Policy Exclusions

The mathematical foundation of a life insurance pool rests on the law of large numbers and standard mortality tables. When you, as a producer, write a standard policy, you are underwriting a predictable, average human lifespan based on normal, everyday risks. However, certain environments, occupations, and intentional actions introduce variables so statistically volatile that they puncture this predictability and threaten the solvency of the entire risk pool. To manage this volatility, insurers deploy contractual boundaries to clearly delineate which extreme risks they cannot accept.

At its core, an exclusion is a provision in an insurance policy that eliminates coverage for specified hazards or eliminates coverage for specified causes of death.

Why do these exist? It is a matter of basic mathematical fairness. If an insurance company were forced to accept the mortality risk of deep-sea explorers and combat soldiers at standard rates, they would have to drastically raise prices for everyone. Insurers use policy exclusions to keep overall premium rates affordable for the average policyowner. Simultaneously, these provisions act as a structural shield to protect the insurance company from catastrophic financial losses that would arise from paying out mass claims during unpredictable events, like a prolonged military conflict.

The mechanics of an exclusion are absolute but equitable. If a life insurance policyholder dies from an excluded cause, the insurer legally denies the full death benefit. However, the insurer does not simply pocket the client's money and walk away. When an insurer denies a death claim due to a policy exclusion, the insurer typically refunds all paid premiums to the beneficiary.

By doing this, the insurer essentially says, "We could not cover this specific hazard, so we are returning the cost of the contract."

When a client defies standard earthly limitations, their mortality risk shifts. This brings us to three highly tested exclusions: aviation, hazardous occupations, and hazardous hobbies.

The Aviation Exclusion

When reviewing a client's application, you must distinguish between a person riding in an airplane and a person operating one.

The standard aviation exclusion does not apply to fare-paying passengers on commercial airlines. If your client is flying on a Delta or United flight to Chicago and the plane crashes, the death benefit is paid in full. Commercial aviation is statistically safer than driving a car.

However, the aviation exclusion eliminates life insurance coverage for deaths related to private flights and deaths related to non-commercial flights. The risk profile of a small Cessna is vastly different from a Boeing 777. Therefore, the standard aviation exclusion typically applies to student pilots and flight instructors, as well as amateur private pilots.

Hazardous Occupations and Hobbies

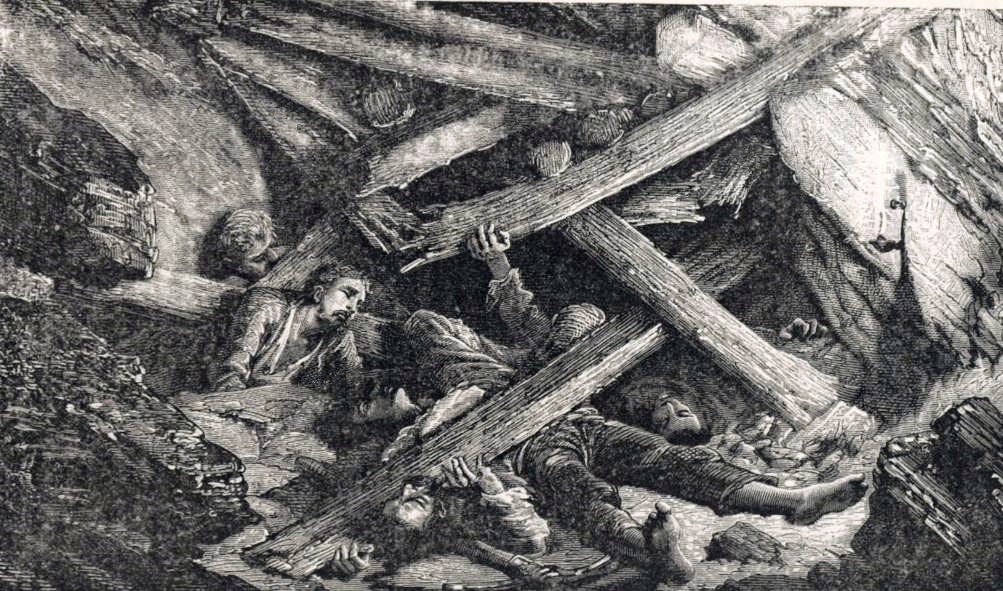

If a client spends forty hours a week in an environment where accidents are frequently fatal, standard underwriting cannot absorb that risk. The hazardous occupation exclusion eliminates life insurance coverage for deaths caused by specific dangerous jobs. A classic, testable example is underground mining, an industry inherently exposed to tunnel collapses and lethal gases.

Similarly, what a client does on their weekends matters. The hazardous hobbies exclusion eliminates life insurance coverage for deaths caused by dangerous recreational activities. Common triggers for this exclusion include skydiving and scuba diving.

The Producer's Workaround: What do you tell the client who loves scuba diving? You do not necessarily have to turn them away. A life insurance applicant with a hazardous hobby can sometimes obtain full coverage by paying a higher premium. This extra premium (often called a flat extra) mathematical compensates the insurer for the added statistical danger, allowing the policy to issue without the exclusion.

War introduces catastrophic, correlated risk—meaning many insured individuals could die at the same time, bankrupting an insurer. To prevent this, the war clause eliminates life insurance coverage for deaths related to military service or resulting from acts of war.

As a producer, you must understand that there are two distinct variations of the war clause. Knowing the difference is critical when advising military clients.

1. The Status Clause

The status clause is a specific type of war exclusion found in life insurance policies that is notoriously rigid. The status clause denies the life insurance death benefit if the insured dies while serving in the military, period. It is entirely based on the client's status as an active service member.

Crucially, the status clause denies the death benefit regardless of the actual cause of death during military service. If an active-duty soldier on leave dies of a sudden heart attack while sitting in their living room, a policy with a status clause will deny the death benefit, because their status at the time of death was military.

2. The Results Clause

In contrast, the results clause is a specific type of war exclusion that looks at the cause of death rather than the individual's uniform.

The results clause denies the life insurance death benefit only if the insured dies as a direct result of an act of war.

| Scenario | Status Clause | Results Clause |

|---|---|---|

| Soldier killed in combat | Denied (Status is military) | Denied (Result of an act of war) |

| Soldier killed in off-duty car accident | Denied (Status is military) | Covered (Not an act of war) |

As shown above, under a results clause, an active-duty soldier killed in an off-duty car accident retains full life insurance death benefit coverage.

Insurance contracts operate on the principle of fortuity—losses must be accidental or unpredictable. The insurer will not subsidize criminal behavior or immediate, intentional self-destruction.

The Illegal Acts Exclusion

If your client dies in the commission of a serious crime, the insurer is not liable. The illegal acts exclusion eliminates life insurance coverage if the insured dies while committing a felony. If an insured is fatally wounded by police while robbing a bank, the death benefit is denied.

The Suicide Clause

Perhaps the most profoundly important exclusion to understand is the suicide clause. The suicide clause excludes the life insurance death benefit if the insured intentionally takes their own life within a specified initial period.

Why a specific period? The insurer must protect against adverse selection—someone buying a massive policy with the immediate, premeditated intent to commit suicide and enrich their beneficiaries. However, insurance also recognizes that severe mental health crises occurring years into a contract are a tragic, but standard, mortality risk.

- The Time Limit: The standard suicide clause time limit is two years from the life insurance policy issue date.

- Within the First Two Years: If an insured commits suicide within the suicide exclusion period, the insurer refunds the exact amount of paid premiums to the beneficiary. No death benefit is paid, but the insurer does not keep the premium money.

- After Two Years: After the suicide clause time limit expires, the insurer must pay the full death benefit in the event of the insured's suicide.

Understanding these exclusions ensures you know exactly the promises you are—and are not—making to your clients. You are selling a contract governed by the mathematics of risk. Exclusions are simply the guardrails that keep that mathematics structurally sound.