will encounter:

| Qualification Tier | Authority |

|---|---|

| State Licensed Real Estate Appraiser | Legally authorized to appraise non-complex residential properties up to a specific transaction value threshold. |

| State Certified General Real Estate Appraiser | Legally authorized to appraise all types of real property regardless of transaction value or complexity (including skyscrapers, industrial parks, and massive commercial centers). |

Appraisals are designed to be a shield against bias. For an appraisal to have any value to a lender, the appraiser must be entirely neutral. This neutrality dictates how appraisers are paid and who they actually work for.

The Payment Rule

If an appraiser were paid a percentage of the final value they concluded, they would have a massive financial incentive to inflate the property's worth. Therefore, an appraiser commits a severe ethical violation by basing an appraisal fee on a percentage of the property's final appraised value. Instead, an appraiser's fee is strictly based on the estimated time and effort required to complete the appraisal assignment.

Who Owns the Report?

One of the most common misunderstandings in residential real estate involves who "owns" the appraisal. Imagine your buyer client, Sarah. She pays a $600 invoice for the appraisal as part of her loan origination fees. When the report is finished, she demands that the appraiser send her a copy directly. The appraiser refuses. Why?

In the appraisal profession, the client in an appraisal assignment is exclusively the specific party who directly engages the appraiser's services. In a standard residential mortgage transaction, the lending institution acts as the appraiser's official client, not the homebuyer.

Because of USPAP confidentiality rules, an appraiser is legally obligated to share the final appraisal report only with the client or parties explicitly authorized by the client. Therefore, a homebuyer who pays for an appraisal during a mortgage transaction does not automatically own the appraisal report. (Federal lending laws dictate that the lender must provide a copy to the borrower, but the appraiser themselves answers only to the bank).

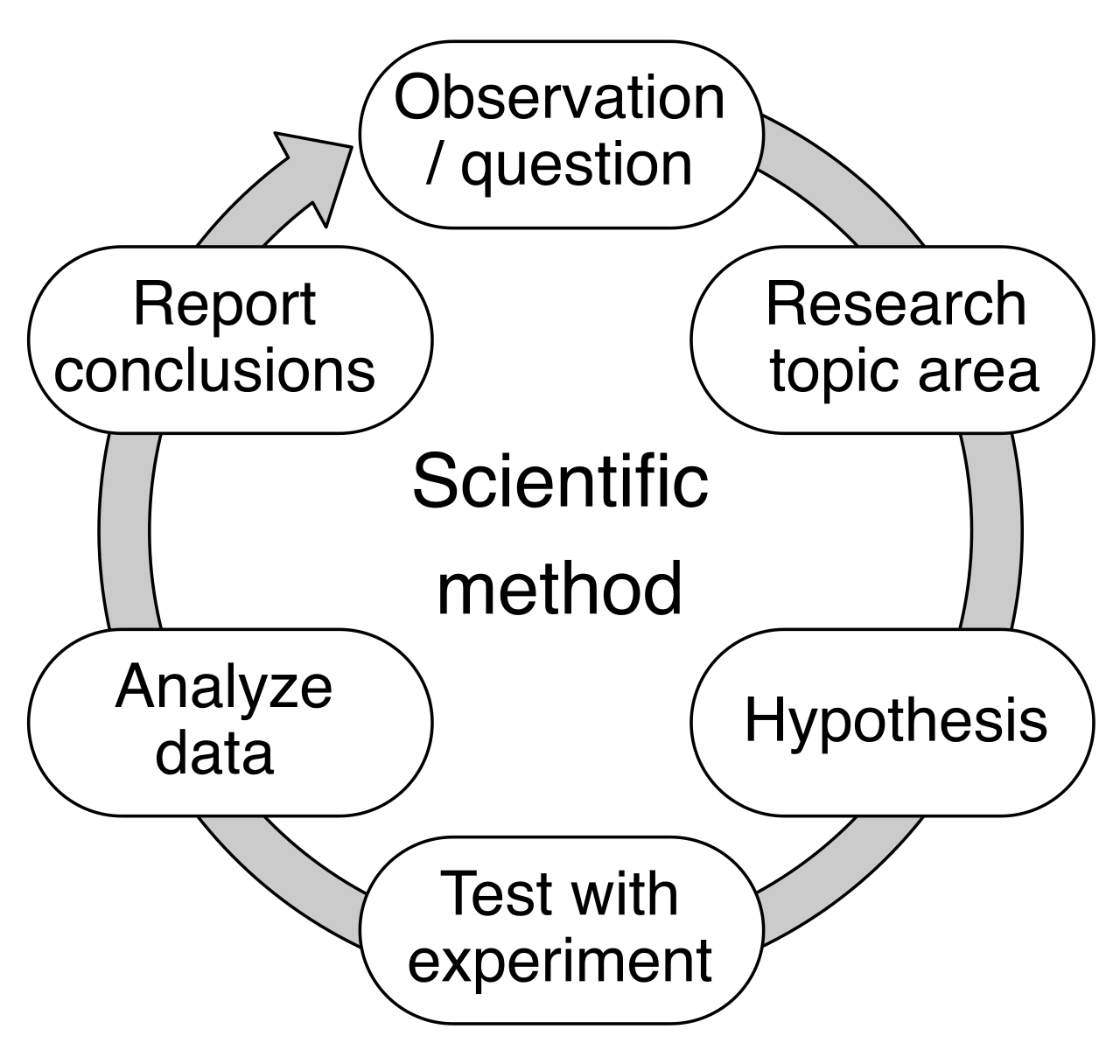

To guarantee that value estimates are credible and unbiased, appraisers do not simply walk through a house, tap the walls, and guess. They execute a highly structured, eight-step scientific method.

Step 1: Stating the Problem

You cannot solve a problem until you define it. The first step in the formal appraisal process involves stating the specific problem to be solved. This is highly specific and requires four exact parameters:

- Identifying the exact subject property being evaluated.

- Identifying the specific property rights to be valued (Are we valuing fee simple absolute ownership, or just a leasehold interest?).

- Defining the specific type of value being sought by the client (Usually Market Value, but could be Insurance Value or Liquidation Value).

- Specifying the effective date of the appraisal.

Step 2: Determining the Scope of Work

Once the problem is stated, the second step in the formal appraisal process is determining the scope of work. The scope of work outlines the extent of the research and analyses the appraiser will perform to reach a credible value conclusion. An appraisal of a cookie-cutter suburban home requires a very different scope of work than an appraisal of a historic, 150-year-old downtown hotel.

Step 3: Gathering, Recording, and Verifying Data

The appraiser acts as a researcher, pulling data from the macro level down to the micro level.

- First, they must gather, record, and verify general data about the region, city, and neighborhood (e.g., economic trends, zoning laws, demographic shifts).

- Next, they must gather, record, and verify specific data regarding the subject property itself (e.g., square footage, condition, age, property defects).

Step 4: Determining Highest and Best Use

This is perhaps the most intellectually fascinating step. The fourth step in the formal appraisal process is determining the highest and best use of the subject property.

The highest and best use analysis evaluates the most profitable, legally permissible, and physically possible use of a specific parcel of real estate. Imagine a rundown single-family home sitting on a large lot right next to a newly built subway station, and the city has just rezoned the land for commercial high-rises. The "highest and best use" of that property is no longer a single-family home; it is high-density commercial. The appraiser must value the property based on what it should be to maximize profit, provided it is legal and physically possible.

Step 5: Estimating Land Value

Because land does not depreciate—but buildings do—the two must be separated. The fifth step in the formal appraisal process is estimating the value of the land separate from any physical structures on the property. Land value in an appraisal is typically estimated using the sales comparison approach (comparing the subject land to recently sold vacant lots in the area).

Step 6: The Three Approaches to Valuation

The sixth step in the formal appraisal process is estimating the total property value using three distinct valuation approaches. Depending on the property type, the appraiser will lean on one or more of these methods:

- The Sales Comparison Approach: Valuing the property by comparing it to recently sold, similar properties. (Most common for residential real estate).

- The Cost Approach: Valuing the property based on how much it would cost to build an exact replica today, minus accumulated depreciation, plus the land value. (Crucial for unique properties like schools, churches, or hospitals where there are no recent sales to compare).

- The Income Approach: Valuing the property based on the present value of the future income it will generate. (Used for commercial properties, apartment buildings, and retail centers).

Step 7: Reconciliation

Once the appraiser has calculated values using the three approaches, they will inevitably have three different numbers. The seventh step in the formal appraisal process is reconciling the estimated values from the three different valuation approaches. Appraisal reconciliation is the analytical process of weighing the findings from different valuation approaches to arrive at a single final estimate of value.

The Golden Rule of Reconciliation: An appraiser must never simply calculate a mathematical average of the values from the three valuation approaches during the reconciliation step.

Averaging is mathematically lazy and logically flawed. If an appraiser is valuing an elementary school, the Cost Approach yields highly reliable data, while the Sales Comparison Approach yields terrible data (because schools rarely sell). The appraiser uses their professional judgment to give the most weight to the most relevant approach, rather than averaging good data with bad data.

Step 8: Delivering the Report

The final step in the formal appraisal process is preparing and delivering the written appraisal report to the client. This report is a comprehensive document that defends the appraiser's methodology, presents the verified data, and conclusively states the final opinion of market value as of the effective date.

By mastering the boundaries of your role and understanding the rigorous, eight-step scientific method appraisers use, you will be deeply equipped to guide your future clients through the anxieties of the valuation process, keeping their transactions smooth, legal, and moving toward the closing table.