Crisis events with severe consequences

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

When a meticulously engineered bridge is suddenly struck by a seismic shock, structural engineers do not immediately consult their blueprints to review the upcoming ten-year maintenance schedule. They deploy to the site, assess structural integrity, and ensure the bridge will not collapse before morning. Financial planning operates under the exact same physical reality. A comprehensively modeled Monte Carlo simulation is entirely irrelevant to a client standing in the smoldering ashes of their home, or one staring blankly at a devastating medical diagnosis. In these acute moments, long-term wealth accumulation is paused. Your only objective is stabilization.

For decades, the financial planning profession viewed itself purely through the lens of quantitative mechanics—tax alpha, asset allocation, and cash flow optimization. However, recognizing that human behavior is the actual engine of financial success or failure, The Psychology of Financial Planning became a principal knowledge domain tested on the CFP certification exam beginning in March 2022.

Within this newly mandated domain, crisis events with severe consequences represent one of the six primary categories you must master.

A crisis event in financial planning is defined as an unexpected occurrence that severely threatens a client's financial stability or emotional well-being.

These events rupture the normal cadence of life. As a CFP® professional, you are not merely a numbers tactician; you are the first responder to your client’s financial continuity.

When a crisis strikes, the human brain shifts into survival mode. Acute emotional stress temporarily impairs a client's cognitive ability to process complex financial information. You cannot present a fifty-page financial plan to a widow the day after her spouse’s funeral. The prefrontal cortex—the logical, calculating center of the brain—is neurologically hijacked by the amygdala.

Furthermore, clients dealing with catastrophic disruption frequently suffer from transition fatigue, which is the physical and emotional exhaustion a client experiences when navigating the complex aftermath of a severe crisis. They are fielding calls from insurance adjusters, hospitals, family members, and attorneys.

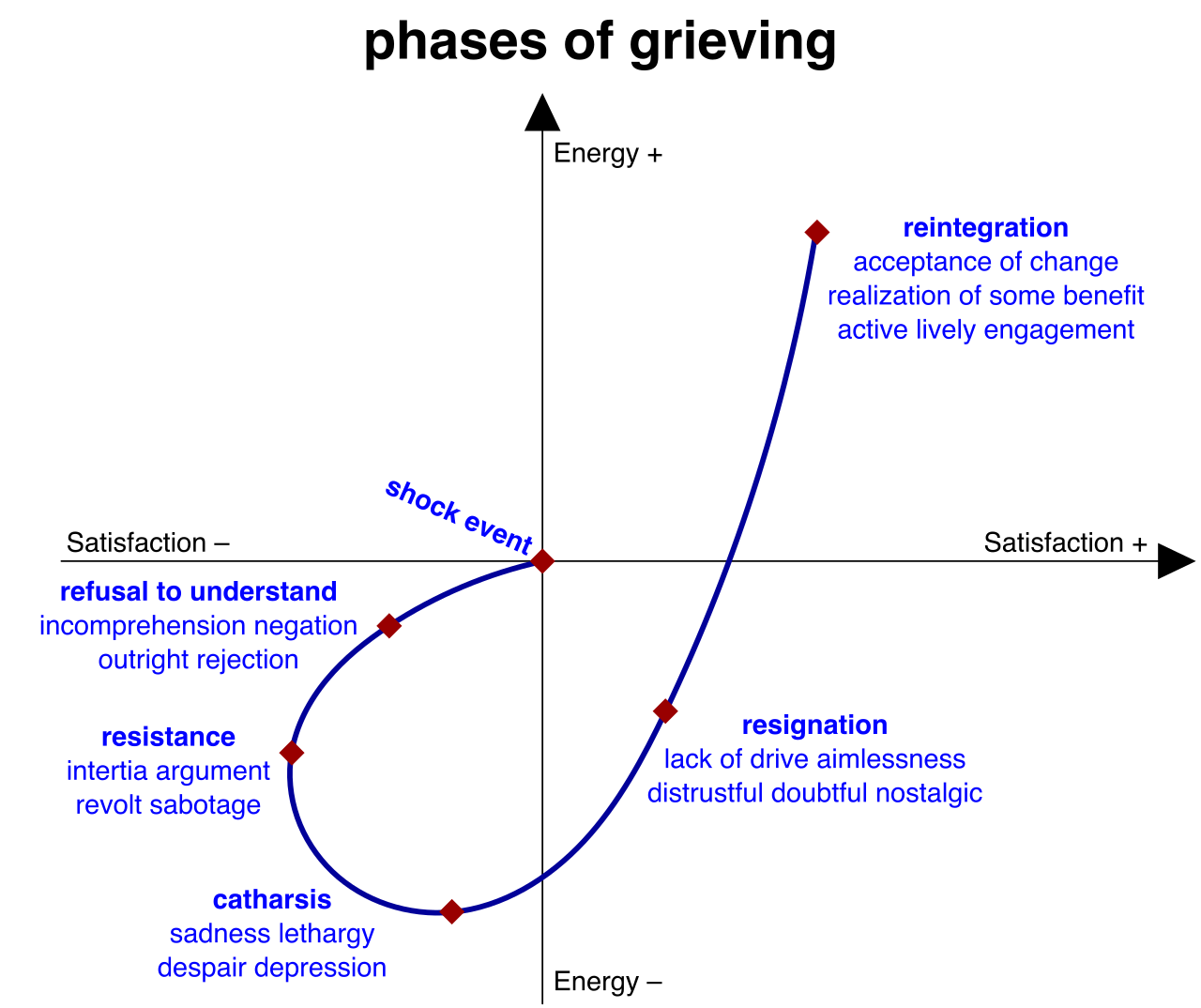

The Kübler-Ross Stages of Grief

To anticipate your client's behavioral responses, we rely on a foundational framework. Psychiatrist Elisabeth Kübler-Ross introduced the foundational five stages of grief model in 1969. Originally developed to understand terminal illness, the Kübler-Ross model outlines five distinct stages of grief comprising denial, anger, bargaining, depression, and acceptance.

Financial planners must identify these stages to tailor their immediate guidance:

| Stage | Manifestation in Financial Planning |

|---|---|

| Denial | The Kübler-Ross denial stage involves the client rejecting the reality or the severity of the financial crisis event. Example: A suddenly unemployed executive refusing to cut discretionary spending because they "will find a better job by next week." |

| Anger | The Kübler-Ross anger stage manifests as the client projecting frustration onto external factors, market conditions, or individuals. Example: A client blaming the Federal Reserve or their ex-spouse for their newly decimated net worth. |

| Bargaining | The Kübler-Ross bargaining stage involves the client attempting to negotiate a reversal of the crisis through hypothetical scenarios. Example: "If I just day-trade these tech options, I can win back the money lost in the divorce." |

| Depression | The Kübler-Ross depression stage is characterized by profound sadness and a withdrawal from financial planning activities. Example: The client ignores emails, leaves bills unopened, and stops caring about portfolio balances. |

| Acceptance | The Kübler-Ross acceptance stage occurs when the client acknowledges the reality of the crisis and begins to engage constructively in future planning. This is the stage where long-term financial planning can safely resume. |

Because acute stress creates a severe cognitive bottleneck, financial planners must use simplified communication and eliminate industry jargon when a client experiences the immediate shock of a crisis. Speak in plain terms. Do not say "We need to re-evaluate your standard deviation and sequence of returns risk." Say, "We need to make sure your cash is safe and accessible."

Empathy vs. Sympathy

Your communication stance must be anchored in empathy, which is vastly different from sympathy.

- Sympathy involves feeling pity for a client's misfortune without actively sharing or understanding their underlying emotional experience. Sympathy separates you from the client ("I feel sorry for you").

- Empathetic responding involves acknowledging a client's feelings without expressing judgment or offering unsolicited reassurance. Empathy puts you in the foxhole with them ("This is incredibly overwhelming, and it makes complete sense that you are angry").

The Mechanics of Active Listening

Active listening requires a financial planner to validate a client's emotions before attempting to provide logical financial solutions. You cannot solve a math problem if the client is still trapped in an emotional problem. To deploy active listening effectively, utilize two distinct techniques:

- Mirroring is a communication technique where the financial planner repeats the client's exact words to demonstrate active listening during a crisis. (Client: "I feel like I'm drowning." Planner: "You feel like you're drowning.")

- Paraphrasing involves the financial planner restating the client's emotional crisis narrative in the planner's own words to confirm understanding. (Planner: "It sounds like you're carrying the weight of the entire family's future on your shoulders right now.")

The Danger of Toxic Positivity

In a desperate attempt to comfort a grieving client, amateur planners often resort to platitudes: "Everything happens for a reason," or "At least you still have your health." Planners must avoid utilizing toxic positivity when a client experiences a severe crisis event.

Toxic positivity is the dismissal of a client's negative emotions through false reassurances or forced optimism. It invalidates the client's reality, damages trust, and stifles the necessary grieving process.

In medical emergencies, trauma surgeons perform triage—addressing arterial bleeding before setting a broken finger. Financial planning requires the exact same discipline.

Financial triage is the process of addressing a client's immediate critical financial needs before focusing on long-term wealth goals.

Financial triage follows a rigorous, three-phase framework:

- The Assessment Phase: This phase evaluates the overall severity of the crisis and identifies the immediate financial impacts. What has fundamentally changed today?

- The Inventory Phase: This phase compiles a comprehensive list of all accessible liquid resources and immediate liabilities. Exactly how much cash can we access by 5:00 PM on Friday?

- The Prioritization Phase: This phase ranks financial issues to ensure basic survival needs are funded first.

Executing the Prioritization Phase

During triage, a financial triage plan categorizes client expenses into essential survival costs and non-essential discretionary spending.

In a crisis, the hierarchy of money changes entirely. Securing basic needs such as housing, food, and healthcare takes strict precedence over unsecured debt repayment during financial triage. If a client has lost their income, paying a credit card bill while facing eviction is a catastrophic misallocation of scarce resources. Credit scores can be repaired later; starvation and homelessness cannot.

To preserve cash, suspending automated non-essential financial outflows is a critical initial step to preserve cash flow during a sudden job loss. Cancel subscription services, pause automated brokerage contributions, and halt aggressive debt paydowns.

Sources of Emergency Liquidity

Where do we find the cash to survive the crisis?

- The Baseline Defense: Establishing an emergency fund before a crisis occurs provides a critical liquidity buffer that reduces the immediate urgency of financial triage.

- Secondary Reserves: If cash reserves are dry, cash value life insurance policies can serve as an emergency liquidity source during severe financial crises (via tax-free policy loans or withdrawals to basis).

- The Last Resort: Tapping retirement accounts during a financial crisis must be treated as a last resort due to potential early withdrawal penalties and tax consequences.

A central tenet of crisis planning is preventing the client from making permanent mistakes based on temporary emotions. The do no harm principle in financial crisis planning dictates delaying irrevocable financial decisions during a client's acute emotional distress.

Do not let a widow sell her house three weeks after her husband's death. Do not let a suddenly unemployed executive liquidate their entire 401(k) to start a speculative business. To enforce this, establish a decision-free zone, which is a temporary period following a crisis during which a financial planner advises a client to avoid making major financial changes.

The CFP® exam will test your ability to apply these frameworks to highly specific, high-stress scenarios. Here is how financial triage adapts to different crises:

Sudden Wealth Loss

Sudden wealth loss is a financial crisis characterized by the abrupt depletion of assets due to market crashes, business failures, or theft.

- Triage Protocol: The shock is visceral. The immediate priority during sudden wealth loss is securing sufficient liquidity to cover essential living expenses. Halt all non-essential outflows and run an immediate inventory of surviving liquid assets.

Sudden Job Loss

- Triage Protocol: In addition to freezing automated outflows, a sudden loss of employment requires an immediate evaluation of the client's eligibility for COBRA health insurance continuation. Lapsing on healthcare coverage during a period of zero income turns a financial crisis into an existential one.

Natural Disasters and Destroyed Homes

When a wildfire or hurricane destroys a client's home, the payout is rarely as robust as the client expects. A reconstruction deficit occurs when a property insurance settlement falls short of the actual rebuilding costs.

- Why does this happen? Mandatory building code updates and construction inflation are primary causes of a reconstruction deficit following a natural disaster. The policy pays based on old cost metrics, but local laws demand modern, expensive materials.

- Triage Protocol: Because funds will likely fall short, financial triage planning for a destroyed home prioritizes structural integrity and essential systems over cosmetic finishes. You must ensure the house has a roof, plumbing, and electricity before approving expenditures for marble countertops.

Sudden Divorce

- Triage Protocol: In acrimonious splits, joint accounts can be drained overnight. Financial triage during a sudden divorce prioritizes the immediate securing of individual liquid assets to prevent unauthorized depletion by an estranged spouse. Work with the client’s attorney to safely establish individual accounts and redirect direct deposits.

Sudden Severe Medical Diagnosis

- Triage Protocol: A sudden severe medical diagnosis requires a financial planner to immediately review the client's health insurance coverage and out-of-pocket maximums. You must instantly quantify the maximum financial exposure for the year so you can ring-fence that specific dollar amount from liquid reserves.

Sudden Death of a Spouse

- Triage Protocol: Amidst the profound grief, bureaucratic gears must turn. The sudden death of a spouse requires the immediate collection of multiple official death certificates to facilitate the rapid transfer of survivor benefits. Life insurance claims, Social Security survivor benefits, and bank account retitlings all require original certificates. Secure them immediately to prevent liquidity bottlenecks.

While you will be a stabilizing force for your clients during the worst moments of their lives, you are not a doctor. Financial planners must recognize the boundaries of their professional competence regarding client mental health.

Providing empathetic financial guidance is a fiduciary duty; diagnosing clinical depression is a profound ethical breach. A financial planner acting as a psychological therapist violates the CFP Board Code of Ethics and Standards of Conduct.

If you notice a client exhibiting symptoms that go beyond normal acute grief—such as self-harm ideation, complete inability to function for prolonged periods, or debilitating panic—you have a professional mandate. Financial planners must provide a referral to a licensed mental health professional when a client exhibits signs of severe depression or trauma. Keep a vetted list of local therapists, grief counselors, and crisis hotlines in your professional network.

By mastering financial triage and crisis psychology, you ensure that when the unthinkable happens, your clients do not have to face the storm alone. You secure their present reality so that, eventually, they can return to planning for their future.