Plan and Manage Finance: Tracking

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

A commercial aircraft does not carry an infinite supply of fuel. Before takeoff, the flight crew maps a precise burn trajectory, anticipating headwinds, altitude changes, and mandatory safety reserves. Once in the air, the instruments do not merely report how much fuel has been consumed; they constantly calculate whether the remaining fuel is sufficient to reach the destination given the current velocity and weather.

Project finance operates on the exact same physical principles. A project budget is not a static pool of money; it is kinetic energy meant to be converted into business value. As project managers, you are in the cockpit. If you wait until the end of the project to check the ledger, you will crash. You must continuously measure the rate of expenditure against the rate of value creation, anticipate structural deficits, and manipulate the levers of schedule and scope to land the project safely.

To track money effectively, you must first establish the rhythm and rules of observation. You cannot measure financial performance chaotically; it requires a structured mechanism.

In traditional and hybrid environments, the project cost management plan defines the format and frequency of project financial reports. It tells you how and when you will measure the money. Because organizations do not operate in a vacuum, project financial reporting periods typically align with the executing organization's fiscal calendar and accounting cycles. If your corporate finance department closes the books on the last Friday of the month, your project financial reporting must synchronize with that heartbeat.

Generating the report is only half the physics; delivering the information is the other. The communications management plan specifies which project stakeholders receive financial performance reports. The CFO requires a different level of financial granularity than the lead engineer.

Agile environments approach reporting through a different lens, prioritizing absolute transparency over periodic distribution. Agile projects use information radiators to provide stakeholders with real-time visibility into financial burn rates. Instead of waiting for an end-of-month PDF, an Agile stakeholder can walk into a team room—or open a shared dashboard—and instantly see how fast capital is being converted into working software.

Before you can control costs, you must understand how a budget is constructed. It is not a single lump sum. It is built in layers, designed to absorb specific types of impact.

- Activity Budgets: The estimated cost of the actual work.

- Contingency Reserves: Funds allocated for identified risks (the "known unknowns").

A project cost baseline includes authorized activity budgets and contingency reserves. This baseline is the standard against which you measure all project performance.

However, there is a third layer of money kept completely separate from your performance measurement: Management reserves are designated exclusively to cover unforeseen project risks (the "unknown unknowns"). Because these risks were never planned for, a project cost baseline strictly excludes management reserves. You do not measure your daily performance against money you were never supposed to spend.

If an unforeseen disaster strikes, you cannot simply reach into the management reserve. Utilizing management reserves requires formal governance approval to move funds into the active cost baseline. Only then can you spend it. Ultimately, the total financial authority you possess—the total project budget—is the sum of the cost baseline and the management reserves.

Financial management is fundamentally predictive. You are looking for icebergs before they hit the hull.

One of the most common ways projects fail is not by exceeding the total budget, but by running out of cash in a specific month. Cash flow analysis compares planned expenditures against funding availability to anticipate future cash deficits. Imagine you have a $1,200,000 budget for a year. That does not mean you have $1,000,000 available on day one. If you plan to buy $400,000 worth of server hardware in February, but corporate finance only releases $100,000 a month, you have a structural cash flow deficit.

How do we solve this? Through funding limit reconciliation, which adjusts the project schedule to prevent expenditures from exceeding authorized periodic funds. If you only have $100,000 in February, you must delay the procurement of the servers—pushing the schedule outward—to smooth the expenditure curve so it fits underneath the funding ceiling.

In Agile, forecasting challenges takes a different form. Burn rate measures the speed at which an Agile project team consumes the authorized project budget. If a team costs $50,000 per iteration, that is their burn rate. To protect the organization's investment, Agile teams mitigate financial risk by delivering the highest-value product features in early iterations. If funding is abruptly cut halfway through the year, the business has already captured the most critical return on investment.

In predictive and hybrid projects, tracking simply how much money you spent is useless. If I tell you I spent $50,000, is that good or bad? You don't know, because I haven't told you what I built for that money.

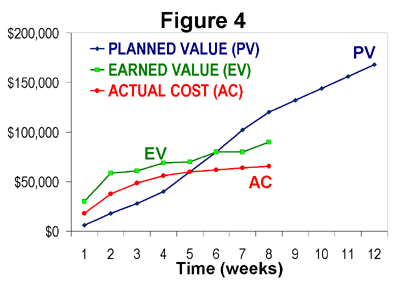

This brings us to Earned Value Analysis (EVA), which compares the performance measurement baseline to actual project schedule and cost performance. EVA translates project progress into a common financial language.

Cost Tracking Metrics

To understand cost performance, we look at Cost Variance (CV) and the Cost Performance Index (CPI).

- Cost Variance represents the mathematical difference between a project's Earned Value and its Actual Cost (CV=EV−AC). It tells you in absolute dollars how far off the mark you are.

- If your CV is negative, your Actual Costs are higher than the value of the work you actually achieved. Therefore, a negative Cost Variance indicates the project is currently over budget.

- The Cost Performance Index measures the cost efficiency of budgeted resources (CPI=EV/AC). It tells you how much value you are getting for every dollar spent.

- A Cost Performance Index below 1.0 indicates a cost overrun for work completed. (A CPI of 0.8 means you are only getting 80 cents of value out of every dollar you spend).

Schedule Tracking Metrics (Using Money)

Fascinatingly, Earned Value allows us to measure time using money.

- Schedule Variance calculates the mathematical difference between Earned Value and Planned Value (SV=EV−PV).

- By converting physical progress into dollars, Schedule Variance provides financial insight into whether the project is ahead of or behind the planned delivery dates.

Agile Earned Value

You might think Agile rejects EVA. It doesn't; it simply changes the units of measurement. Because Agile fixes time and cost (a stable team working in fixed sprints), Agile earned value management uses story points and iteration velocity to track financial performance. The "Planned Value" is the planned velocity, the "Earned Value" is the completed story points, and the financial health is derived from how many iterations are required to burn through the backlog.

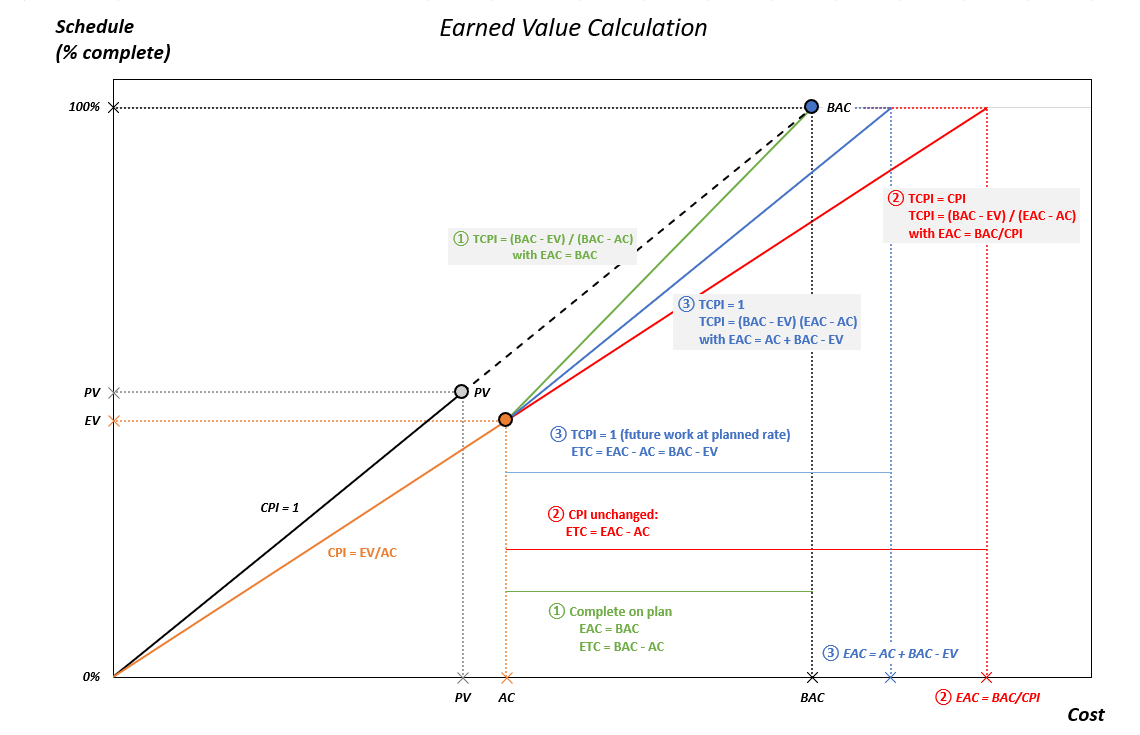

Now that we know exactly where we are, we must look at the instruments and predict where we will end up. Control Costs is the specific project management process of monitoring project status to update and manage project costs. It involves calculating four distinct futures:

| Metric | Definition in Plain English | Formal Concept |

|---|---|---|

| EAC (Estimate at Completion) | "Given what has happened so far, what will the entire project cost by the time we are done?" | Estimate at Completion calculates the forecasted total cost of a project upon completion. |

| ETC (Estimate to Complete) | "How much more money do I need from today onward to finish?" | Estimate to Complete predicts the expected cost to finish all remaining project work. |

| VAC (Variance at Completion) | "When we finish, how far over or under the original budget will we be?" | Variance at Completion projects the expected amount of budget deficit or surplus at the end of the project. |

| TCPI (To-Complete Performance Index) | "How hard do we have to work for the rest of the project to meet our financial goals?" | To-Complete Performance Index calculates the cost efficiency required on remaining work to meet a specified financial goal. |

The TCPI Warning Light

TCPI is your engine temperature gauge. If your TCPI is 1.2, it means you must extract $1.20 of value out of every remaining $1.00 in the budget. A To-Complete Performance Index greater than 1.0 indicates the project team must work more efficiently to meet the budget. If the TCPI becomes mathematically impossible (e.g., 2.5), you cannot simply tell the team to "work harder."

When reality violently departs from the plan, your original estimates are useless. In these cases, a new bottom-up Estimate at Completion is required when original estimating assumptions are proven completely invalid. You must stop, re-evaluate every remaining task, and build a brand new ETC from scratch.

Project managers are empowered to manage minor turbulence. But what happens when the financial deviation is severe?

Every organization sets boundaries, known as tolerance thresholds, which define the acceptable range of cost variance before requiring formal escalation to senior management. If your tolerance is +/- 5%, and your CPI drops to 0.98, you document it and adjust your management tactics. But if your CPI plummets to 0.85, you have breached the threshold.

When a threshold is breached, you lose the authority to handle it locally. Managing severe financial variations requires submitting a formal change request to adjust the cost baseline. You cannot arbitrarily add money or remove scope to fix your numbers.

This request goes to the Change Control Board (CCB). The CCB doesn't just look at the money; they look at the physics of the project triangle. The Change Control Board evaluates the impact of financial variations on project scope before approving budget changes. If they grant you more money, they are altering the cost baseline. If they refuse to grant you money, they must authorize a reduction in project scope.

By mastering these mechanics—planning the reporting cycles, separating baselines from reserves, reading the Earned Value instruments, and respecting governance thresholds—you cease to be a passive observer of expenditures. You become an active pilot of project finance, capable of landing the project safely regardless of the economic weather.