Microeconomics Fundamentals

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Every aspiring educator faces an immediate, mathematical constraint: there are exactly twenty-four hours in a day, and the demands on a teacher’s time are virtually infinite. Lesson planning, grading, professional development, and student outreach all compete for the same limited resource. This fundamental conflict between infinite desires and finite resources is not merely a scheduling problem; it is the universal mechanism from which the entire discipline of microeconomics emerges. To understand history, government, and human behavior—the core of the social studies curriculum—one must first understand how societies navigate the inescapable reality of limits.

The engine of all economic thinking is scarcity. Scarcity occurs because human wants exceed the limited resources available. It is not a temporary shortage or a localized phenomenon; it is a permanent condition of human existence. Because we cannot have everything we want, scarcity forces individuals and societies to make choices about resource allocation.

Every choice requires a sacrifice. In economics, we separate the totality of what you give up from the specific value of the best alternative. A trade-off involves all the possible alternatives given up when a decision is made. If a school district decides to spend its budget on upgrading athletic facilities, the trade-offs include new history textbooks, updated science labs, and hiring more counselors—everything they could have bought instead.

However, we need a precise way to measure the true cost of that decision.

Opportunity cost is the value of the next best alternative given up when making a choice.

It is not the sum of all trade-offs; it is the specific value of the one thing you would have chosen had you not made your current choice. If the school board’s second choice was the history textbooks, the opportunity cost of the new athletic facility is the value of those unpurchased textbooks.

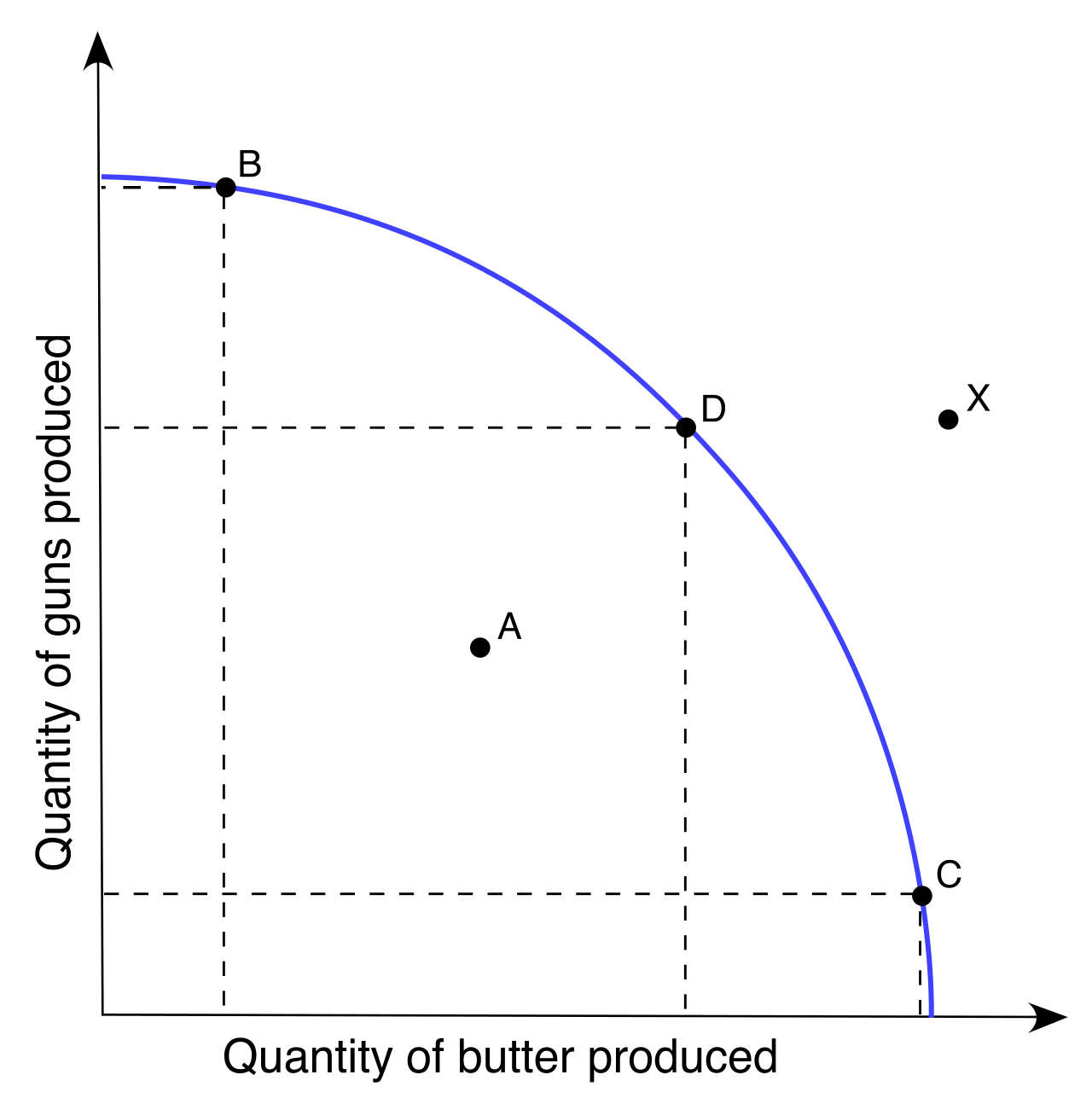

To teach this concept clearly, economists use a model called the Production Possibilities Curve (PPC). The Production Possibilities Curve illustrates the maximum possible output combinations of two goods.

Imagine a nation transitioning to a wartime footing—a frequent scenario in your U.S. and World History curricula. The society must choose between producing civilian goods (tractors) and military goods (tanks).

- Points on the Production Possibilities Curve represent the efficient use of resources. If the economy is on the curve, it is running at maximum capacity.

- Points inside the Production Possibilities Curve represent the inefficient use of resources. During the Great Depression, for example, factories sat empty and millions were unemployed; the U.S. economy was operating deep inside its PPC.

- Points outside the Production Possibilities Curve are unattainable with current resources and technology. The nation simply does not have the steel or labor to produce that much.

Why does the PPC typically bow outward rather than form a straight line? This brings us to the law of increasing opportunity cost, which states that producing more of one good requires giving up increasing amounts of another good. Resources are not perfectly adaptable. If you shift auto-workers and tractor factories to build tanks, the first conversions are easy and cheap. But as you demand more and more tanks, you must start converting resources that are terrible at making tanks—like agricultural land and bakers. The cost of each additional tank, measured in lost tractors, gets steeper and steeper.

To produce anything—whether it is a tank, a tractor, or an education—a society must utilize resources. The factors of production are the resources used to produce goods and services. The four primary factors of production are land, labor, capital, and entrepreneurship.

Each factor generates a specific economic return (income) for its owner:

| Factor of Production | Definition | Economic Return |

|---|---|---|

| Land | In economics, land refers to all natural resources used in production (e.g., forests, minerals, water). | Rent is the economic return generated by the land factor of production. |

| Labor | Labor refers to the human effort directed toward producing goods and services (e.g., teachers, factory workers). | Wages are the economic return generated by the labor factor of production. |

| Capital | Capital refers to human-made goods used to produce other goods and services (e.g., factory machines, smartboards, hammers). | Interest is the economic return generated by the capital factor of production. |

| Entrepreneurship | Entrepreneurship involves the risk-taking and organization required to combine land, labor, and capital for production. | Profit is the economic return generated by the entrepreneurship factor of production. |

A vital clarification for your Praxis exam: Do not confuse physical capital with money. Financial capital is money used to buy the tools and equipment used in economic production. Money itself does not produce anything; it is the medium used to acquire the actual physical capital (the hammers and tractors) that does the producing.

Because resources are scarce, every society must answer three fundamental questions: An economic system determines what to produce, how to produce, and for whom to produce. History is largely the study of how different societies have structured these systems.

- A traditional economy relies on customs, rituals, and historical precedents to make economic decisions. Roles are typically passed down through generations, ensuring stability but severely limiting innovation and growth.

- A command economy features a central government authority making the major decisions regarding production and distribution. Think of the Soviet Union’s Five-Year Plans. The government owns the factors of production and decides what gets made and who gets it.

- A market economy relies on the voluntary exchange of buyers and sellers to allocate resources. To function, this system requires a specific legal framework: private property rights are a foundational requirement for a functioning market economy. Without the guarantee that you own your labor, capital, and the fruits of your entrepreneurship, the incentive to produce vanishes.

- A mixed economy combines elements of both market and command economic systems. No purely market or purely command economy exists in the modern world. The United States operates primarily as a mixed economy; while largely driven by free markets, the government regulates industries, provides public education, and commands resources for national defense.

In a market-leaning economy, the questions of what, how, and for whom are answered by the decentralized machinery of supply and demand. This is how millions of strangers coordinate their behavior without a central planner.

Understanding Demand

Demand represents the consumer's side of the market.

- The law of demand states that quantity demanded has an inverse relationship with the price of a good. As price rises, consumers buy less; as price falls, they buy more.

- Because of this inverse relationship, a standard demand curve graphically slopes downward from left to right.

Here is the most critical conceptual trap on any economics exam: distinguishing between a movement and a shift.

- A change in the price of a good causes a movement along the demand curve. If the price of coffee drops from $4 to $2, you slide down the existing curve. A movement along the demand curve is strictly defined as a change in quantity demanded.

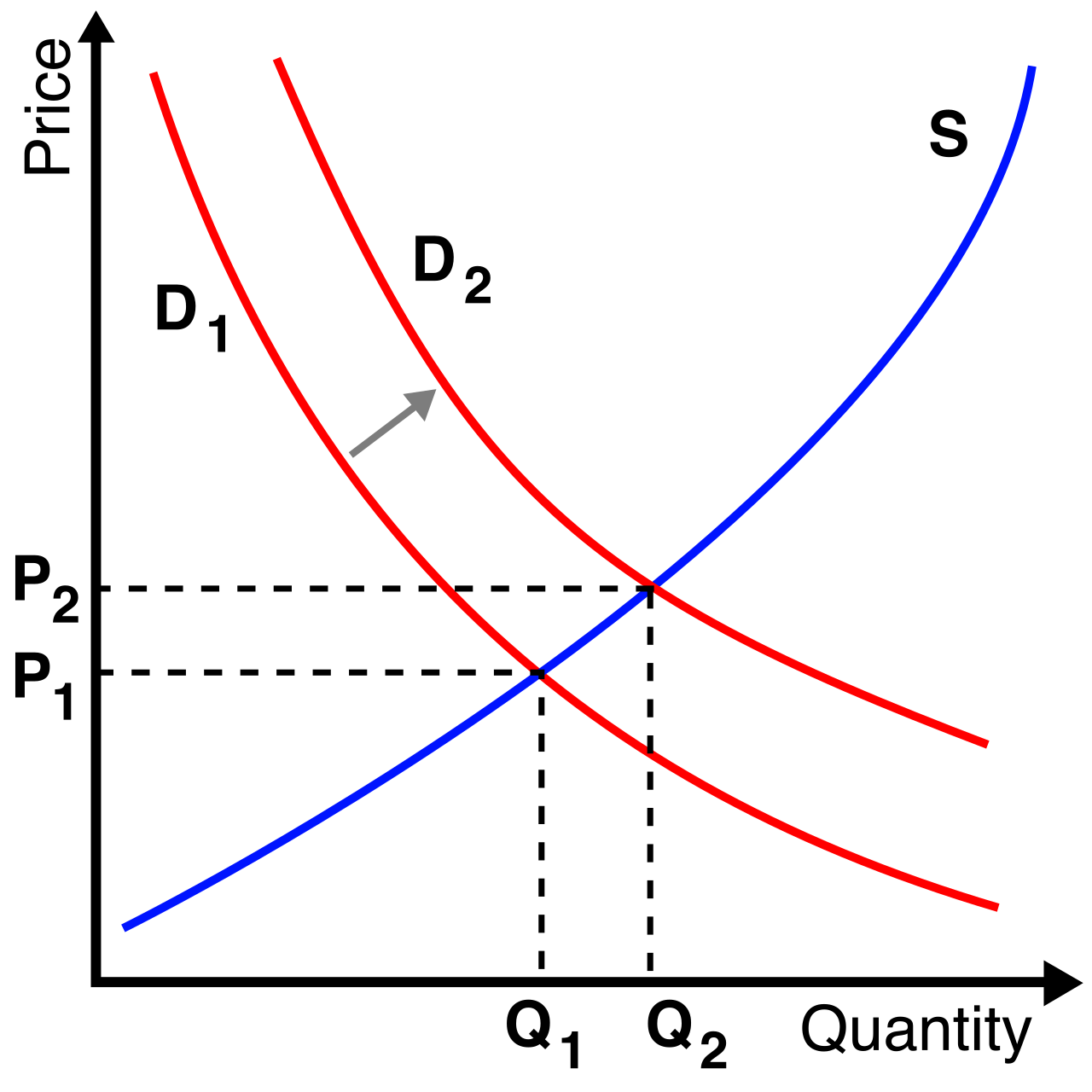

- Non-price determinants cause a shift of the entire demand curve. This means that at every single price, consumers now want a different amount. A shift of the entire demand curve is defined as a change in demand.

What causes these shifts? Several non-price determinants:

- Income: For most goods, an increase in consumer income increases the demand for normal goods (like fresh steaks or new cars). Conversely, an increase in consumer income decreases the demand for inferior goods (like instant ramen or used clothing), because consumers can now afford better alternatives.

- Substitute Goods: Substitute goods are products that can be used in place of one another (e.g., butter and margarine). An increase in the price of a substitute good increases the demand for the related substitute alternative. If butter gets expensive, the whole demand curve for margarine shifts outward.

- Complementary Goods: Complementary goods are products that are typically consumed together (e.g., hot dogs and hot dog buns). An increase in the price of a complementary good decreases the demand for the related partner good. If hot dogs become prohibitively expensive, people buy fewer buns.

Understanding Supply

Supply represents the producer's side of the market.

- The law of supply states that quantity supplied has a direct relationship with the price of a good. As the price a producer can fetch increases, they are incentivized to produce more.

- Because of this direct relationship, a standard supply curve graphically slopes upward from left to right.

The same strict language rules apply to producers:

- A change in the price of a good causes a movement along the supply curve. This movement is defined as a change in quantity supplied.

- Non-price determinants cause a shift of the entire supply curve. This shift is defined as a change in supply.

What shifts the entire supply curve?

- Technology: Improvements in production technology increase the supply of a good (shifting the curve to the right). If a new assembly line makes building cars twice as fast, manufacturers will supply more cars at every price point.

- Input Costs: An increase in the cost of production inputs (labor wages, land rent, capital interest) decreases the supply of a good (shifting the curve to the left). If the price of steel skyrockets, producing cars becomes more expensive, and the overall supply shrinks.

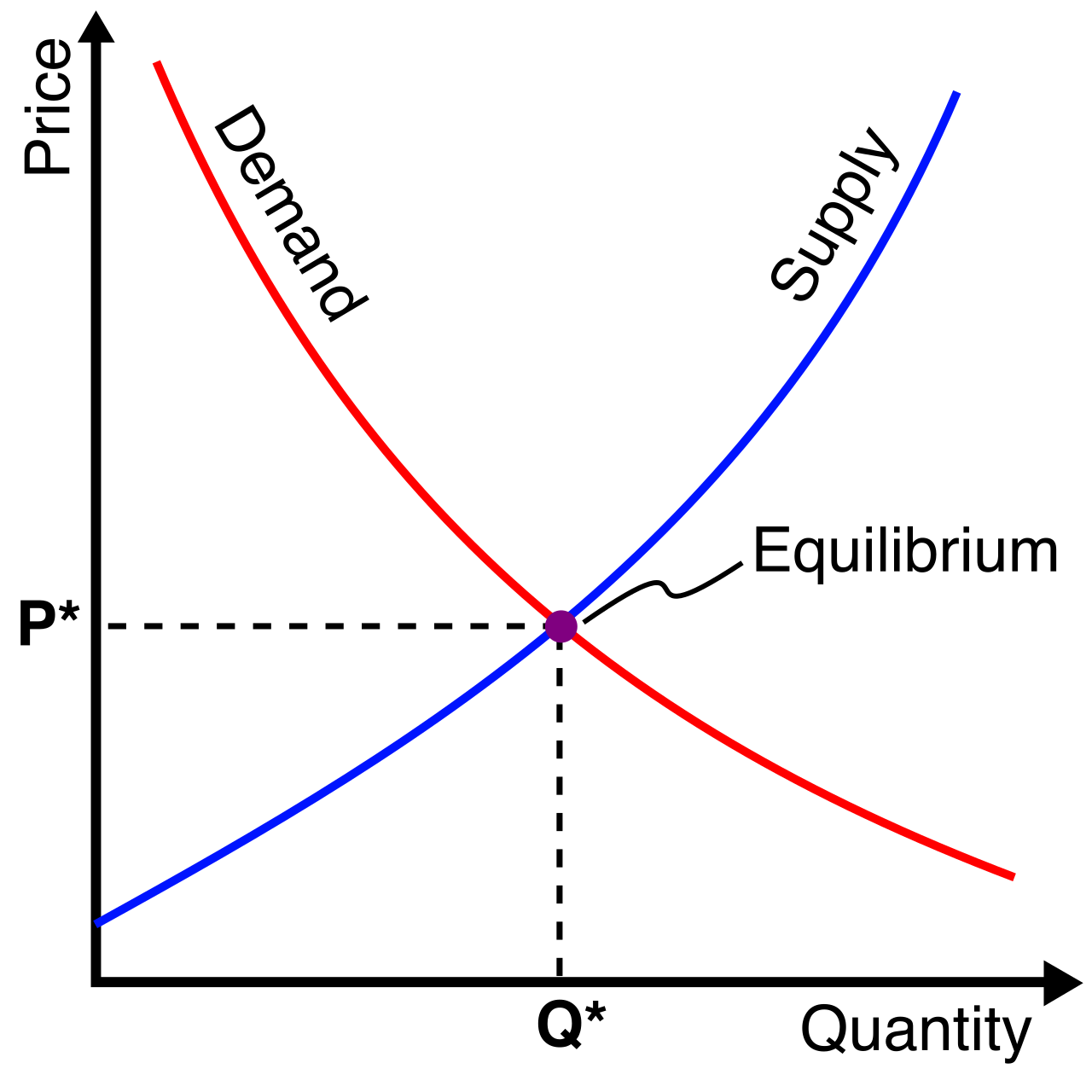

When you overlay the downward-sloping demand curve and the upward-sloping supply curve on the same graph, they intersect. This intersection is the heartbeat of a market economy.

Market equilibrium occurs at the exact price where quantity demanded equals quantity supplied.

At this precise point, every consumer willing to pay the price gets the good, and every producer willing to sell at that price sells the good. Because there are no leftover goods and no unfulfilled buyers, the equilibrium price is commonly referred to as the market-clearing price.

But what happens when the market is out of balance?

- A surplus occurs when the quantity supplied exceeds the quantity demanded at a given price. This happens when the price is temporarily too high. Producers make too much, consumers buy too little, and goods sit on the shelves. To clear the inventory, producers must lower the price.

- A shortage occurs when the quantity demanded exceeds the quantity supplied at a given price. This happens when the price is temporarily too low. Consumers swarm to buy the good, emptying shelves before everyone gets one. This signals producers to raise the price.

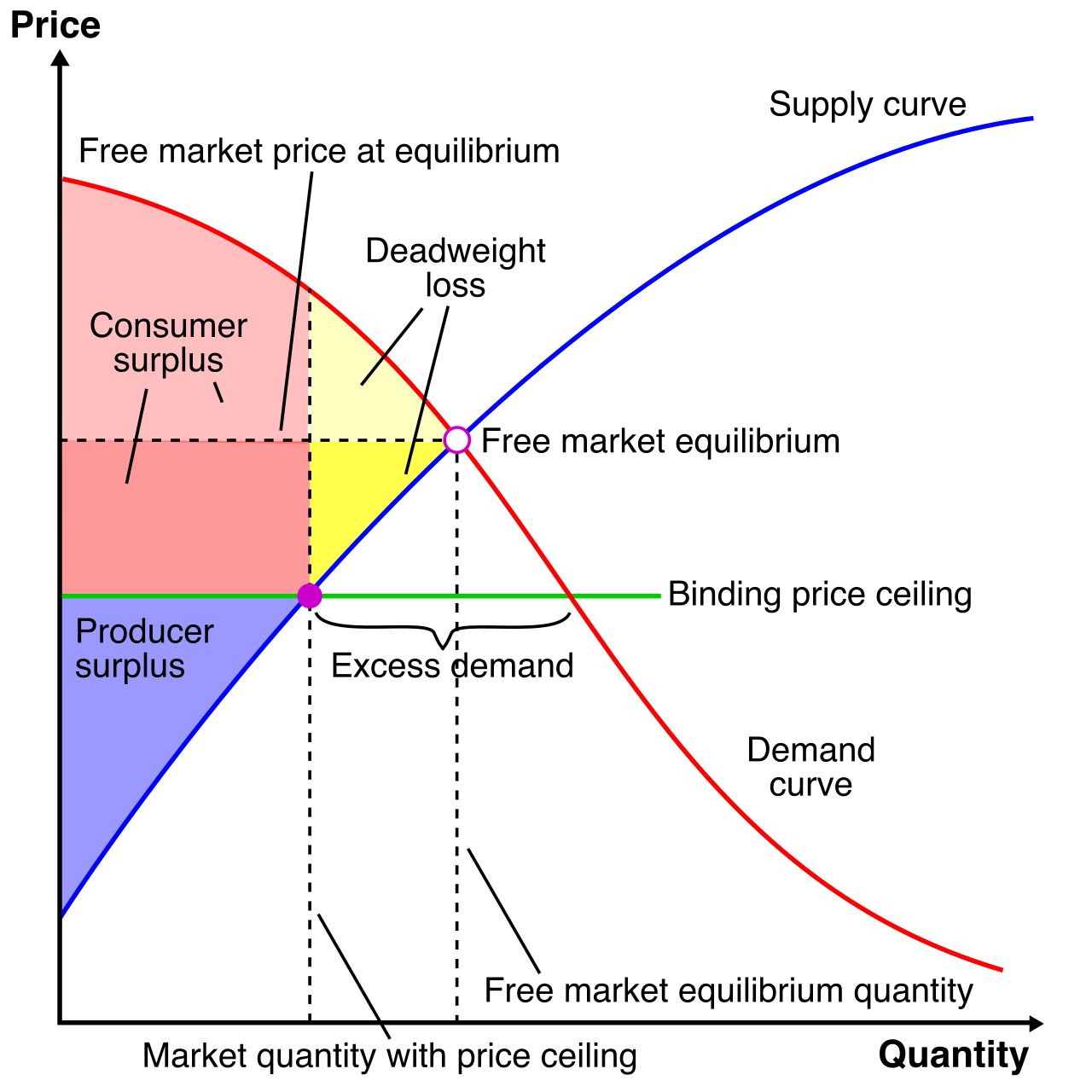

Sometimes, a government decides that the market-clearing price is unfair to buyers (too high) or unfair to sellers (too low). In a mixed economy, the government may intervene using price controls. Because these controls legally prevent the market from reaching equilibrium, they invariably create disequilibrium.

Price Ceilings

A price ceiling is a government-imposed legal maximum price that can be charged for a good (e.g., rent control laws designed to keep housing affordable).

For a price ceiling to actually impact the market, it must be "binding." A binding price ceiling set below the equilibrium price forces the price to stay artificially low. Because the price is low, consumers demand more apartments than producers are willing to supply. Therefore, a binding price ceiling set below the equilibrium price creates a market shortage.

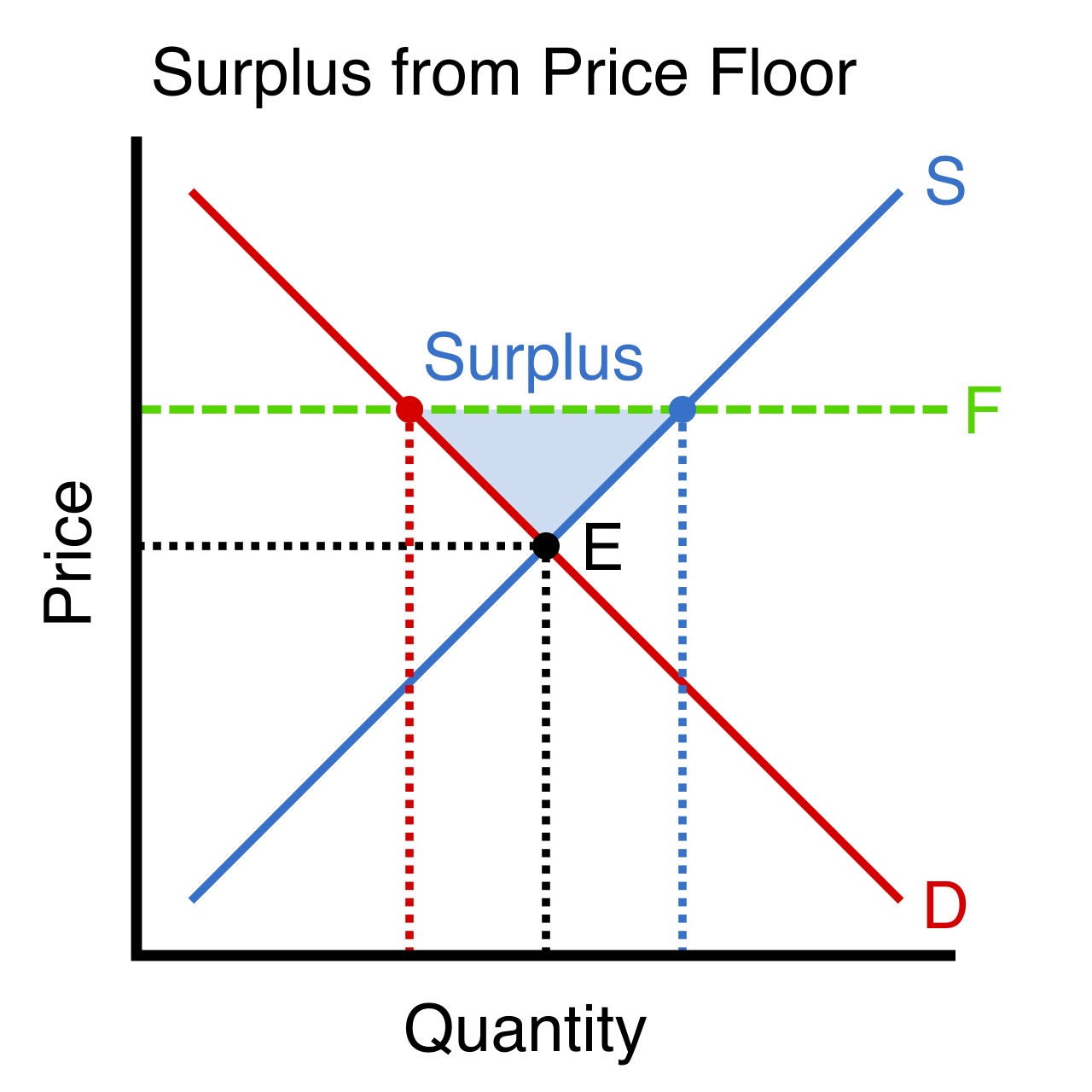

Price Floors

A price floor is a government-imposed legal minimum price that can be charged for a good (e.g., minimum wage laws or agricultural price supports).

To impact the market, a price floor must be binding by being set above the equilibrium price. This forces the price to remain artificially high. At this high price, producers are eager to supply vast amounts of the good, but consumers demand very little. Therefore, a binding price floor set above the equilibrium price creates a market surplus.

By mastering these mechanics—from the inescapable reality of scarcity to the intricate dance of supply, demand, and government policy—you are not just memorizing vocabulary for a test. You are learning the fundamental grammar of human decision-making, an essential toolkit for any teacher preparing to explain the complex history and civic structures of our world.