Consumer protection laws

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

The modern financial system is a highly asymmetrical machine. On one side are massive institutional lenders, credit bureaus, and collection agencies operating with algorithmic efficiency; on the other side is the individual consumer. Without a counterbalance, this disparity in power would inevitably crush the individual. The body of consumer protection law is the structural counterbalance—the legal armor that prevents predatory practices and provides systematic relief when individuals are pushed to the brink. For a financial planner, mastering this legal framework is not merely an exercise in compliance. It is about understanding the exact specifications of the armor your clients wear, knowing precisely which assets are shielded during a catastrophic failure, and recognizing exactly when an institution has crossed a legal boundary so you can forcefully intervene on their behalf.

When a client’s debt becomes mathematically impossible to service, bankruptcy acts as an economic relief valve. It is not a moral failing; it is a legally structured reset. However, the exact nature of that reset depends entirely on the chapter of the bankruptcy code deployed.

Liquidation vs. Reorganization

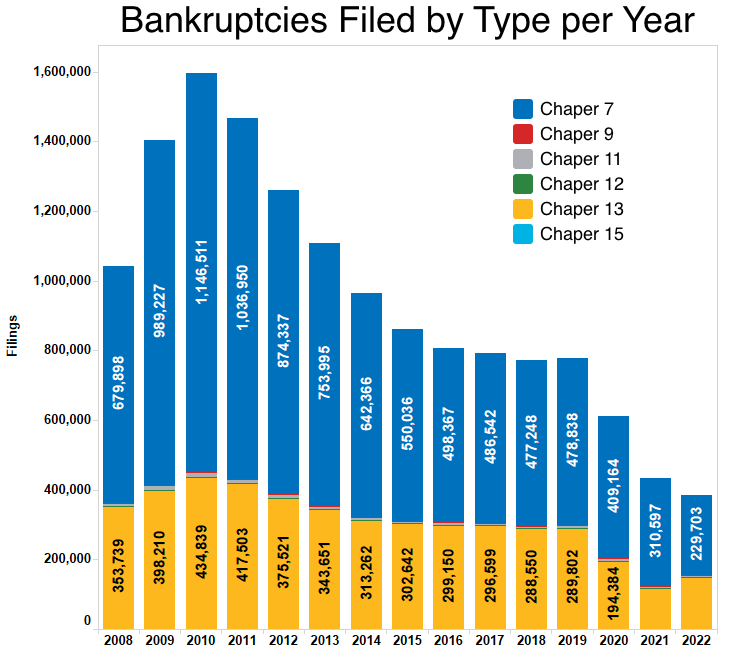

The most decisive wipeout of debt occurs under Chapter 7 bankruptcy, which involves the liquidation of a debtor's non-exempt assets to discharge unsecured debts. But a Chapter 7 discharge is not a free pass. To prevent high-income individuals from simply erasing debts they could afford to pay over time, the Bankruptcy Abuse Prevention and Consumer Protection Act (BAPCPA) established a strict means test to determine Chapter 7 bankruptcy eligibility.

If you have clients whose income exceeds the state median, they are subject to the Chapter 7 bankruptcy means test. If they fail the bankruptcy means test, they are categorically ineligible for Chapter 7 liquidation.

Debtors ineligible for Chapter 7 liquidation due to the means test may file for Chapter 13 bankruptcy. Instead of wiping the slate clean through liquidation, Chapter 13 bankruptcy allows individual debtors to retain their assets rather than liquidating them. In exchange, Chapter 13 bankruptcy requires individual debtors to repay a portion of their debts over a three-to-five-year plan. Naturally, to successfully execute this repayment plan, Chapter 13 bankruptcy requires the filing debtor to have a regular source of income.

If the client in trouble is a corporation rather than an individual, they will likely utilize Chapter 11 bankruptcy, which is primarily used by businesses to reorganize debt. The distinct power of Chapter 11 bankruptcy is that it allows a business to continue operations during debt reorganization, preserving the entity's ability to generate cash flow while restructuring its obligations.

Crucial Prerequisite: No matter which individual path is chosen, the law requires a moment of mandatory reflection and education. Individual debtors must complete mandatory credit counseling before filing for bankruptcy.

The Fortress: Asset Protection in Bankruptcy

When a client declares bankruptcy, their net worth is under siege. As a planner, you must know exactly which accounts act as impenetrable fortresses and which are vulnerable to creditors.

Under federal bankruptcy law:

- ERISA-qualified retirement plans (like 401(k)s) receive unlimited asset protection from creditors.

- SEP IRAs and SIMPLE IRAs also receive unlimited creditor protection.

- Traditional IRAs and Roth IRAs are protected in federal bankruptcy proceedings up to an inflation-adjusted limit.

- Rollovers: What happens if a client moves money from a 401(k) to an IRA? The shield moves with the money. Funds rolled over from a qualified employer plan to a Traditional IRA retain unlimited creditor protection in federal bankruptcy proceedings.

However, there is a massive structural vulnerability regarding inherited wealth. The Supreme Court ruled in Clark v. Rameker that inherited IRAs are not considered retirement funds because the beneficiary can withdraw the money at any time without penalty and cannot make ongoing contributions. Consequently, inherited IRAs lack federal bankruptcy creditor protection.

Beyond retirement accounts, debtors look to shield their homes and income:

- The Homestead Exemption: Debtors historically abused the system by moving to states with unlimited homestead exemptions (like Florida or Texas) right before filing. To stop this, federal bankruptcy law caps state homestead exemptions if the debtor acquired the property within 1,215 days before filing for bankruptcy.

- Exempt Income: Certain vital safety-net incomes are untouchable. Both Social Security benefits and disability benefits are completely exempt from liquidation in federal bankruptcy proceedings.

The Indestructible Debts

Just as certain assets are untouchable by creditors, certain debts are indestructible and survive the bankruptcy fire.

- Family Obligations: Both alimony debts and child support obligations are strictly non-dischargeable in bankruptcy proceedings.

- Education: Student loan debts are generally non-dischargeable in bankruptcy proceedings (requiring an exceptionally rare showing of "undue hardship" to overcome).

- Taxes: Income tax debts are not dischargeable in bankruptcy if the associated tax return was due within three years of the bankruptcy filing.

A client's credit report is their financial shadow. It dictates their ability to borrow, the rates they pay, and sometimes even their employment prospects.

The Fair Credit Reporting Act (FCRA)

The Fair Credit Reporting Act regulates the collection of consumer credit information and strictly governs how consumer credit information can be legally utilized.

Under the FCRA:

- Consumers have the right to request one free credit report every twelve months from each major credit bureau.

- If a client spots a hallucination in their credit data, the burden of proof shifts to the data brokers. Credit bureaus must investigate consumer disputes regarding inaccurate information within thirty days of the request.

- The Memory of the System: Negative credit information generally remains on a consumer's credit report for seven years. However, severe systemic failures carry a longer penalty: Chapter 7 bankruptcies and Chapter 11 bankruptcies can legally remain on a consumer's credit report for up to ten years.

- Transparency in Rejection: Lenders must issue an Adverse Action Notice to consumers denied credit based on credit report information, allowing the consumer to see exactly what data caused the rejection.

The Fair and Accurate Credit Transactions Act (FACTA)

Identity theft is a statistical inevitability in modern finance. The Fair and Accurate Credit Transactions Act arms consumers against this threat. It allows consumers to place fraud alerts on their credit files to mitigate identity theft.

FACTA also attacks point-of-sale vulnerabilities. It requires businesses to truncate credit card numbers on printed receipts. Specifically, printed retail receipts must display no more than the last five digits of a consumer's credit card number.

The Gramm-Leach-Bliley Act (GLBA)

Financial institutions hold a terrifying amount of private data. The Gramm-Leach-Bliley Act requires financial institutions to provide consumers with privacy notices that must detail the financial institution's information-sharing practices.

GLBA fundamentally shifted power back to the consumer through two vital rules:

- The Financial Privacy Rule grants consumers the right to opt out of having their non-public personal information shared with non-affiliated third parties.

- The Safeguards Rule requires financial institutions to implement physical and digital security measures to protect consumer data.

Furthermore, the GLBA explicitly prohibits pretexting, which is the practice of obtaining a consumer's personal financial information under false pretenses (e.g., a bad actor calling a bank and impersonating your client to steal data).

When clients borrow money, the true cost of that capital is often intentionally obscured by complex math and hidden fees. The law forces lenders to illuminate these metrics.

The Truth in Lending Act (TILA)

The Truth in Lending Act applies exclusively to consumer credit transactions (it does not protect business loans). TILA requires lenders to disclose two vital metrics to borrowers prior to issuing credit:

- The Annual Percentage Rate (APR)

- The total finance charges

TILA also guards against the predatory high-pressure sales tactics that historically cost people their homes. It grants consumers a three-day right of rescission for loans secured by their primary residence. The right of rescission allows borrowers to cancel a home-secured loan within three business days without financial penalty.

Why doesn't this break the real estate market? Because the Truth in Lending Act right of rescission does not apply to initial mortgages used to purchase a primary residence. If it did, home sales would be paralyzed for three days post-closing. It applies primarily to refinances and home equity loans.

The Equal Credit Opportunity Act (ECOA)

Lending decisions must be driven by mathematical reality, not prejudice. The Equal Credit Opportunity Act prohibits creditors from discriminating against credit applicants based on age, sex, or marital status. Crucially for lower-income clients, the Equal Credit Opportunity Act also prohibits lenders from denying credit solely because an applicant receives public assistance income.

To ensure efficiency and respect for the borrower's time, creditors must notify applicants of the approval or denial of their credit application within thirty days of receiving a completed application.

The Credit CARD Act of 2009

Credit card issuers used to arbitrarily hike interest rates on existing balances and allow unused gift cards to rapidly drain via hidden "inactivity fees." The Credit CARD Act of 2009 stopped this. It requires credit card issuers to provide at least forty-five days of advance notice before increasing a consumer's interest rate, and dictates that retail gift cards cannot expire for at least five years from the date of purchase.

This is one of the most mechanically critical distinctions a financial planner must understand. The laws protecting credit cards and debit cards are entirely different, reflecting the structural reality of the assets: a credit card spends the bank's money, while a debit card directly drains the client's actual cash.

The Fair Credit Billing Act (FCBA) - Credit Cards

Because a stolen credit card represents the bank's liability, the law gives the consumer heavy protection. The FCBA limits a consumer's liability for unauthorized credit card transactions to a maximum of $50.

For billing errors, strict timelines apply:

- Consumers must notify the creditor in writing of a billing error within sixty days after the first erroneous bill was mailed.

- Creditors must acknowledge a consumer's written billing error dispute within thirty days.

- Creditors must resolve a billing error dispute within two billing cycles.

- The absolute maximum time a creditor has to resolve a billing error dispute is ninety days.

The Electronic Fund Transfer Act (EFTA) - Debit Cards

The Electronic Fund Transfer Act governs consumer liabilities for unauthorized transactions involving debit cards. Because debit transactions instantly remove a client's hard-earned cash, the law heavily incentivizes the consumer to report fraud immediately via a brutal, sliding scale of liability:

| Time of Fraud Report | Consumer Liability Limit |

|---|---|

| Within 2 business days | Limited to $50 |

| Between 3 and 60 days | Jumps to $500 |

| After 60 days of the bank statement | Consumers risk unlimited liability for unauthorized debit card transactions |

If a client fails to read their bank statement for two months while a thief drains their checking account, the EFTA offers them absolutely no safety net. The money is simply gone.

When a client defaults, the system tries to recover the capital. Historically, debt collection was a brutal, unregulated industry.

The Fair Debt Collection Practices Act (FDCPA)

The Fair Debt Collection Practices Act restricts the methods third-party debt collectors can use to recover unpaid personal debts. Take careful note of the scope: The Fair Debt Collection Practices Act does not govern original creditors collecting their own debts; it only applies to third-party collection agencies who buy or are hired to collect the debt.

The FDCPA establishes rigid boundaries around a client's peace of mind:

- Time of day: Debt collectors are prohibited from contacting consumers before 8:00 AM local time or after 9:00 PM local time.

- Workplace harassment: Debt collectors cannot contact a consumer at their workplace if the collector knows the employer forbids such communication.

- Psychological warfare: Debt collectors are prohibited from using abusive language when communicating with consumers, and they cannot threaten a consumer with imprisonment for failure to pay a civil debt (since debtor's prisons are illegal).

- The Kill Switch: If a client is overwhelmed, they hold ultimate veto power over communication. Consumers can halt most third-party debt collector communications by sending a written cease-and-desist letter.

The Dodd-Frank Act and the CFPB

Following the catastrophic 2008 financial crisis, it became obvious that having dozens of fragmented agencies trying to enforce consumer protections was a failure. In response, the Dodd-Frank Wall Street Reform and Consumer Protection Act established a centralized watchdog: the Consumer Financial Protection Bureau (CFPB).

Today, the Consumer Financial Protection Bureau holds primary regulatory authority to enforce federal consumer financial protection laws. When a financial institution systematically violates the TILA, FCRA, or FDCPA, the CFPB is the apex predator that brings them to heel.