Privacy, Fraud, and Federal Compliance

Insurance is fundamentally an information business. Long before a premium is collected or a death benefit is paid, an insurer must gather deeply personal data to quantify human risk. This extraction of data—ranging from financial histories to biological vulnerabilities—creates an immense asymmetry of power between the institution and the individual. To balance this scale, federal law wraps the insurance transaction in a strict framework of privacy protections, consumer rights, and national security mandates. For an insurance producer, mastering these federal compliance standards is not merely a secondary administrative task; it is the absolute prerequisite for participating in the modern financial system.

When a client applies for a life or health insurance policy, they are handing you the blueprints to their personal life. Because this information is so sensitive, two major federal laws govern exactly what you can do with it: the Gramm-Leach-Bliley Act (GLBA) for financial data, and the Health Insurance Portability and Accountability Act (HIPAA) for medical data.

The Gramm-Leach-Bliley Act (GLBA)

The Gramm-Leach-Bliley Act was designed to tear down the walls between banks, brokerages, and insurance companies, allowing them to consolidate. But with consolidation comes the risk of rampant data sharing. To protect the public, the GLBA requires insurance companies to disclose their information-sharing practices to consumers.

The law enforces transparency through two distinct mechanisms:

- Initial and Ongoing Notice: Insurance companies must provide a clear written privacy notice at the time a new customer relationship is established. But privacy policies change. Therefore, insurance companies must also provide existing customers with an updated privacy notice on an annual basis.

- The Power to Say No: If an insurer wants to monetize a client’s data, the client must have a veto. The Gramm-Leach-Bliley Act provides consumers with the right to opt out of having their personal financial information shared with non-affiliated third parties.

Health Insurance Portability and Accountability Act (HIPAA)

While GLBA protects a client's bank account details, HIPAA protects the privacy of individually identifiable health information.

Definition: Individually identifiable health information under the Health Insurance Portability and Accountability Act is called Protected Health Information (PHI). This includes everything from a blood test result to a record of a prescribed medication.

Because producers routinely handle PHI during the underwriting process, insurance producers must provide applicants with a Notice of Privacy Practices detailing exactly how their health information will be used.

Routine uses of PHI—like an underwriter reviewing medical records to issue a policy—are expected. However, if the data is going to be used for anything outside the core function of insurance processing, insurers must obtain written authorization from an applicant before disclosing Protected Health Information for non-routine purposes.

Insurers rely heavily on third-party reporting agencies to verify the claims made on an application. The Fair Credit Reporting Act (FCRA) regulates the collection and distribution of consumer credit information. It ensures that consumers are not secretly monitored or unfairly penalized by inaccurate data.

There are two primary types of reports underwriters request, and they carry very different compliance burdens.

| Feature | Standard Consumer Report | Investigative Consumer Report |

|---|---|---|

| Source of Data | Institutional databases and financial records. | Human beings (personal interviews). |

| What it Gathers | Contains information regarding a consumer's credit history and financial status. | Gathers information on a consumer's character and reputation through personal interviews with associates and friends. |

| Notice Requirement | General disclosure usually bundled in the standard application paperwork. | Highly regulated; requires specific, time-sensitive disclosures to the consumer. |

Because an investigative consumer report involves interviewing neighbors and coworkers—a highly invasive procedure—the FCRA enforces strict transparency rules:

- The 3-Day Rule: An insurer must notify an applicant in writing within three days of requesting an investigative consumer report.

- The Right to Know: Consumers have the right to request a complete written disclosure of the nature and scope of an investigative consumer report.

- The 5-Day Rule: Once that request is made, an insurer must provide the nature and scope of an investigative report within five days of receiving a formal consumer request.

Adverse Action and Criminal Penalties

What happens if a standard consumer report reveals terrible credit, and the insurer decides the applicant is too risky to insure? An insurer must provide the consumer with the name and address of the reporting agency if insurance coverage is denied based on a credit report. The insurer does not hand over the report itself; they simply point the consumer to the agency so the consumer can dispute any inaccuracies directly.

Because consumer data is so powerful, accessing it illicitly is treated as a severe offense. The Fair Credit Reporting Act imposes criminal penalties on individuals who obtain consumer credit information under false pretenses.

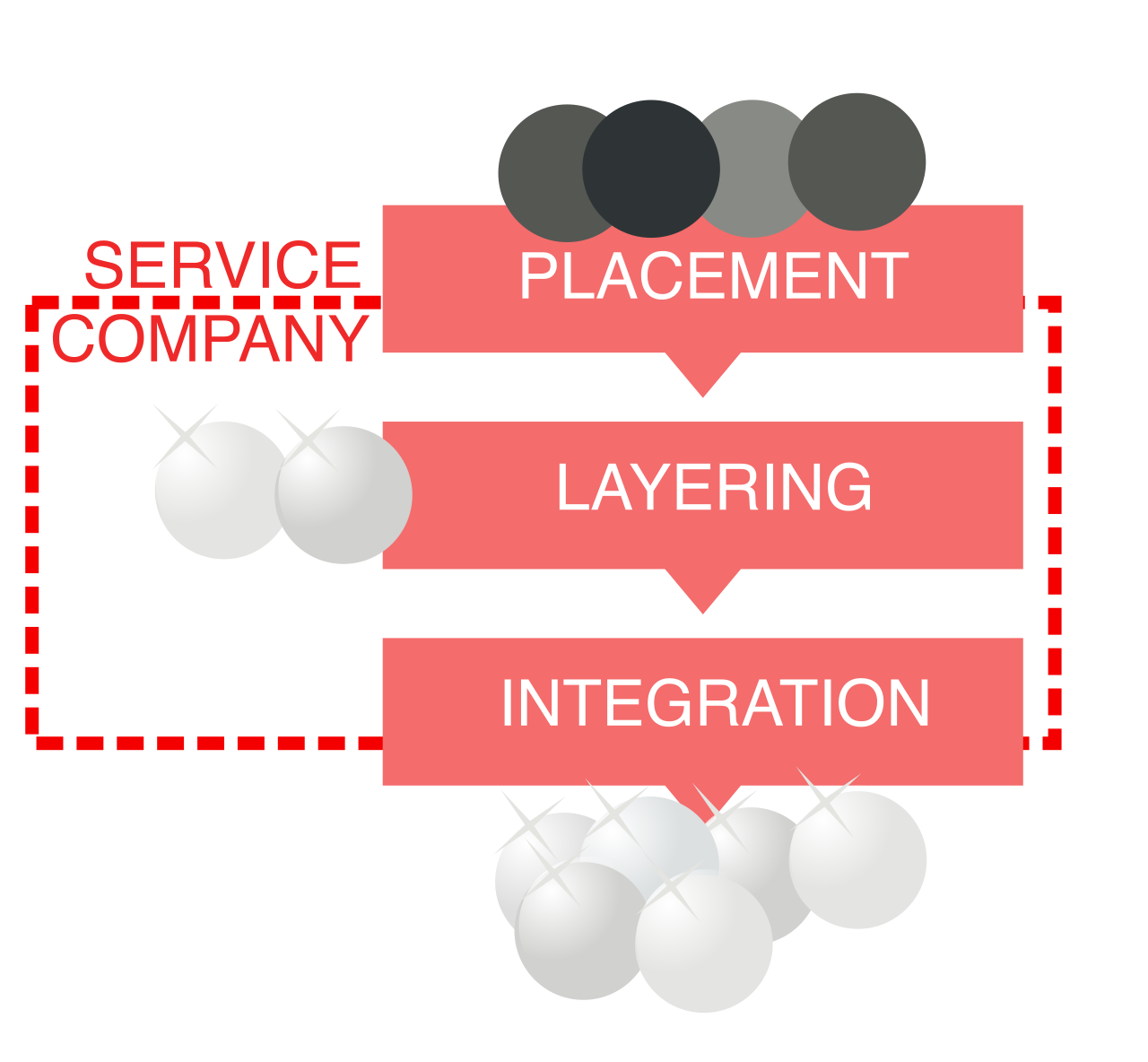

Imagine you are a criminal with $50,000 in illicit, untaxed street cash. You cannot deposit it into a bank without triggering an investigation. But if you take that physical cash, purchase an asset, and then liquidate that asset, the institution cuts you a perfectly clean, traceable corporate check. This is money laundering.

To combat this, the USA PATRIOT Act requires financial institutions to establish strict anti-money laundering (AML) programs. As a producer, you are the eyes and ears of this federal mandate.

The Vulnerability of Life Insurance

Not all insurance products are useful to money launderers. Term life insurance policies without cash value are generally exempt from the USA PATRIOT Act anti-money laundering regulations. Why? Because term life is pure protection; there is no liquid cash account to withdraw from, making it useless for laundering.

However, life insurance policies with cash value components are considered highly susceptible to money laundering activities. Criminals use these policies as temporary bank accounts to "wash" their funds.

Recognizing Red Flags Producers must remain vigilant for behaviors that defy logical financial planning. Two distinct red flags include:

- Paying life insurance premiums with large amounts of physical cash.

- Canceling a cash value life insurance policy shortly after issuance to receive the cash value (accepting the surrender penalties just to get a clean check).

If you witness this behavior, you do not confront the client. Instead, insurance companies must file a Suspicious Activity Report (SAR) for suspicious financial transactions involving funds of $5,000 or more.

To sell insurance, you must prospect. But federal law heavily restricts how and when you can pick up the telephone.

The National Do Not Call Registry prohibits telemarketers from calling registered phone numbers to solicit insurance sales. Because this list grows daily, insurance producers must update their telemarketing calling lists from the National Do Not Call Registry every 31 days.

The Established Business Relationship Exemption

The law is designed to stop cold-calling harassment, not to prevent businesses from servicing their existing clients. Insurance producers may call a consumer on the Do Not Call Registry if an established business relationship exists.

Federal law sets specific countdown clocks for these relationships:

- Post-Transaction: An established business relationship allows an insurance producer to call a consumer for up to 18 months after a purchase or transaction.

- Post-Inquiry: An insurance producer may call a consumer on the Do Not Call Registry for up to three months after a consumer makes an inquiry (e.g., requesting a quote).

Time of Day Restrictions

Even if a consumer is not on the Do Not Call list, you cannot call them at any hour. Federal telemarketing rules restrict solicitation calls to between the hours of 8:00 AM and 9:00 PM.

Critically, telemarketing time restrictions are strictly based on the local time zone of the consumer being called. If you are a producer in New York calling a prospect in Los Angeles at 9:00 AM Eastern, you are violating federal law, because it is 6:00 AM Pacific.

Because insurance is a business built entirely on trust and the faithful execution of financial promises, the industry aggressively polices who is allowed to participate.

Under 18 U.S.C. § 1033, federal law prohibits individuals convicted of a felony involving dishonesty from engaging in the insurance business without state authorization. "Dishonesty" includes crimes like fraud, embezzlement, or perjury.

A prior conviction does not mean a lifetime ban, but it removes the default right to become licensed. To legally work in the insurance industry, a prohibited person must obtain a written consent waiver from a state insurance commissioner. This clearance, officially restoring their eligibility to participate in the business of insurance, is commonly known as a 1033 waiver.