Function, purpose, and general structure of financial institutions

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Capital, left to its own devices, is inert. To drive an economy, a dollar saved by a teacher in Ohio must efficiently find its way into the hands of an entrepreneur building a factory in Texas. In the broader economy, financial institutions act as market intermediaries connecting parties with surplus capital to parties needing capital. Without these structures, a consumer would have to personally locate a willing borrower, assess their creditworthiness, and draft legal lending contracts—an impossibly inefficient hurdle. By aggregating capital and standardizing operations, financial institutions reduce transaction costs for consumers seeking to save, invest, or borrow money. For the comprehensive financial planner, these institutions represent the physical and legal architecture upon which every client’s financial plan is built. Understanding the specific function, regulatory environment, and protective limits of each institution is not merely academic; it is the blueprint for securely allocating a client's life savings.

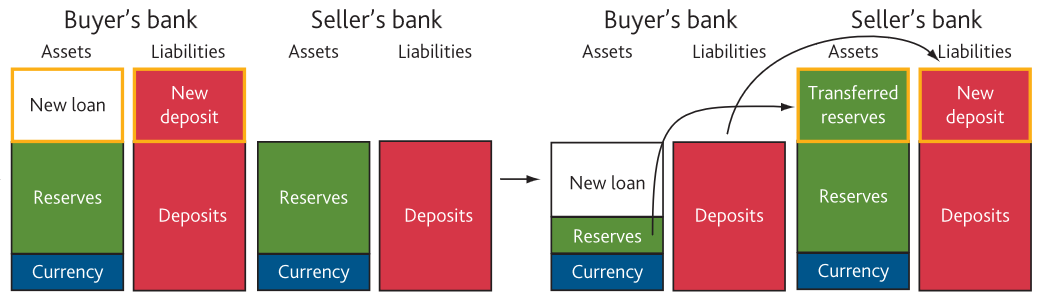

Depository institutions are the foundational layer of consumer finance. While consumers view them simply as safe places to store cash, their macroeconomic function is much more dynamic. Depository institutions create broad money in the economy through the fractional reserve lending process. When a deposit is made, the institution retains only a fraction of that cash in reserve, lending the remainder out to borrowers, who in turn deposit those funds back into the banking system to be lent out again.

Commercial Banks

Commercial banks are for-profit depository institutions owned by private shareholders. They perform a seemingly paradoxical feat of financial engineering: commercial banks facilitate economic liquidity by accepting short-term deposits to fund long-term loans. A client expects to be able to withdraw their checking account balance on demand (short-term liability for the bank), yet the bank uses that same money to fund 30-year mortgages and 5-year business loans (long-term assets).

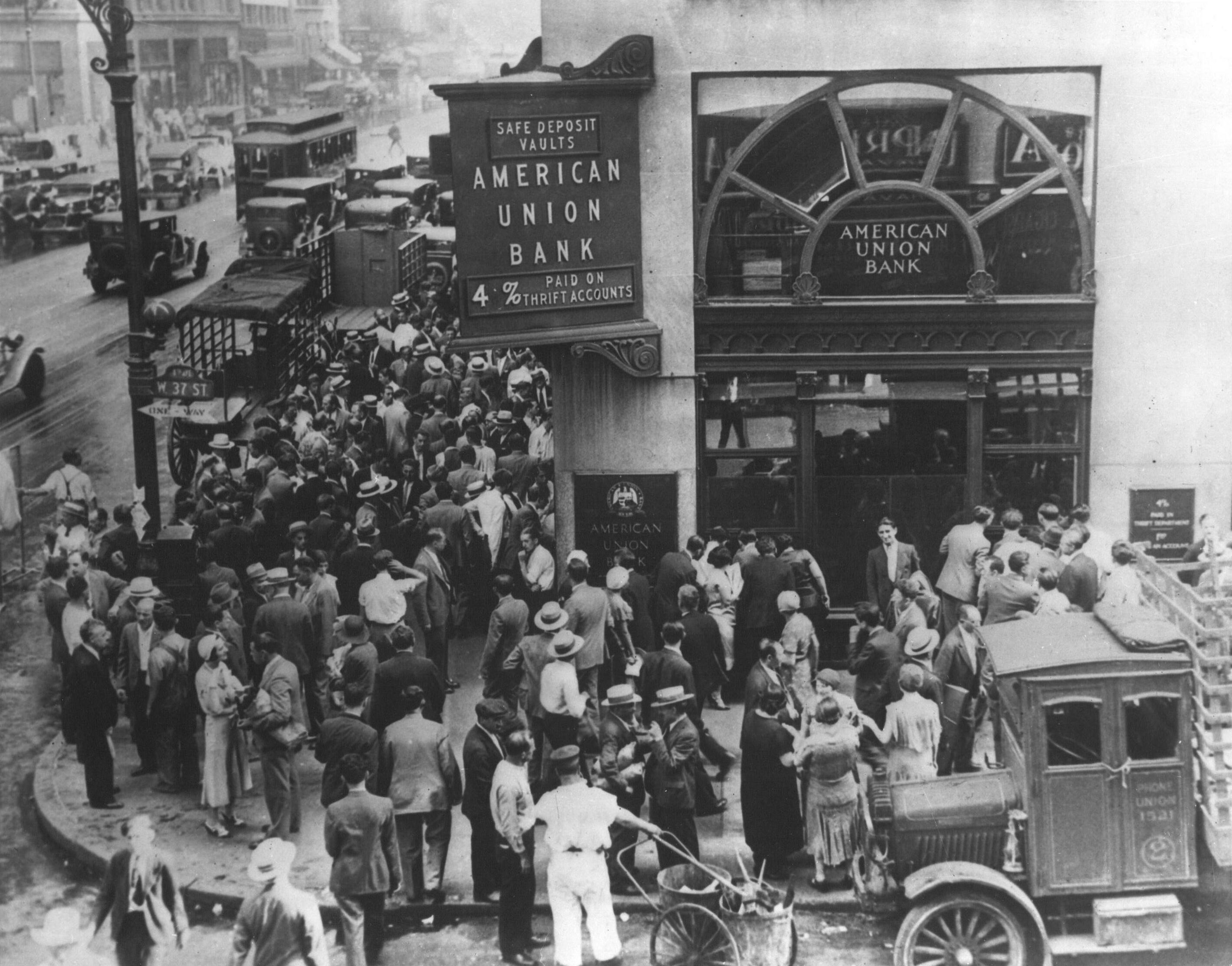

To prevent panic-driven bank runs resulting from this maturity mismatch, the federal government steps in. The Federal Deposit Insurance Corporation (FDIC) insures deposits at participating commercial banks up to $250,000 per depositor per ownership category. Because of this absolute principal protection and immediate accessibility, financial planners use commercial banks to house a client's emergency fund in highly liquid accounts.

Credit Unions and S&Ls

Not all depository institutions are designed to generate profits for outside shareholders. Credit unions are member-owned, not-for-profit financial cooperatives. Because they lack the mandate to maximize shareholder value, credit unions typically distribute surplus organizational income to members by offering higher deposit yields or lower borrowing costs.

However, the cooperative structure requires a defined community. Credit union membership is legally restricted to individuals sharing a common bond such as an employer or geographic community. Their deposits are protected by a distinct regulatory body: the National Credit Union Administration (NCUA) insures credit union deposits up to $250,000 per individual depositor.

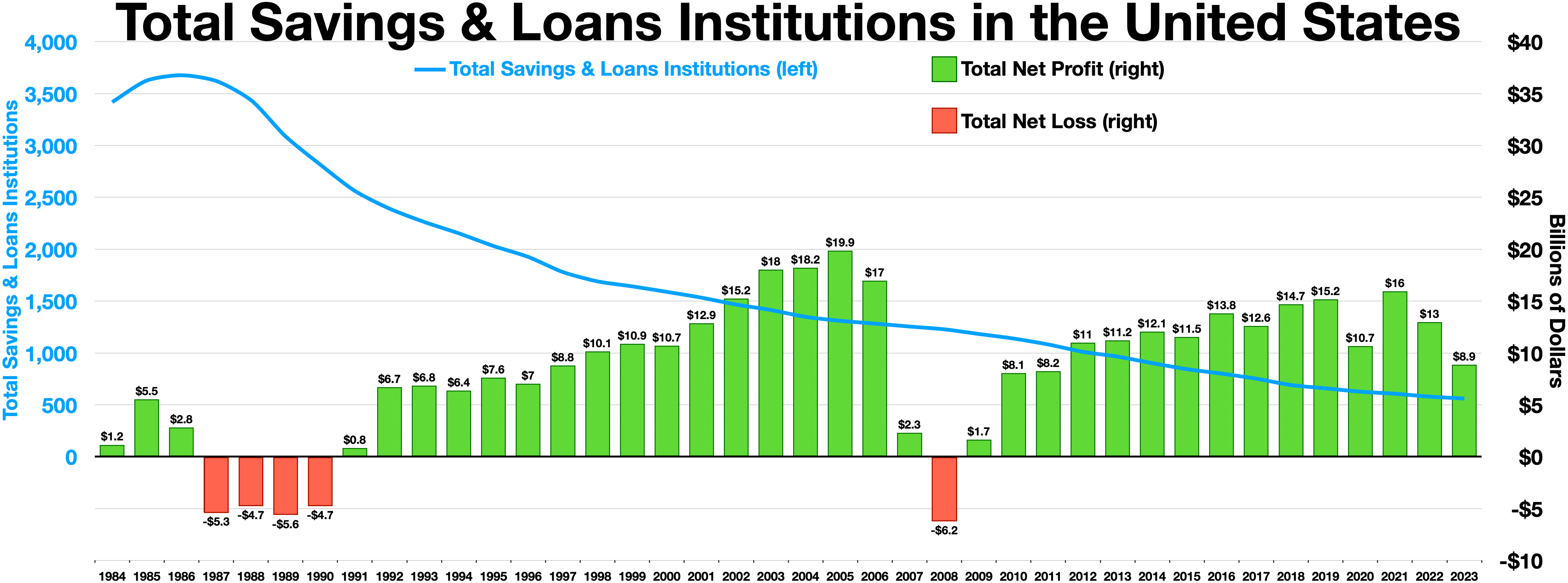

Historically parallel to banks and credit unions are Savings and Loan Associations (S&Ls). Savings and loan associations are depository institutions mandated to focus primarily on residential mortgages. Though their prevalence has waned since the 1980s, they remain a structural component of the mortgage financing ecosystem.

Comparison of Depository Protections

| Feature | Commercial Bank | Credit Union |

|---|---|---|

| Motive | For-profit | Not-for-profit, member-owned |

| Insurance Agency | FDIC | NCUA |

| Coverage Limit | $250,000 per depositor, per ownership category | $250,000 per individual depositor |

| Primary Beneficiary | Shareholders | Member-depositors |

If depositories are for storing liquidity, brokerages are for building wealth. While depositories take your cash and lend it out on their own balance sheet, brokerage firms act as market intermediaries to facilitate the purchase and sale of financial securities between third parties. Financial planners utilize brokerage firms to establish and manage client wealth accumulation portfolios, translating human capital into appreciating financial assets.

To understand execution, you must distinguish between the two hats a brokerage firm can wear:

- A broker acts as an agent executing trade orders on behalf of clients. Much like a real estate agent matching a buyer to a seller for a commission, the broker merely facilitates the exchange without ever owning the security.

- A dealer acts as a principal by trading securities directly from the inventory of the firm. Like a used car dealership, the firm buys securities with its own capital and sells them to clients for a markup.

Crucial Exam Distinction: Bank deposits are guaranteed against absolute loss of principal. Securities in a brokerage account fluctuate with market risk and are never protected against poor investment performance.

However, if the brokerage firm itself goes bankrupt or commits fraud, clients have a safety net. The Securities Investor Protection Corporation (SIPC) protects customers of failed brokerage firms up to $500,000 per customer. Within that half-million-dollar umbrella, the Securities Investor Protection Corporation protection limit includes a maximum of $250,000 for uninvested cash.

Constructing a properly diversified portfolio from individual stocks and bonds requires massive amounts of capital and specialized research—barriers that historically locked retail investors out of the market. Investment companies solve this scale problem. Investment companies are legal entities that pool money from investors to purchase a diversified portfolio of securities.

By aggregating the capital of thousands of individuals, investment companies provide retail investors with immediate portfolio diversification at a lower cost than purchasing individual securities, while simultaneously ensuring that investment companies provide retail investors with professional portfolio management.

The primary legislation governing this space is foundational to modern finance: The Investment Company Act of 1940 establishes the regulatory framework for investment companies in the United States, creating strict rules on leverage, transparency, and fiduciary duty. Under this act, the most ubiquitous tool in the financial planner's arsenal was defined: mutual funds are legally structured as open-end investment companies, meaning they continually issue and redeem shares directly with investors based on the fund's end-of-day net asset value.

While banks and brokerages handle the accumulation of wealth, a financial plan is incomplete without a mechanism to defend it from catastrophic loss. Financial planners integrate insurance company products into client plans to transfer catastrophic financial risks away from the client.

An individual cannot predict if their house will burn down this year, but a statistician can predict with high accuracy how many houses in a state will burn down. Capitalizing on the Law of Large Numbers, insurance companies pool premium payments from many individuals to pay for the financial losses of a few individuals.

This risk transfer falls into two primary categories for the financial planning client:

- Life insurance companies provide financial products designed to replace human capital upon premature death. This ensures that surviving dependents can maintain their standard of living, pay off mortgages, and fund future goals even if the primary earner's income halts.

- Property and casualty insurance companies protect client assets against physical damage and liability claims. This defends the client's balance sheet from being wiped out by a lawsuit, an automobile collision, or a natural disaster.

Unlike banks and investment companies which answer heavily to federal regulators (the Federal Reserve, SEC, FDIC), the insurance industry maintains a decentralized regulatory structure. Insurance companies are primarily regulated at the state level rather than the federal level, requiring financial planners to navigate state-specific nuances in asset protection, licensing, and insurance guarantees.

For high-net-worth clients, the mechanics of wealth transfer become as complex as wealth accumulation. Trust companies are legal entities authorized to act as fiduciaries, agents, or trustees on behalf of individuals or businesses.

Instead of relying on a family member who may lack financial acumen or impartiality, financial planners coordinate with trust companies to implement complex wealth transfer strategies for clients. These entities offer continuity and professional detachment that a human trustee cannot. In practice, trust companies administer estates, manage trusts, and provide custodial arrangements for assets, ensuring that a grantor's exact wishes are carried out across generations, insulated from family politics and emotional decision-making.

When sitting across from a client, you are the architect directing traffic across these institutions. You do not build the plumbing; you assemble it. You will leverage a Commercial Bank to secure their $30,000 emergency fund (guaranteed by the FDIC), utilize an Insurance Company to replace their $2,000,000 of future earnings potential, rely on a Brokerage Firm and Investment Companies to grow their retirement wealth via open-end mutual funds, and finally, engage a Trust Company to ensure those accumulated assets pass seamlessly to their heirs. Understanding the distinct borders, rules, and functions of these institutions is how a planner engineers a resilient, lifelong financial strategy.