General principles of effective communication

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

A financial plan is only as robust as the data upon which it is built, yet the most critical data points in a client's life—their fears, aspirations, and hidden biases—are rarely handed over on a neatly formatted balance sheet. They are encoded in hesitations, shifting postures, and passing remarks. Effective communication in financial planning is not merely a soft skill; it is the primary diagnostic tool used to extract, decode, and verify the human variables that dictate financial strategy. To build a plan that survives the stress tests of market volatility and personal tragedy, the planner must master the architecture of human interaction: extracting truth through precision questioning, decoding layered emotional meaning, and reflecting comprehension to build unshakeable trust.

Many novice financial planners mistake hearing for listening. Hearing is a passive physiological event—sound waves striking the eardrum. Active listening, by contrast, is a rigorous cognitive process.

Active listening requires fully concentrating on the speaker rather than passively hearing the message. Think of your attention as a spotlight; active listening demands keeping that spotlight fixed entirely on the client, rather than letting it drift to the Monte Carlo simulation you plan to run later. It is a multi-step mental mechanism that requires the listener to actively comprehend the speaker's complete message, parsing not just the numbers, but the intent behind them.

Furthermore, comprehension is useless if the data is lost. Active listening requires the listener to retain and remember what the speaker communicated. If a client mentions in passing that they are worried about their daughter's health, and you fail to retain that information for future estate planning discussions, you have failed the active listening test. Finally, the loop must be closed: active listening requires the listener to provide appropriate feedback to the speaker, signaling that the message was received, decoded, and valued.

Attending Behaviors: The Visual Proof of Attention

How does a client know you are actively listening? Through attending behaviors—physical cues that visually demonstrate the listener is actively engaged in the conversation. If you are staring at your legal pad while the client pours out their retirement anxiety, the communication chain breaks.

Two foundational attending behaviors establish immediate engagement:

- Maintaining consistent eye contact is an attending behavior that conveys active listening to the speaker. It signals that they have your undivided focus.

- Leaning slightly forward is an attending behavior that signals interest and focus to the speaker. It is a biological cue that says, "I am moving closer to the source of information because it is important to me."

When a client speaks, they are transmitting data across three distinct channels simultaneously. A masterful financial planner monitors all three frequencies to capture the complete picture.

1. Verbal Communication

Verbal communication consists strictly of the actual words spoken by an individual. If we were to read a transcript of a client meeting, we would only be analyzing the verbal communication. While essential for gathering concrete facts (like the balance of an IRA), words alone are surprisingly inefficient at conveying emotion.

2. Paraverbal Communication

Paraverbal communication refers to the specific tone utilized while speaking. It is the audio metadata of the conversation. Specifically, paraverbal communication includes:

- The pitch of the speaker's voice (e.g., a high pitch indicating stress or excitement).

- The pace at which the speaker talks (e.g., rapid speech suggesting anxiety, or slow speech suggesting reluctance).

- The volume of the speaker's voice (e.g., dropping to a whisper when discussing financial embarrassment).

3. Non-Verbal Communication

Non-verbal communication encompasses physical cues such as body language and facial expressions. It includes the speaker's physical posture during a conversation—are they slumping in defeat, or sitting rigid with defensive tension? It also crucially includes the speaker's level of eye contact, which can indicate confidence, shame, or distraction.

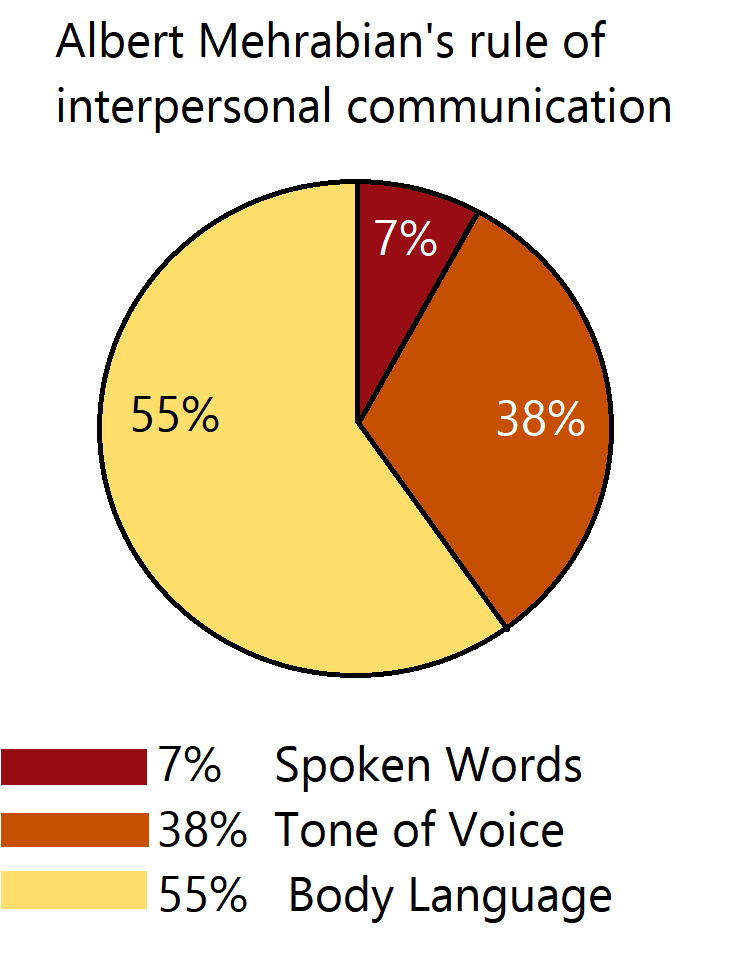

The Mehrabian Model: Where Meaning Truly Resides

Why must we monitor all three channels? Because human beings are remarkably bad at hiding their true feelings, provided you know where to look.

Albert Mehrabian's Communication Model When interpreting emotional meaning, Albert Mehrabian’s communication model posits that:

- 55 percent of emotional meaning in communication is conveyed through body language (Non-verbal).

- 38 percent of emotional meaning in communication is conveyed through vocal tone (Paraverbal).

- 7 percent of emotional meaning in communication is conveyed through the actual spoken words (Verbal).

Consider a scenario where you suggest a client delay retirement by two years. The client crosses their arms tightly, looks down at the table, sighs heavily, and mutters, "I guess that's fine."

If you only listen to the 7% (the words "that's fine"), you will update the financial plan and move on, oblivious to the impending client departure. A mismatch between a client's verbal statements and non-verbal cues often indicates hidden emotional concerns. When the words say "yes" but the posture and tone scream "no," the elite financial planner stops, pivots, and investigates the non-verbal data.

| Modality | What it is | Mehrabian's Weight (Emotional Meaning) | Planner Focus |

|---|---|---|---|

| Verbal | The actual words spoken | 7% | Extracting objective facts and figures. |

| Paraverbal | Tone, pitch, pace, volume | 38% | Detecting stress, confidence, or hesitation. |

| Non-Verbal | Posture, facial expressions, eye contact | 55% | Reading true comfort levels and unspoken fears. |

Financial planners extract information using specific conversational tools. Just as a surgeon uses different scalpels for different tissues, a planner must use different question types for different phases of discovery.

Open-Ended vs. Closed-Ended Questions

When you are mapping a client's financial universe, you need floodlights. Open-ended questions encourage clients to provide detailed explanations and broader context. By design, they cannot be answered with a simple "yes" or "no."

Open-ended questions typically begin with words like how, what, or why.

- Example: "What are your greatest concerns about leaving a legacy to your children?"

Conversely, when you need to pin down exact coordinates, you use a laser pointer. Closed-ended questions are designed to elicit a simple yes or no response. In our profession, closed-ended questions are used by financial planners to confirm specific factual data points.

- Example: "Do you have umbrella liability insurance?"

If a client gives you an answer that is muddy or contradictory, you deploy a third tool: Clarifying questions are utilized to resolve ambiguous or confusing statements made by the client.

- Example: "You mentioned you want to 'play it safe' with this $500,000 inheritance, but you also want 'market-beating growth.' Can you clarify what 'playing it safe' means to you?"

The Power of the Void: Silence as a Tool

Novice planners are terrified of silence; they rush to fill dead air with jargon. Elite planners wield silence like an instrument.

Silence is an active listening technique that provides the client with uninterrupted time to process complex emotions. If a client realizes during a meeting that they have severely underfunded their retirement, they need cognitive space to absorb that shock. Talking over them prevents processing. Furthermore, strategic silence encourages the client to continue speaking and elaborate further on a topic. Human beings naturally abhor a conversational vacuum; if you ask a difficult question, receive a brief answer, and simply wait, the client will almost always offer deeper, more revealing context to fill the quiet.

Understanding a client is only half the equation; the client must know you understand them. If they do not feel understood, they will not trust your recommendations, no matter how mathematically sound your tax alpha or asset allocation might be.

Paraphrasing and Summarizing

To prove cognitive understanding, we use two related, but distinct, feedback mechanisms.

Paraphrasing involves the financial planner restating the client's message using different words. This is critical: if you just act as a parrot and repeat their exact words, you prove only that your ears work. Paraphrasing demonstrates to the client that the financial planner accurately comprehends the client's message.

- Client: "I'm so sick of watching the news and seeing the market tank. I just want out."

- Planner (Paraphrasing): "It sounds like the daily volatility is causing you a lot of stress, and you're looking for a way to protect your principal."

When a client has been speaking for a long time—perhaps outlining their entire chaotic family business history—you must synthesize the data. Summarizing consists of condensing the client's extended statements into the most essential points. This organizes the narrative and confirms that you have captured the macro-level themes.

Reflective Listening and Empathy

Financial planning is inherently emotional. Money represents security, legacy, ego, and survival. Reflective listening involves identifying and verbally acknowledging the client's underlying emotions. You are acting as a mirror for their feelings.

When you reflect an emotion, you are demonstrating empathy. In a professional context, empathy in communication involves recognizing and validating the client's feelings without requiring agreement with those feelings. You do not have to agree that the client should liquidate their entire portfolio out of panic, but you must validate the sheer terror they feel during a 30% market drawdown. Saying, "I can see how terrifying it is to watch your life savings drop," validates the emotion without endorsing a poor financial action.

Subconscious Rapport: The Art of Mirroring

While reflective listening mirrors emotions verbally, physical mirroring operates beneath the client's conscious awareness. Mirroring is a technique where the financial planner subtly mimics the client's physical body language. If the client rests their chin on their hand, a few moments later, you might naturally adopt a similar posture.

Why do this? Because humans are biologically wired to trust those who resemble them. Mirroring helps establish subconscious rapport between the financial planner and the client. It sends a primal, non-verbal signal that says, "We are in sync; we are on the same side of the table."

Mastering the principles of effective communication transforms the financial planner from a mere human calculator into a trusted fiduciary architect. By deploying active listening, interrogating the spaces between words, and reflecting both meaning and emotion, you uncover the true variables of your client's life. Only then can you build a financial plan that truly serves them.