Market Efficiency and Firm Behavior

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Every human society, from ancient agrarian civilizations to hyper-connected modern democracies, faces the identical fundamental problem: how to allocate scarce resources. The market system operates as a decentralized computational engine designed to solve this problem. When buyers and sellers interact, they communicate through the language of prices, constantly negotiating the most efficient use of land, labor, and capital. To understand history, politics, and human geography, one must understand the invisible mathematical architecture governing these choices. As a social studies educator, you will trace the effects of economic policy—from the bread riots of the French Revolution to the geopolitics of modern oil—meaning you must possess a rigorous, intuitive grasp of how markets clear, why they fail, and how firms behave under different structural conditions.

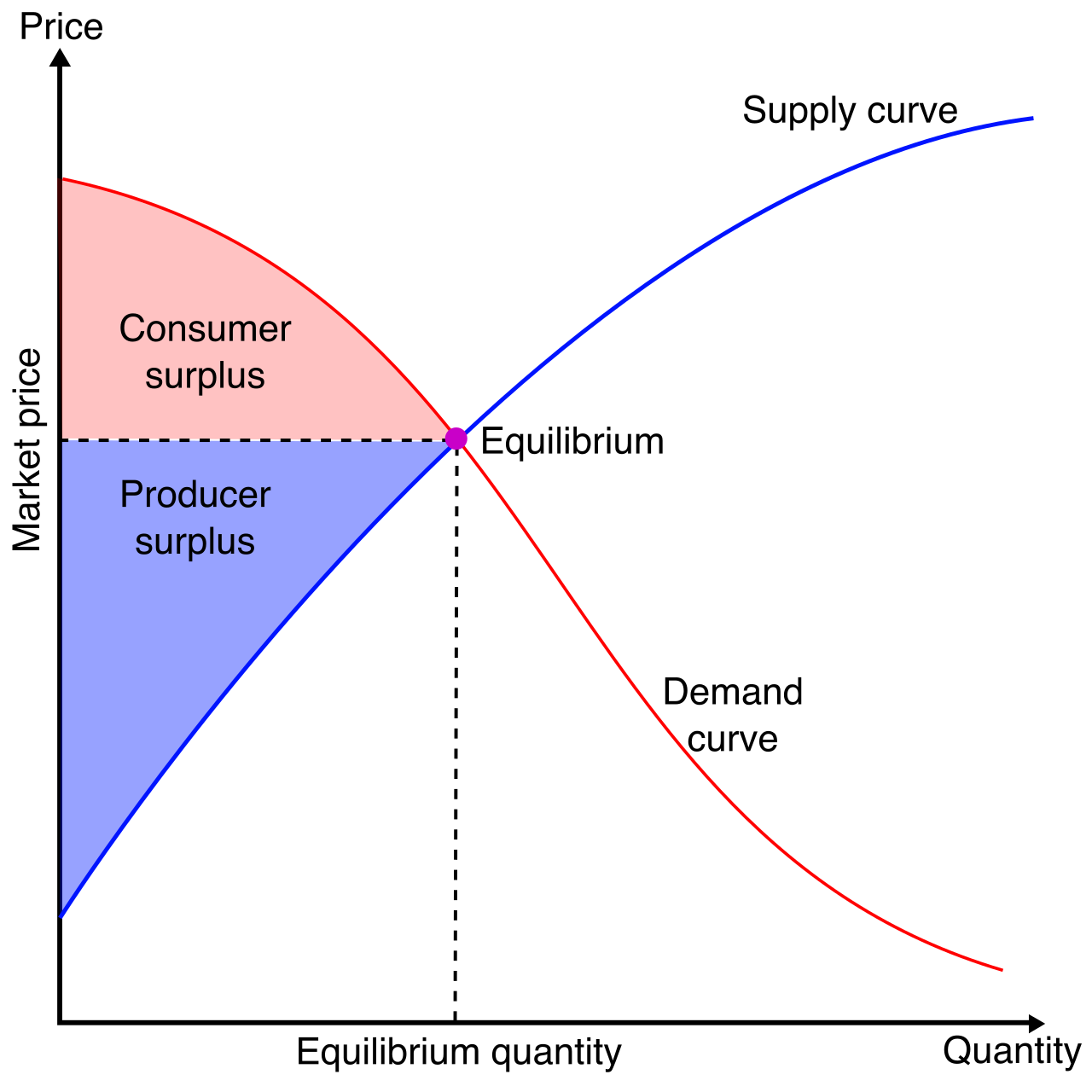

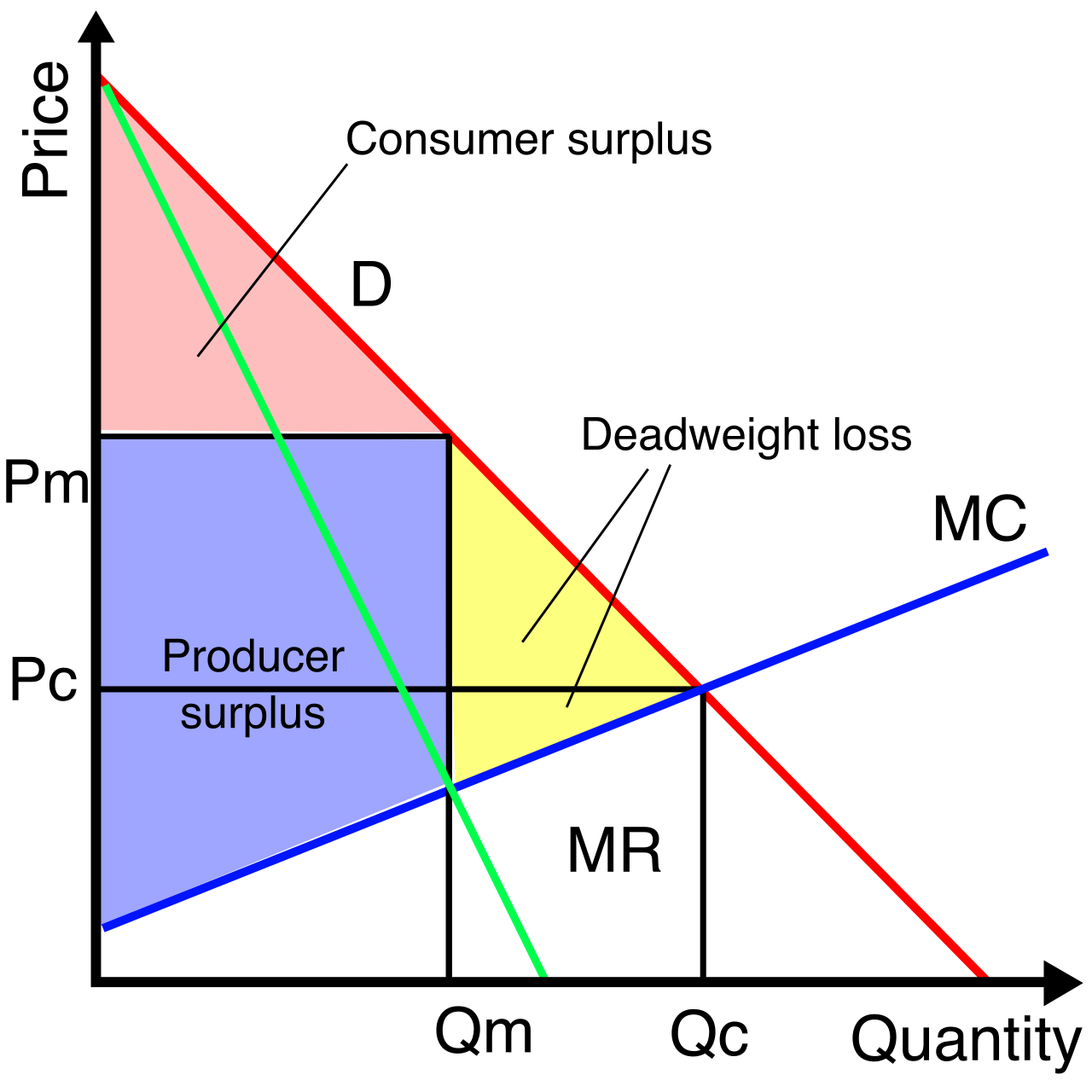

Imagine a student in your classroom who desperately wants a specific historical atlas. She is willing to pay $40 for it. You have an extra copy that you are willing to sell for a minimum of $15. If you agree on a price of $25, something magical happens: you both walk away wealthier in terms of utility.

This transaction illustrates the core of market mechanics. Consumer surplus is the difference between the maximum price a consumer is willing to pay and the actual price paid (in this case, $40 - $25 = $15). Producer surplus is the difference between the actual price received and the minimum price a seller is willing to accept ($25 - $15 = $10).

Total Economic Surplus = Consumer Surplus + Producer Surplus

In our atlas example, the total economic surplus is $25. Market efficiency occurs when total economic surplus is maximized. When a free, perfectly competitive market reaches equilibrium, it allocates resources to the buyers who value them most highly and the sellers who can produce them most cheaply.

However, external forces often prevent the market from reaching this optimal point. When a market is distorted, we experience a deadweight loss, which is the reduction in total surplus resulting from a market distortion. It is economic value that simply evaporates into thin air—trades that should have happened but didn't.

Governments rarely leave markets completely alone. They intervene to raise revenue, support vital industries, or protect vulnerable citizens. For a social studies teacher, these interventions are the building blocks of civics and political history.

Taxation and the Price Wedge

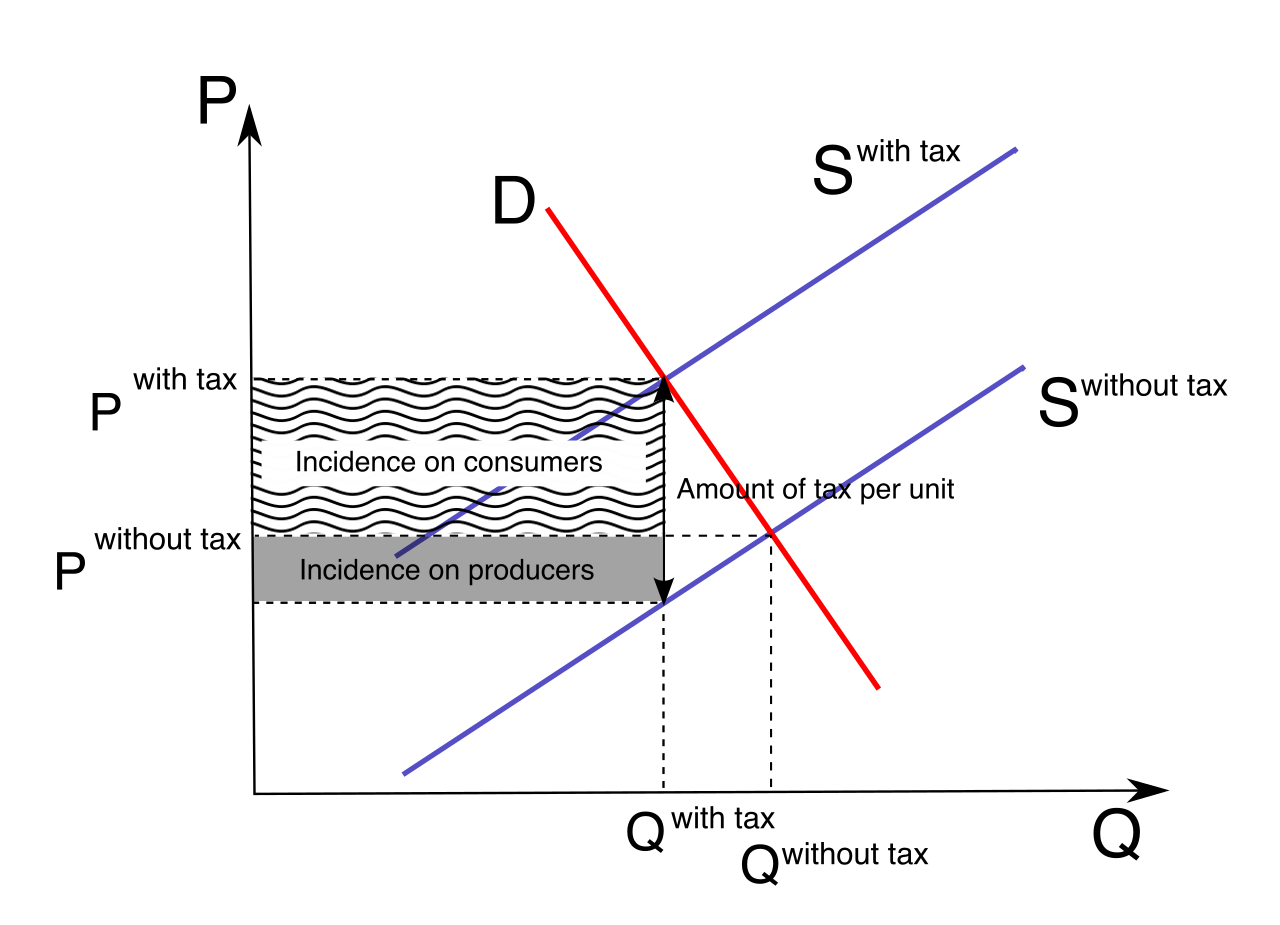

When a government levies a tax on a good, it creates a wedge between the price buyers pay and the price sellers receive. Imagine a $5 tax on every textbook. Buyers now pay more, sellers net less, and as a result, a tax placed on a market decreases the equilibrium quantity traded. Because fewer textbooks are sold than in a free market, taxes inherently create deadweight loss.

Who actually pays the tax? This depends on elasticity—how sensitive buyers and sellers are to price changes.

The Burden of Taxation: The burden of a tax falls more heavily on the side of the market that is more price inelastic.

If consumers are addicted to coffee (inelastic demand) and coffee roasters can easily switch to roasting cocoa (elastic supply), a tax on coffee will be paid almost entirely by the consumers in the form of higher prices.

Subsidies: The Artificial Boost

A government subsidy is a reverse tax. By providing financial assistance to producers, a subsidy shifts the supply curve to the right. This creates two immediate, visible effects:

- It lowers the equilibrium price paid by consumers.

- It increases the effective price received by producers.

While this sounds like a win-win, subsidies create deadweight loss. Why? Because they artificially prop up production, encouraging the production of units where the cost of production exceeds the value to consumers. Society is spending $10 worth of resources to grow soybeans that consumers only value at $8.

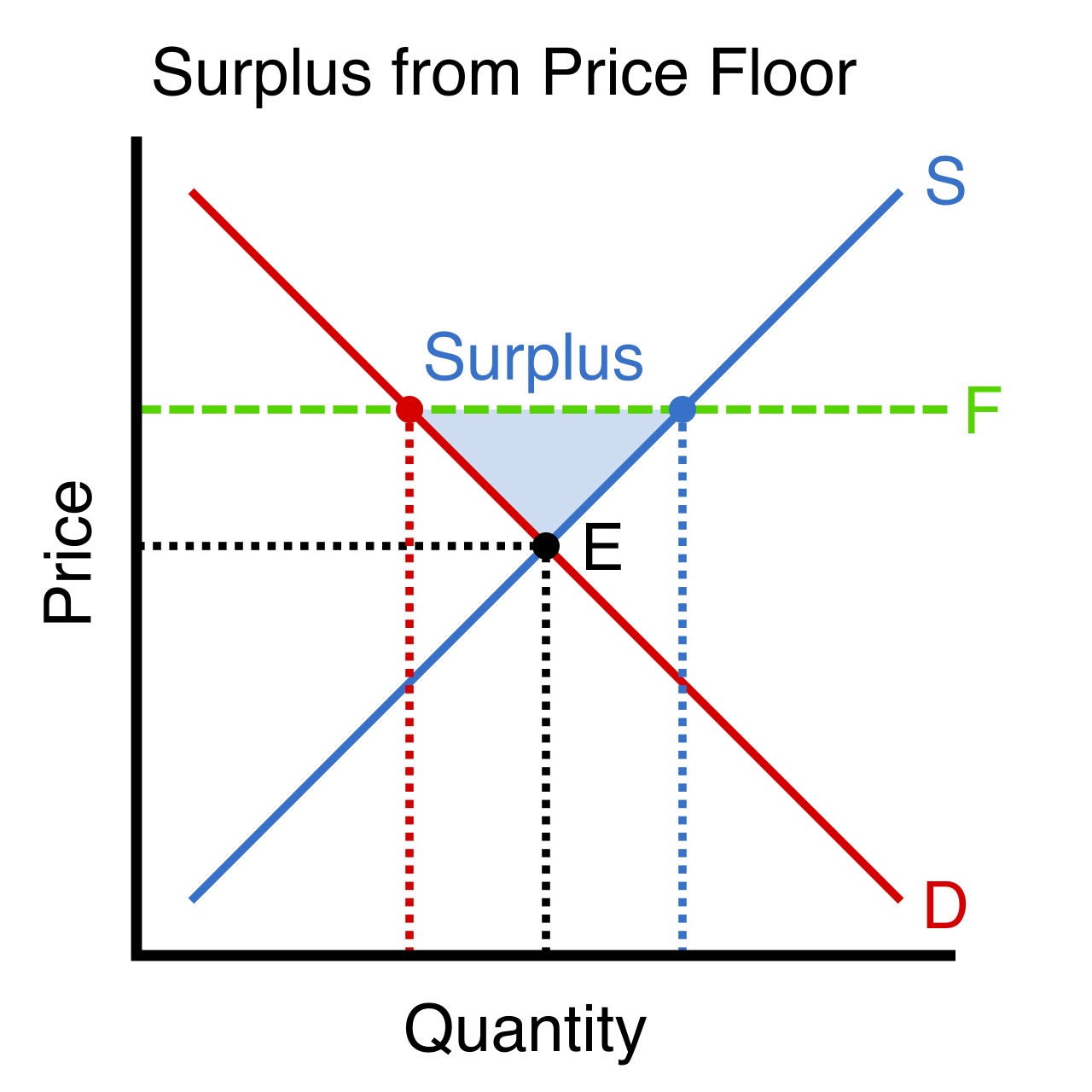

Price Controls: Ceilings and Floors

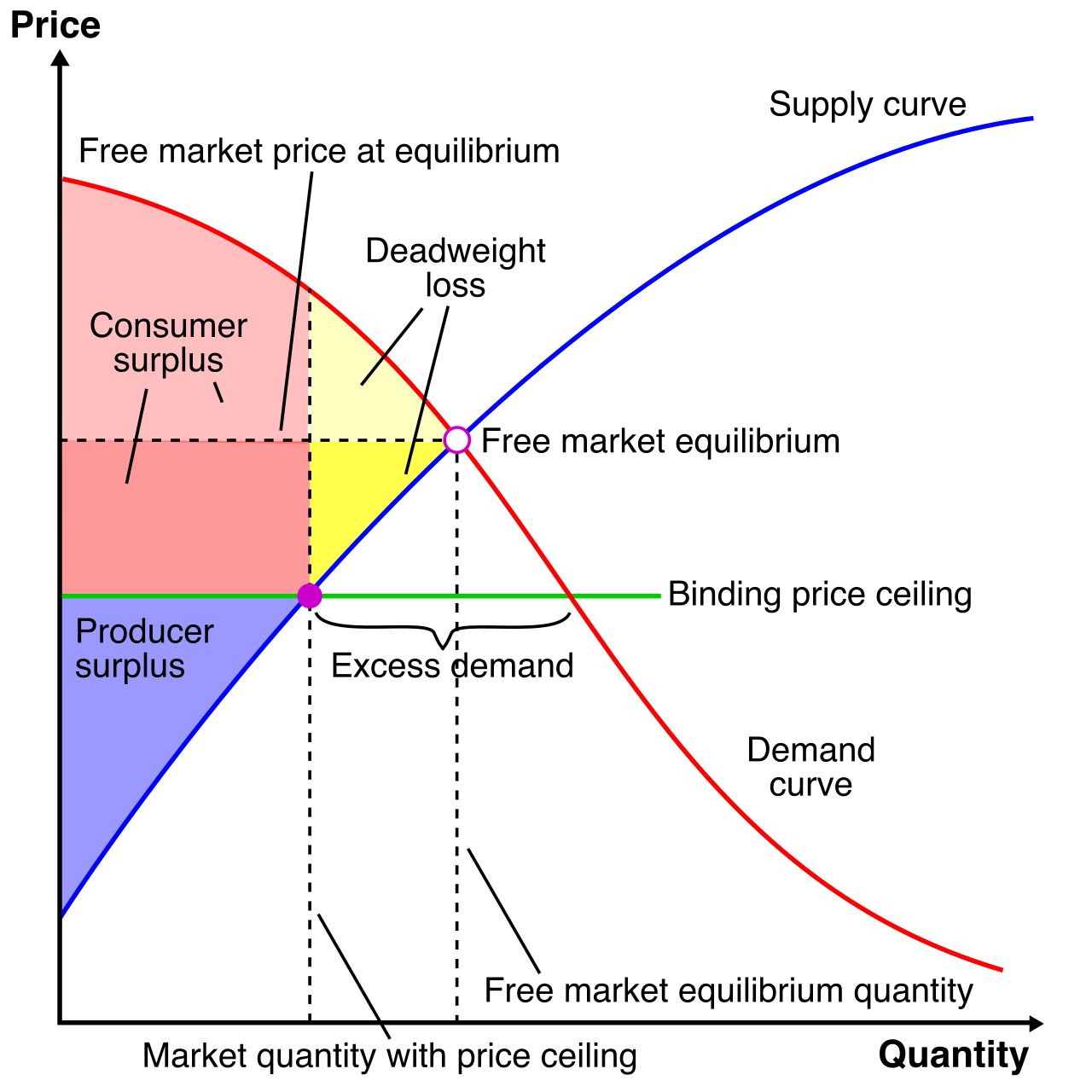

Governments often intervene because they believe the market equilibrium price is unfair.

A price ceiling is a legally established maximum price at which a good can be sold. To actually alter the market, a binding price ceiling is set below the free-market equilibrium price. Because the price is artificially low, consumers demand more than producers are willing to supply, meaning a binding price ceiling causes a market shortage.

- Historical/Civic Example: Rent control policies are standard examples of economic price ceilings. By legally capping apartment rents below market value, cities often experience severe housing shortages.

Conversely, a price floor is a legally established minimum price. A binding price floor is set above the free-market equilibrium price. Because the price is artificially high, producers supply more than consumers want to buy, meaning a binding price floor causes a market surplus.

- Historical/Civic Example: The federal minimum wage is an example of an economic price floor. If the minimum wage is set above the equilibrium wage for low-skilled labor, it results in a surplus of labor—commonly known as unemployment.

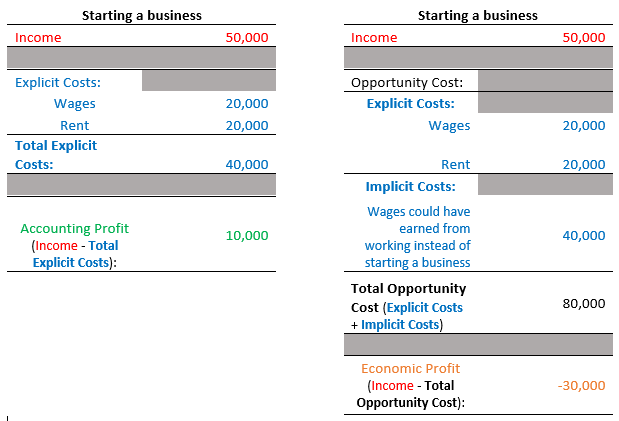

To understand how a business reacts to a market, we must first think like an entrepreneur. Imagine you decide to leave your $60,000-a-year teaching job to open a bakery. You invest $40,000 of your own money into flour, ovens, and labor.

At the end of the year, your bakery makes $80,000 in revenue. Should you celebrate?

- Your accountant says yes. Accounting profit is calculated as total revenue minus total explicit costs. Explicit costs are direct monetary out-of-pocket payments for business inputs (the $40,000 for flour and ovens). Your accounting profit is $40,000.

- An economist says no. Economists factor in implicit costs, which represent the opportunity cost of using resources already owned by a business firm. Your implicit cost is the $60,000 teaching salary you gave up. Economic profit is calculated as total revenue minus the sum of explicit costs and implicit costs.

Economic Profit = $80,000 (Revenue) - $40,000 (Explicit) - $60,000 (Implicit) = -$20,000.

You suffered an economic loss. Understanding the difference between accounting and economic profit is essential for explaining why businesses seemingly making a "profit" might still choose to shut down.

The Anatomy of Production Costs

As a firm produces goods, it encounters different types of costs:

- Fixed costs do not change with the level of business output. (e.g., Your bakery's monthly rent).

- Variable costs change proportionally with the level of business output. (e.g., The flour and sugar you buy to bake more cakes).

- Total business cost is simply the sum of fixed costs and variable costs.

- Average total cost (ATC) is calculated by dividing total cost by the quantity of output produced.

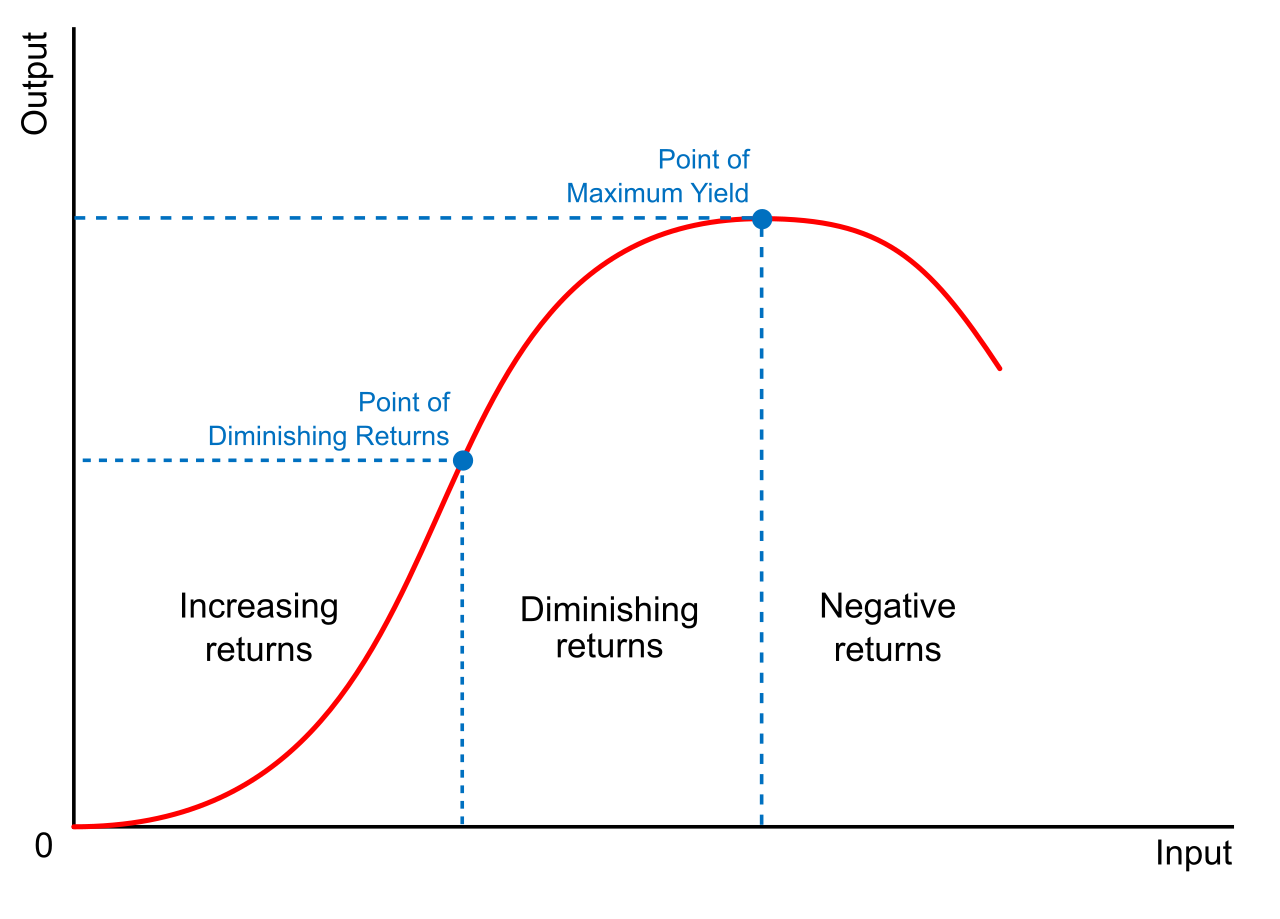

When making decisions, businesses focus on the margins. Marginal cost is the additional monetary cost incurred from producing one additional unit of output.

Why do marginal costs eventually rise? Because of the law of diminishing marginal returns, which states that adding more of a variable input (like bakers) to a fixed input (like one kitchen) eventually yields successively smaller increases in output. The first baker makes 10 cakes. The second baker makes 8. The fifth baker is just bumping elbows with the others, making only 1 extra cake.

Not all markets look the same. The behavior of a firm depends entirely on its environment. We classify these environments along a spectrum from perfect competition to absolute monopoly.

Perfect Competition: The Benchmark

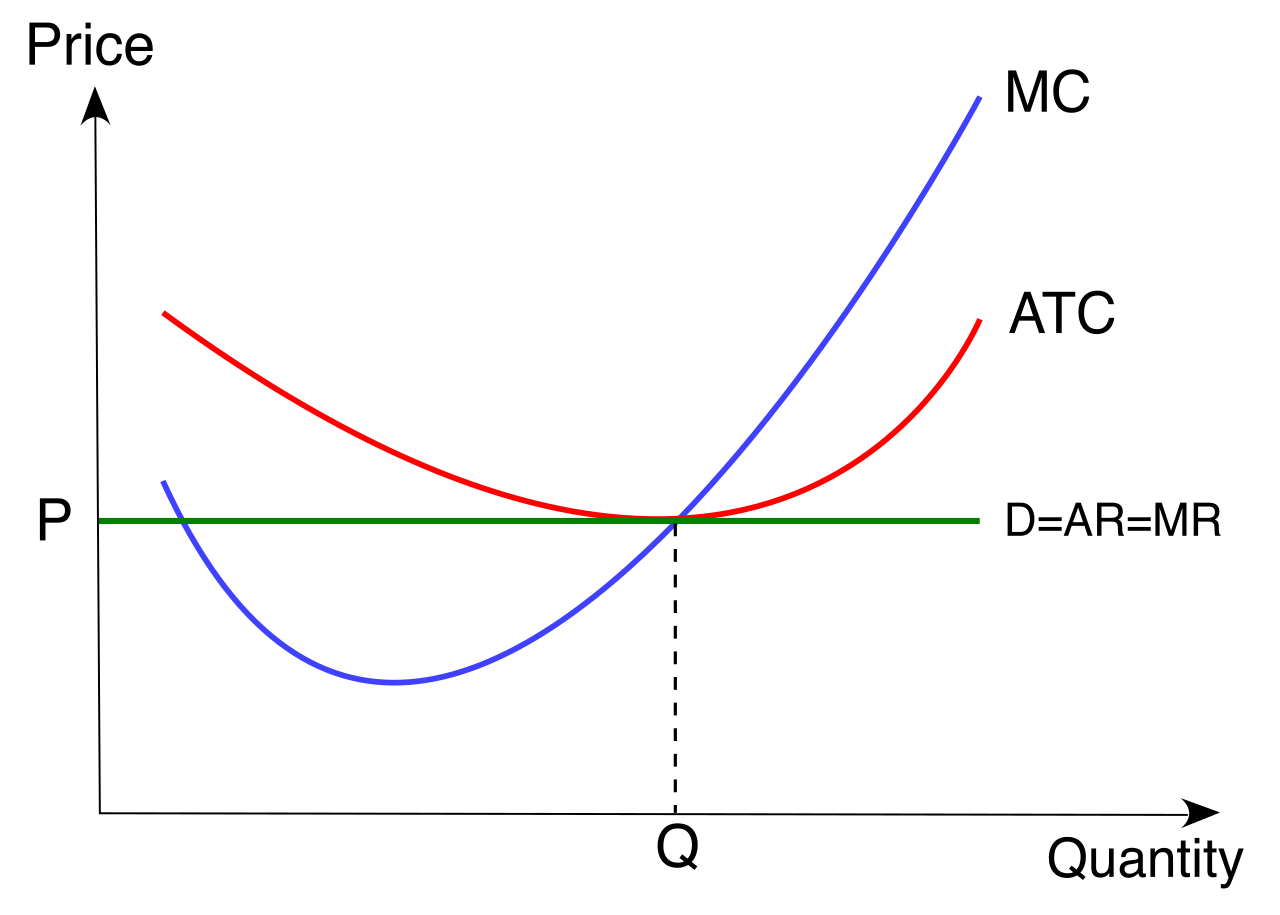

Perfect competition is a market structure characterized by many buyers and many sellers.

- Identical Goods: Firms in perfectly competitive markets sell completely identical products (think of millions of bushels of wheat).

- Market Power: Because products are identical, firms in perfectly competitive markets are market price takers. A price taker must accept the prevailing market equilibrium price. If a wheat farmer tries to charge one penny more than the market rate, buyers will simply buy from the thousands of other farmers.

- Entry and Exit: Perfectly competitive markets feature zero barriers to market entry or exit.

- Long-Run Reality: Because anyone can enter the market if there is money to be made, new firms rush in whenever there are profits, driving down prices. Consequently, firms in perfectly competitive markets earn exactly zero economic profit in the long run. (They earn enough to cover their explicit and implicit opportunity costs, but nothing more).

Monopoly: The Sovereign Seller

At the opposite extreme lies the monopoly, a market structure with a single seller of a highly unique product.

- Barriers: A monopoly faces extremely high barriers to market entry (patents, massive start-up costs, or control of a key resource).

- Market Power: Monopolies are price makers possessing the ability to independently set the market price.

- The Revenue Quirks: Because a monopoly represents the entire market, the only way it can sell more units is by lowering the price for everyone. Therefore, marginal revenue for a monopoly firm is always strictly less than the price of the good.

- Profit Maximization: To extract the maximum wealth, a monopoly uses a universal rule: A monopoly firm maximizes profit by producing the quantity where marginal revenue exactly equals marginal cost (MR = MC).

Sometimes, monopolies happen not through evil scheming, but through the sheer physics of infrastructure. Natural monopolies arise when a single firm can supply a good or service to an entire market at a lower total cost than two or more distinct firms.

- Historical/Civic Example: Municipal public utilities serve as common historical examples of natural monopolies. It is wildly inefficient to have three competing water companies laying three separate sets of pipes under the same city street.

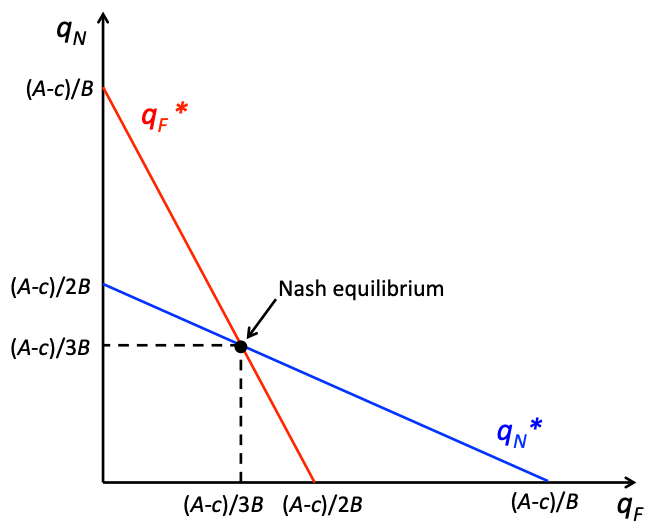

Oligopoly: The Game of Chess

Most major modern markets—airlines, cell phone providers, automobiles—fall into the category of oligopoly, a market structure dominated by a small number of large firms.

- Barriers: Oligopolistic markets possess significant barriers to entry, keeping new competitors at bay.

- The Core Trait: Firms in an oligopoly exhibit strong mutual interdependence. This means a firm's strategic decisions are significantly affected by the anticipated decisions of rival firms. If Delta Airlines lowers ticket prices, they must immediately calculate how United and American Airlines will react.

- Analytical Tools: Because oligopoly is fundamentally about strategy, game theory is frequently utilized by economists to mathematically analyze the strategic behavior of interacting firms in an oligopoly.

Because price wars destroy profits for everyone, firms in an oligopoly frequently attempt to engage in collusion to act collectively like a single monopoly. When they formalize this arrangement, it becomes a cartel—a formal agreement among competing firms to artificially fix prices or restrict output.

- Historical/Civic Example: The Organization of the Petroleum Exporting Countries (OPEC) functions globally as a modern economic cartel. By agreeing to restrict oil production, they artificially inflate the global price of oil, demonstrating how oligopolistic behavior shapes international relations and geopolitics.

Market Structures at a Glance

| Feature | Perfect Competition | Oligopoly | Monopoly |

|---|---|---|---|

| Number of Firms | Many | A small number of large firms | Single seller |

| Type of Product | Completely identical | Differentiated or identical | Highly unique |

| Market Power | Price taker | Mutual interdependence | Price maker |

| Barriers to Entry | Zero barriers | Significant barriers | Extremely high barriers |

| Long-Run Economic Profit | Exactly zero | Can be positive | Can be highly positive |

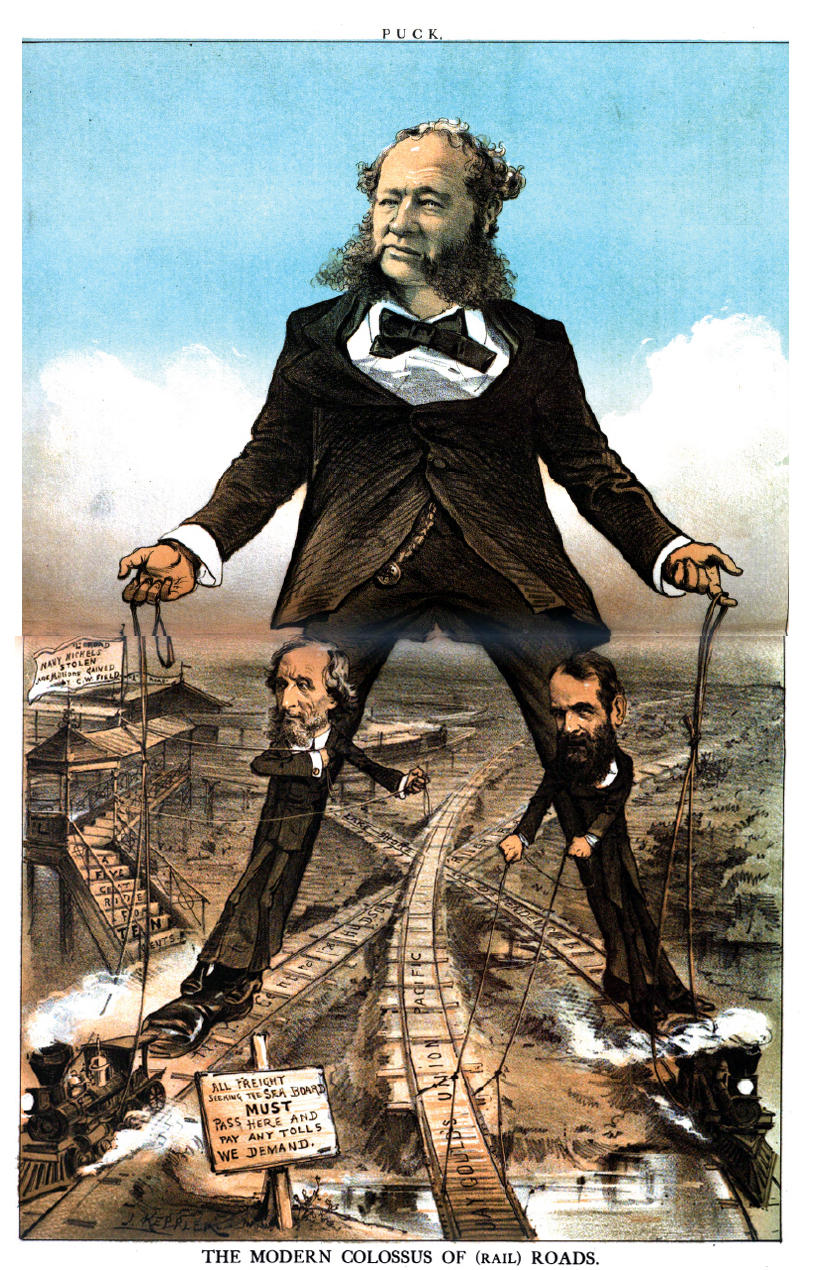

When you teach the Gilded Age, you aren't just teaching about men in top hats; you are teaching about monopolies manipulating price and quantity. When you teach the 1970s energy crisis, you are teaching the game theory of an oligopolistic cartel. When you teach the New Deal or the Progressive Era, you are exploring the tension between market efficiency and government intervention.

By mastering these concepts—the invisible architecture of surplus, cost, and competition—you equip your students with a lens to see past the noise of politics and grasp the foundational mechanics that drive human civilization forward.