Financial services regulations and requirements

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Financial markets are invisible engines of capital, converting human ingenuity and saved wealth into economic progress. But unlike physical engines, which run on combustion and thermodynamics, financial engines run entirely on a fragile psychological construct: trust. If investors suspect the game is rigged, they withdraw their capital, and the engine seizes. The regulatory framework governing financial services is not merely a bureaucratic hurdle for planners to jump over; it is the structural engineering that keeps this engine running. For the financial planning professional, mastering these laws is not about memorizing acronyms for an exam. It is about understanding the exact boundaries of your professional role, the legal weight of the advice you dispense, and the mechanisms designed to protect the very public you serve.

To understand modern financial regulation, you have to look at the wreckage of the 1929 stock market crash. The federal government realized that sunlight and structural integrity were the only ways to restore faith in the system. They built the modern regulatory framework in two primary phases: regulating the birth of a security, and regulating its life.

The Securities Act of 1933: The Primary Market

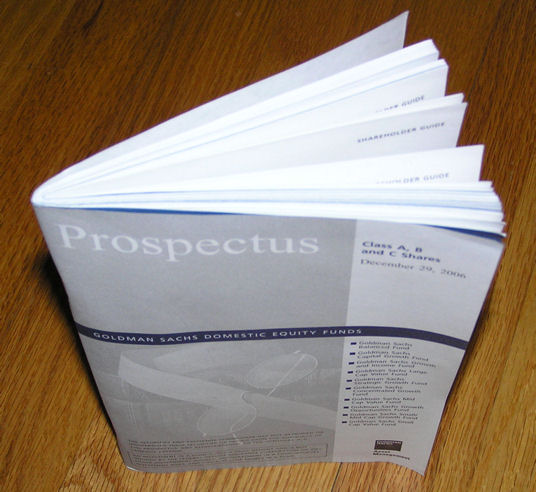

When a company wants to raise capital by issuing new stock to the public, it is asking for blind faith. The Securities Act of 1933 stepped in to regulate the issuance of new securities in the primary market.

Think of this Act as a "truth in labeling" law. Just as you wouldn't buy medicine without an ingredients list, the Securities Act of 1933 requires the delivery of a prospectus to prospective investors of new securities. The law doesn't guarantee the investment is good; it guarantees the investor has the accurate data needed to make an informed decision.

The Securities Exchange Act of 1934: The Secondary Market

Once a security is born and sold to its first owner, it begins its life trading hands among the public. The Securities Exchange Act of 1934 regulates the secondary trading of securities.

Because secondary markets involve millions of moving parts and participants, the 1934 Act did something monumental: The Securities and Exchange Commission was created by the Securities Exchange Act of 1934.

The SEC’s Tripartite Mission The primary mission of the Securities and Exchange Commission is to:

- Protect investors.

- Maintain fair, orderly, and efficient markets.

- Facilitate capital formation.

To ensure orderly trading, the Securities Exchange Act of 1934 requires broker-dealers to register with the Securities and Exchange Commission. It also takes direct aim at market manipulation. Specifically, the Securities Exchange Act of 1934 prohibits insider trading.

Definition: Insider Trading Insider trading involves buying or selling a security while in possession of material, nonpublic information about that security. If the market is a poker game, insider trading is looking at the dealer's deck. It destroys the fairness the SEC is mandated to protect.

By 1940, it became clear that everyday investors needed a way to buy diversified baskets of stocks, leading to the rise of pooled investments. The Investment Company Act of 1940 regulates the organization of companies that engage primarily in investing in securities. Most crucially for your day-to-day practice, the Investment Company Act of 1940 governs the operations of mutual funds, ensuring these pooled vehicles have transparent structures, fair pricing, and strict limits on leverage.

If the 1933 and 1934 Acts regulate the products and the markets, the Investment Advisers Act of 1940 regulates the people interpreting those markets for clients. It regulates individuals and firms that provide investment advice for compensation.

To determine who falls under this rigorous regulatory umbrella, the SEC applies a foundational filter. An investment adviser must meet the three-prong test:

- Providing advice (or analysis concerning securities).

- Being in the business of providing advice (holding oneself out to the public as an adviser).

- Receiving compensation (charging a fee, whether flat, hourly, or asset-based).

The Duty of a Fiduciary

If you meet this test, you are held to the highest standard in law. Investment advisers are bound by a fiduciary duty to their clients under the Investment Advisers Act of 1940. Think of a fiduciary not as a salesperson, but as a financial physician.

The fiduciary duty of an investment adviser includes:

- A Duty of Care: You must provide advice that is in the client's best interest, based on a rigorous understanding of their financial profile.

- A Duty of Loyalty: You must eliminate, or fully disclose, all conflicts of interest. Your client's financial well-being must completely subordinate your own.

Exclusions to the Definition

Not everyone who casually mentions a stock is an investment adviser. The law provides specific, narrow exclusions for professionals whose advice is ancillary to their actual job.

- The L.A.T.E. Professionals: Lawyers, Accountants, Teachers, and Engineers providing investment advice that is solely incidental to their professional practice are excluded from the definition of an investment adviser. If a divorce attorney explains how a stock split works during settlement negotiations, she is acting as a lawyer, not an adviser.

- The Publisher Exclusion: Publishers of bona fide financial publications of regular and general circulation (like The Wall Street Journal) are excluded from the definition of an investment adviser, because their advice is not tailored to the specific portfolios of individual readers.

- The Broker-Dealer Exclusion: Broker-dealers whose investment advisory services are solely incidental to the conduct of their business are excluded from the definition of an investment adviser. However, the broker-dealer exclusion from the definition of an investment adviser requires that the broker-dealer receives no special compensation for the investment advice. If they charge a separate fee for the advice itself, they cross the line and become an adviser.

If investment advisers are the fiduciaries managing portfolios for a fee, broker-dealers are the mechanisms executing trades and facilitating market liquidity.

Because broker-dealers facilitate the physical plumbing of the markets, they are overseen by the Financial Industry Regulatory Authority (FINRA). The Financial Industry Regulatory Authority oversees broker-dealers in the United States. Crucially, FINRA is not a government agency; the Financial Industry Regulatory Authority is a self-regulatory organization (SRO). It operates under the oversight of the Securities and Exchange Commission, acting as the referee on the field while the SEC sits in the league office.

Regulation Best Interest (Reg BI)

For decades, the standard for broker-dealers was merely "suitability"—recommending products that fit the client's risk profile, even if they paid the broker a higher commission. This has changed.

Today, broker-dealers are subject to the Securities and Exchange Commission Regulation Best Interest standard of conduct.

Regulation Best Interest requires a broker-dealer to act in the best interest of the retail customer at the time a recommendation is made. While not a continuous fiduciary duty (like an RIA has), Regulation Best Interest prohibits a broker-dealer from placing its financial or other interest ahead of the interest of the retail customer during that transaction.

Just as the US has federal and state laws, financial regulation is bifurcated. State-level securities regulations are commonly referred to as Blue Sky Laws—originally coined because regulators wanted to stop hucksters from selling speculative investments backed by nothing more than "so many feet of blue sky."

To prevent 50 entirely different sets of rules, the Uniform Securities Act serves as model legislation for state-level securities regulations, providing a template that states can adopt and adapt. Overseeing this at a macro level is the North American Securities Administrators Association (NASAA), which represents state and provincial securities regulators in the United States, Canada, and Mexico.

The Weight of Assets: Where Do You Register?

Investment advisers do not register with everyone; they are divided by the size of their footprint, measured by Assets Under Management (AUM).

| AUM Threshold | Regulatory Jurisdiction |

|---|---|

| Less than $25 million | Investment advisers with less than twenty-five million dollars in assets under management generally must register with state securities regulators. |

| Between $90 million and $110 million | Investment advisers with assets under management between ninety million dollars and one hundred ten million dollars may choose to register with either state regulators or the Securities and Exchange Commission. |

| $110 million or more | Investment advisers with one hundred ten million dollars or more in assets under management must register with the Securities and Exchange Commission. |

Sunlight is the best disinfectant. To ensure clients know exactly who is advising them and how they are paid, Registered Investment Advisers (RIAs) must electronically file Form ADV with the Securities and Exchange Commission or state securities authorities.

The anatomy of this disclosure is critical for the CFP exam:

- Form ADV Part 1: This is the raw data. It contains information about the investment adviser business ownership, clients, employees, and disciplinary history. It is highly formatted and searchable by regulators.

- Form ADV Part 2A: This is the client-facing narrative. Form ADV Part 2A requires investment advisers to create a narrative brochure detailing their advisory services, fees, and conflicts of interest. Timing matters: Registered Investment Advisers must deliver the Form ADV Part 2A brochure to a client before or at the time of entering into an advisory contract.

- Form ADV Part 2B: This gets personal. Form ADV Part 2B requires investment advisers to provide brochure supplements containing information about the specific individuals providing advisory services to the client (their education, background, and outside business activities).

To bridge the gap between broker-dealers and investment advisers, regulators introduced Form CRS (Client Relationship Summary). Form CRS is a brief relationship summary that broker-dealers and investment advisers must deliver to retail investors, outlining the nature of the relationship, the standard of conduct, and how the firm makes money.

Institutionalizing Ethics

Finally, a fiduciary duty cannot exist solely as a philosophical concept; it must be operationalized. The Investment Advisers Act of 1940 requires Registered Investment Advisers to designate a Chief Compliance Officer (CCO) to ensure the rules are followed.

Furthermore, Registered Investment Advisers must adopt and implement written policies and procedures designed to prevent violations of the Investment Advisers Act of 1940. They must also establish, maintain, and enforce a written code of ethics, legally binding their practitioners to the highest standards of the profession.

By internalizing these regulations, you do not just pass an exam—you protect the integrity of the financial engine, ensuring the capital markets remain a fair, transparent, and trustworthy space for the clients who depend on you.