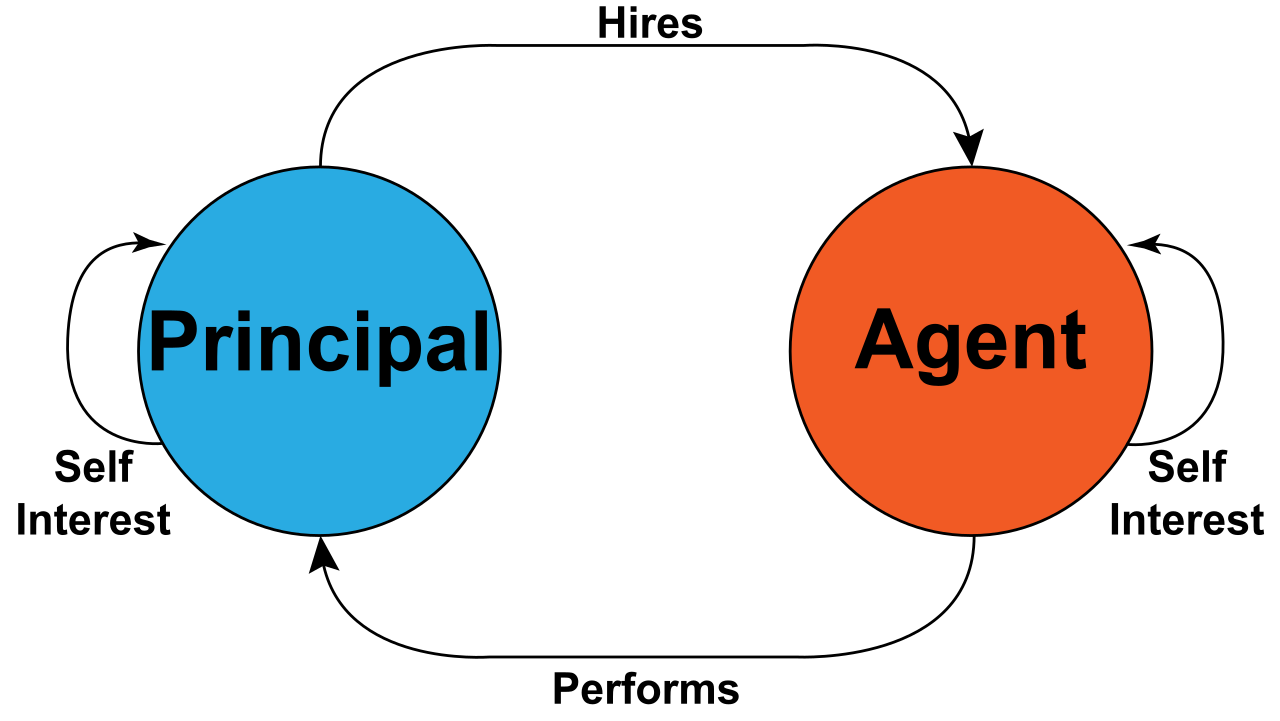

Corporate Governance and Compliance

A company is a legal person that can own property, borrow money, and be sued in its own name — but it cannot chair a meeting, sign a cheque, or decide anything. Every one of its acts is really the act of a human being who has been handed power over other people's capital, with none of the natural restraint that comes from spending your own money. Corporate governance is the machinery built to manage that gap: who gets to hold the power, what duties constrain them while they hold it, and what happens to the shareholders who never get a turn.

For SQE1, this topic is less about memorising section numbers in isolation and more about recognising the pattern behind them: every rule here exists to solve the same underlying problem of agency risk between directors, majority shareholders, and everyone else with money at stake.

The Companies Act 2006 (CA 2006) is the primary statute governing directors' duties, shareholder rights, and company decision-making in England and Wales, and almost every rule below traces back to it.

Company size dictates the minimum board. A private company must have at least one director (s.154), while a public company must have at least two. Historically, s.155 required only that at least one director be a natural person, leaving room for corporate directors to fill the rest of the board. That position is being phased out: s.156A — inserted by the Economic Crime and Corporate Transparency Act 2023 and brought into force from March 2024, with a transition period for existing corporate directors — now requires that each director be a natural person, subject to narrow exceptions in ss.156B–156C. Practically, treat s.156A as the current default rule for SQE1 purposes: corporate directors are being eliminated, not merely diluted. Whoever holds the role must also clear a low bar of formal capacity — s.157 fixes the minimum age for appointment as a director at 16.

Appointment itself is usually mundane: under the model articles, directors are appointed by an ordinary resolution of the shareholders, or the board can co-opt someone itself to fill a casual vacancy or add to its own numbers. That board-appointed director doesn't get a free pass, though — they typically hold office only until the next AGM, where they must stand for election by the shareholders like anyone else.

Removal works in the shareholders' favour by design. Under s.168 CA 2006, shareholders can remove a director before their term ends by ordinary resolution, and this can be done despite anything in the articles or any service agreement — a deliberately blunt override of private ordering. The procedural safeguard is special notice: at least 28 clear days under s.312. The director isn't silenced in the process — s.169 gives them the right to make written representations and to be heard at the meeting. And removal is not free of consequences for the company: s.168 expressly does not deprive the director of compensation or damages for loss of office, and a removed director may still have a separate claim for breach of their service contract or wrongful dismissal. Crucially, a s.168 removal resolution cannot be passed as a written resolution (s.288(2)) — the director's right to be heard requires an actual meeting.

There is one well-known escape hatch from all of this: a Bushell v Faith clause, a weighted-voting article that gives a director extra votes specifically on a resolution to remove them. Used correctly, it can make removal mathematically impossible — a legitimate, long-standing device for founder-directors who want security of tenure.

Shadow vs de facto directors. A shadow director (s.251) is someone in accordance with whose directions or instructions the actual directors are accustomed to act — influence without title. A de facto director is the reverse: someone who acts as a director without ever being validly appointed — title without formality. Both can attract director-level duties and liabilities despite never sitting through a proper appointment process.

Sections 171–177 CA 2006 codify seven duties that existed for centuries as fragmented common law and equitable rules. The codification did not freeze them in amber — the pre-existing case law remains relevant for interpreting what the statutory language means. All seven duties are owed by a director to the company, not to individual shareholders, which is why a shareholder generally cannot sue a director directly for a breach (that gap is exactly what derivative claims, covered later, exist to bridge).

| Section | Duty | Core idea |

|---|---|---|

| s.171 | Act within powers | Follow the constitution; only use powers for their proper purpose |

| s.172 | Promote the success of the company | Act in good faith for members' benefit as a whole, having regard to listed factors |

| s.173 | Exercise independent judgement | Don't fetter your own discretion (subject to valid prior agreements) |

| s.174 | Reasonable care, skill and diligence | Objective/subjective blended standard |

| s.175 | Avoid conflicts of interest | Situational conflicts — property, information, opportunity |

| s.176 | Not accept benefits from third parties | Bribes, kickbacks, inducements |

| s.177 | Declare interest in a proposed transaction | Disclosure before the company contracts |

s.171 requires a director to act in accordance with the company's constitution and to exercise powers only for the purposes for which they were conferred — a director can technically follow the rulebook and still breach this duty if they use a power for an improper collateral purpose (issuing shares to dilute a takeover bidder, for instance, rather than to raise capital).

s.172 is the duty most students initially misread as "maximise shareholder value" — it is broader than that. The director must act in the way they consider, in good faith, most likely to promote the company's success for the benefit of the members as a whole, and s.172(1) lists factors they must have regard to along the way: the likely long-term consequences of a decision, the interests of employees, the need to foster relationships with suppliers and customers, the impact on the community and environment, the desirability of maintaining a reputation for high standards of business conduct, and the need to act fairly between members. None of these factors override the director's own good-faith judgement about what serves the company — they inform it.

The most important qualification to s.172 sits at the edge of insolvency. Where a company is insolvent or bordering on insolvency, the duty to promote the company's success requires directors to have regard to the interests of creditors. The Supreme Court settled the trigger point for this in BTI 2014 LLC v Sequana SA [2022] UKSC 25: the creditor duty is engaged when directors know or ought to know the company is insolvent or bordering on insolvency, or that insolvent liquidation or administration is probable — not merely foreseeable as a distant risk. Sequana confirmed this "creditor duty" is not a freestanding obligation but an inflection of s.172 itself, and that its weight increases as the company's financial position deteriorates.

s.173 (independent judgement) has a built-in safety valve: a director does not breach it merely by acting in accordance with an agreement the company has validly entered into that restricts future discretion — a joint-venture agreement that binds a nominee director's vote, for example.

s.174 sets a dual-limbed standard of care: a subjective element (judged against the knowledge, skill, and experience the director actually has) and an objective element (judged against what is reasonably expected of someone carrying out that director's functions). The applicable standard is whichever of the two is higher — so a finance director with genuine accountancy expertise cannot claim a general-competence floor; they're held to their own superior standard.

s.175 is the broadest of the seven: it catches exploitation of any property, information, or opportunity, whether or not the company could actually have taken advantage of it itself — you can't defend a diverted opportunity by arguing the company was never in a position to pursue it. A conflict under s.175 can be authorised in advance by the independent directors on the board, but only if the company's constitution actually permits board-level authorisation — private companies get this by default under the model articles' framework; not every company does. Notably, s.175 has a carve-out: it does not apply to a conflict arising from a transaction or arrangement with the company itself — that scenario is hived off to ss.177 and 182 instead.

s.176 targets third-party benefits — a director must not accept a benefit conferred by reason of being a director or by reason of doing (or not doing) anything as a director. This is the bribery/kickback duty.

ss.177 and 182 form a pair covering self-dealing, split by timing. Under s.177, a director must declare the nature and extent of any interest in a proposed transaction or arrangement with the company before the company enters into it. s.182 covers the mirror case — declaring an interest in a transaction the company has already entered into. The consequences diverge sharply: failing to declare under s.182 is a criminal offence, whereas failing to declare under s.177 is not.

Breach of any general duty is not necessarily fatal — s.239 allows shareholders to ratify a breach by ordinary resolution, but with a built-in fairness filter: the votes of the director in question, and of any connected person who happens to be a member, must be disregarded when counting.

Beyond the general duties, CA 2006 layers specific approval requirements onto transactions where a director's personal interest is structurally obvious:

| Transaction | Section | Approval threshold |

|---|---|---|

| Substantial property transaction | s.190 (definition in s.191) | Ordinary resolution, if non-cash asset value exceeds £100,000, or exceeds 10% of net asset value and is more than £5,000 |

| Loan to a director | s.197 | Ordinary resolution (generally) |

| Director's service contract >2 years guaranteed term | s.188 | Ordinary resolution |

| Payment to a director for loss of office | s.217 | Ordinary resolution |

The substantial property transaction rules are the ones examiners lean on most, because the threshold is a genuine two-limbed test (either limb triggers approval), and s.191 measures the asset's value at the time the arrangement is entered into against the company's most recent statutory accounts.

Two Insolvency Act 1986 offences sit downstream of the general duties and become live once a company is genuinely in trouble.

Wrongful trading (s.214 IA 1986): a director may be personally liable if they continued trading after they knew, or ought to have concluded, there was no reasonable prospect of avoiding insolvent liquidation. The statutory defence is that the director took every step to minimise potential loss to creditors — this is a demanding standard; simply stopping trading isn't automatically enough if better mitigating steps were available.

Fraudulent trading (s.213 IA 1986) is the more serious sibling: liability requires the business to have been carried on with intent to defraud creditors, which means proof of actual dishonesty — a much higher bar than wrongful trading's constructive-knowledge test.

Sitting above both is the Company Directors Disqualification Act 1986, which allows a court to disqualify a person from acting as a director for between 2 and 15 years. The disqualification bites hard: acting as a director while disqualified is itself a criminal offence, independent of whatever conduct led to the disqualification in the first place.

A company's articles of association set out the internal rulebook for board and shareholder decision-making — but that rulebook has limited power to protect the company from its own board's overreach when dealing with outsiders. Under s.40 CA 2006, the board's power to bind the company is deemed free of any limitation in the constitution, in favour of a person dealing with the company in good faith — a third party generally doesn't need to check the articles before relying on the board's authority. Separately, s.39 provides that the validity of an act done by the company cannot be questioned merely because the constitution lacked the capacity to authorise it — the old ultra vires doctrine has been almost entirely defanged for third parties.

Board decisions. Directors generally act collectively as a board, not individually, unless authority has been delegated. Under the model articles for a private company limited by shares, decisions can be taken at a board meeting or as a unanimous written resolution. A board meeting is quorate with at least two directors present (unless the articles set a different number), and decisions are generally taken by simple majority, with the chair holding a casting vote on a tie. A director with an interest in a resolution must not vote on it, or be counted in the quorum for it, subject to the exceptions the model articles carve out.

Shareholder resolutions. An ordinary resolution requires a simple majority — more than 50% of votes cast (s.282). A special resolution requires at least 75% of votes cast (s.283) and must expressly state that it is being proposed as a special resolution. Both types can generally be passed either at a general meeting or as a written resolution, except where the Act specifically mandates a meeting (removal of a director under s.168 being the standout example). Only private companies can use written resolutions (s.281) — public companies are locked out of that shortcut entirely. A written resolution is passed once the required majority of eligible members has signified agreement, and it lapses after 28 days from circulation unless the articles specify otherwise (s.297).

Meetings. A private company's general meeting needs at least 14 clear days' notice (s.307); a public company's AGM needs at least 21 clear days', unless a shorter period is agreed. Short notice is always possible if the requisite majority of members entitled to attend and vote consent. Only public companies are actually required to hold an AGM at all (s.336) — private companies can skip the ritual entirely. The default quorum for a general meeting, under the model articles and s.318, is two members present, unless the company genuinely has only one member.

Shareholders aren't purely passive between meetings, either: those holding at least 5% of paid-up voting capital can require the directors to call a general meeting (s.303). If the directors fail to call it within 21 days of a valid requisition, the requisitionists can call the meeting themselves.

Majority rule is the default, but CA 2006 gives minority shareholders several distinct routes to relief when the majority's control becomes abusive rather than merely unwelcome.

Unfair prejudice petitions (s.994). A minority shareholder can petition the court where the company's affairs have been conducted in a manner unfairly prejudicial to some or all members' interests. The court's remedial powers under s.996 are deliberately wide — any order it thinks fit — and the most common outcome is a share purchase order: the majority buys out the petitioner's shares at a fair value, letting them exit rather than forcing them to keep fighting from inside a company they no longer trust.

Derivative claims (s.260). Where the wrong is really done to the company — a director's negligence, default, breach of duty, or breach of trust — an individual member can bring a claim on the company's behalf. This requires the court's permission to continue under s.261, a deliberate gatekeeping step to filter out claims the company itself wouldn't rationally pursue. Any damages recovered belong to the company, not to the member who brought the claim — the member is a procedural vehicle, not the beneficiary.

Just and equitable winding up (s.122(1)(g) Insolvency Act 1986). This is the nuclear option: a minority shareholder can petition to have the company wound up entirely. It's treated as a remedy of last resort, most commonly deployed where trust and confidence between "quasi-partners" in a small, closely held company has broken down irretrievably — think of two 50/50 co-founders who can no longer work together and have no functioning board to resolve the deadlock.

Contractual protection. Statutory remedies aside, a shareholders' agreement can layer additional protection on top of the articles — reserved matters requiring unanimous consent being the classic mechanism, giving a minority a genuine veto over specified major decisions regardless of what the ordinary/special resolution thresholds would otherwise allow.

Class rights. Where shares are divided into classes with different rights, those rights can only be varied following the procedure in s.630 — typically requiring consent from holders of at least 75% of that class. A majority of the whole company cannot simply outvote a minority class into losing its special rights.

Good governance leaves a paper trail, and CA 2006 makes several parts of that trail compulsory. Companies must keep statutory registers — including a register of members and a register of directors — under Part 8. Since the Small Business, Enterprise and Employment Act 2015 amendments, companies must also maintain a PSC register (people with significant control), capturing anyone who generally holds more than 25% of the company's shares or voting rights (among other control tests) — a transparency measure aimed squarely at unmasking who really stands behind the company. Board minutes and general meeting minutes serve a related evidential function: they're the record that due process was actually followed when a decision was taken, which matters enormously if that decision is later challenged.

Finally, one equitable principle deserves to sit alongside all this formal machinery precisely because it dispenses with it: the Duomatic principle. Where shareholders together hold all the voting shares, they can informally agree to a course of action without following the statutory procedures for a resolution at all. It is the doctrine's job to recognise that unanimous, informed consent is substantively the same thing as a resolution — just without the paperwork — and for SQE1 purposes it is the clean answer to any scenario where a small, all-agreeing shareholder base seems to have skipped a formal step.