Encumbrances and Liens

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

When a buyer purchases a piece of real estate, they naturally assume they are acquiring absolute, uncompromised dominion over the land and the physical structures sitting upon it. In legal reality, ownership is rarely so isolated. Almost every parcel of real property carries invisible attachments—legal rights, financial claims, or usage liabilities held by third parties. These attachments can dramatically alter the asset's underlying economics or limit what the owner can actually do with the dirt they just bought. Understanding exactly who holds these invisible strings, how they are mathematically prioritized, and what power they wield is the fundamental basis of real estate finance and title transfer.

To navigate a property transaction safely, you must first understand the broad category of forces that act upon a property's title.

An encumbrance is any claim, charge, or liability attached to real property.

Encumbrances generally fall into two categories: physical and financial. A physical encumbrance—like an easement or a zoning law—may restrict the physical use of a piece of real property. You might own the land, but an encumbrance might legally prevent you from building a fence over a utility line or operating a business from the living room.

A financial encumbrance, on the other hand, may lessen the financial value of a piece of real property. Crucially, an encumbrance does not necessarily prevent the transfer of real property title. A property can be bought and sold with encumbrances completely intact. The claim simply "runs with the land," meaning the new buyer inherits the encumbrance along with the deed. For a real estate salesperson, discovering these encumbrances early is the difference between a smooth closing and a derailed transaction.

While "encumbrance" is the umbrella term, real estate professionals spend the vast majority of their time dealing with one highly specific variant: the lien.

A lien is a specific type of financial encumbrance. It provides security for a debt or obligation of the property owner. Think of a lien as a legal anchor dropped onto a property's title. If the property owner honors their financial obligation, the anchor is lifted. If they do not, the lienholder holds a profound legal weapon: a lienholder can force the legal sale of a property to satisfy a debt if the property owner defaults.

Understanding how liens are created and enforced dictates how you advise a client whose title search returns unexpected legal complications.

The Genesis of a Lien: Voluntary vs. Involuntary

Liens do not simply appear; they are generated through distinct legal mechanisms. We classify them by how they originate—specifically, whether the property owner agreed to them.

| Origin Type | Definition | Common Example |

|---|---|---|

| Voluntary Lien | A voluntary lien is created intentionally by the actions of the property owner. | A real estate mortgage is an example of a voluntary lien. The buyer explicitly offers the home as collateral to secure the $500,000 bank loan. |

| Involuntary Lien | An involuntary lien is created by law without the property owner's consent. | Tax liens or judgments. The owner did not ask for this debt to be attached to their property, but the legal system imposed it. |

Involuntary liens are further subdivided by the engine of law that created them:

-

A statutory lien is an involuntary lien created by state or federal legislation. The law writes the rule, and the lien applies automatically when conditions are met (like unpaid property taxes).

A public notice of delinquent property taxes. When an owner fails to pay municipal taxes, a statutory lien is automatically attached to the specific property without the owner's consent. Source: Delinquent property tax lien list by Raquel Baranow, CC BY-SA 4.0. -

An equitable lien is an involuntary lien created by a court order based on common law principles. This typically arises when a court deems it fundamentally fair to impose a lien to prevent unjust enrichment.

Beyond how a lien is created, you must understand what the lien is allowed to touch. If your client owes money, does the creditor get to go after their house, their bank accounts, or their investment properties?

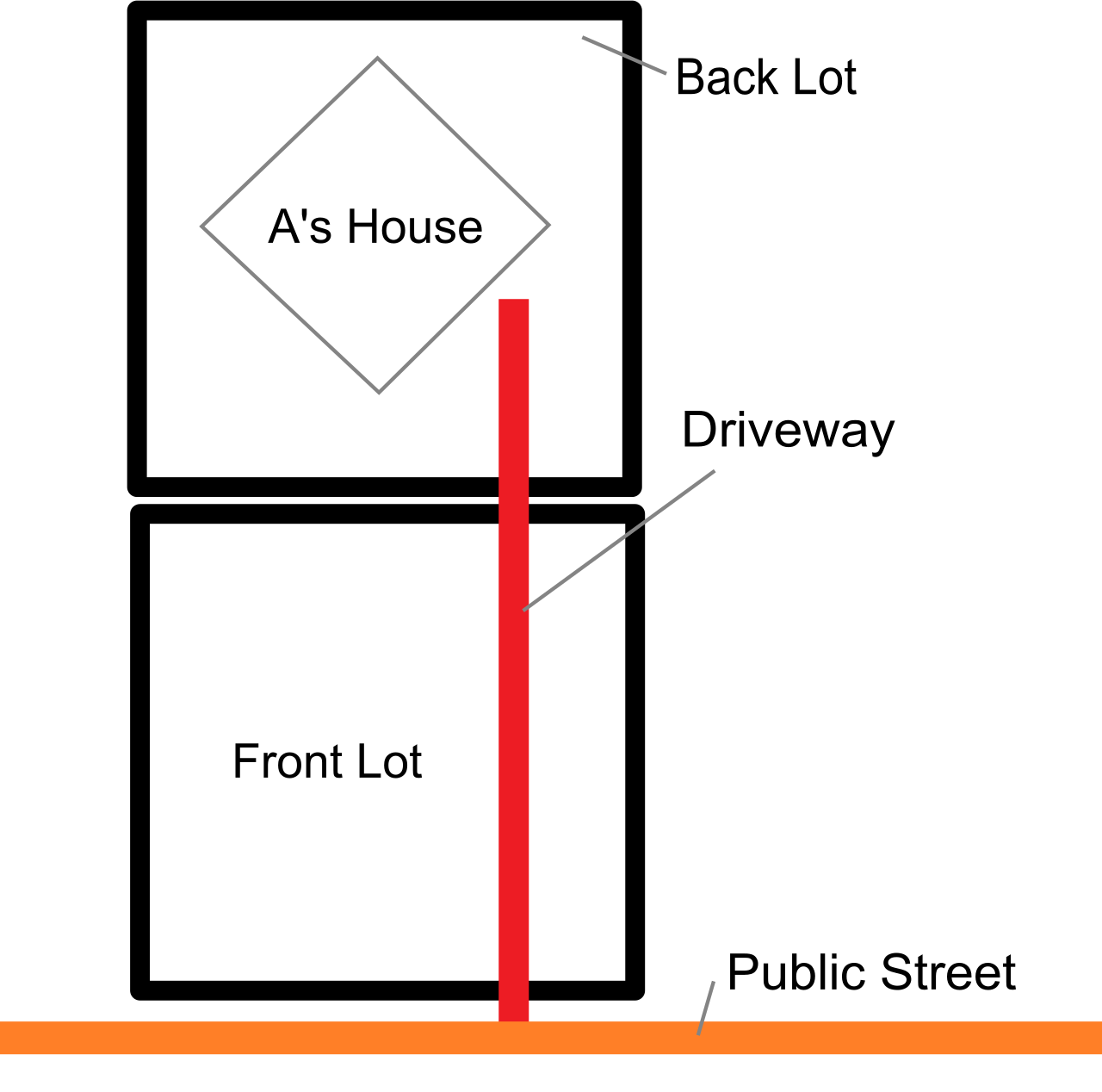

Specific Liens

A specific lien attaches only to one particular piece of real estate. The debt is married strictly to that exact parcel of land, ignoring the owner's other assets.

- A property tax lien is an example of a specific lien. If an owner fails to pay the property taxes on their Manhattan condo, the city places a lien only on that condo, not on their house in the Hamptons.

- A mechanic's lien is an example of a specific lien.

The Mechanic's Lien in New York A mechanic's lien secures payment for labor or materials used to improve real property. Because the contractor is not asked by the owner to place this lien, a mechanic's lien is classified as an involuntary lien. It exists to protect the carpenters, plumbers, and architects who pour their labor and materials into an asset but are left holding an unpaid invoice.

New York State enforces strict statutory clocks for these filings, and as a real estate professional, you must be acutely aware of these timelines when dealing with renovated properties:

- In New York, a mechanic's lien on a single-family dwelling must be filed within four months of the completion of work.

- In New York, a mechanic's lien on a commercial property must be filed within eight months of the completion of work.

If you are listing a recently flipped residential property, ensuring the contractor was paid—and the four-month window has cleared—protects your buyer from inheriting the flipper's unpaid bills.

General Liens

Conversely, a general lien attaches to all of a debtor's real and personal property. It casts a wide net. However, geography matters: a general lien affects debtor property located in the county where the lien is officially recorded. If a creditor wants to encumber properties in multiple counties, they must record the lien in each respective county clerk's office.

There are four major general liens you will encounter in real estate practice:

-

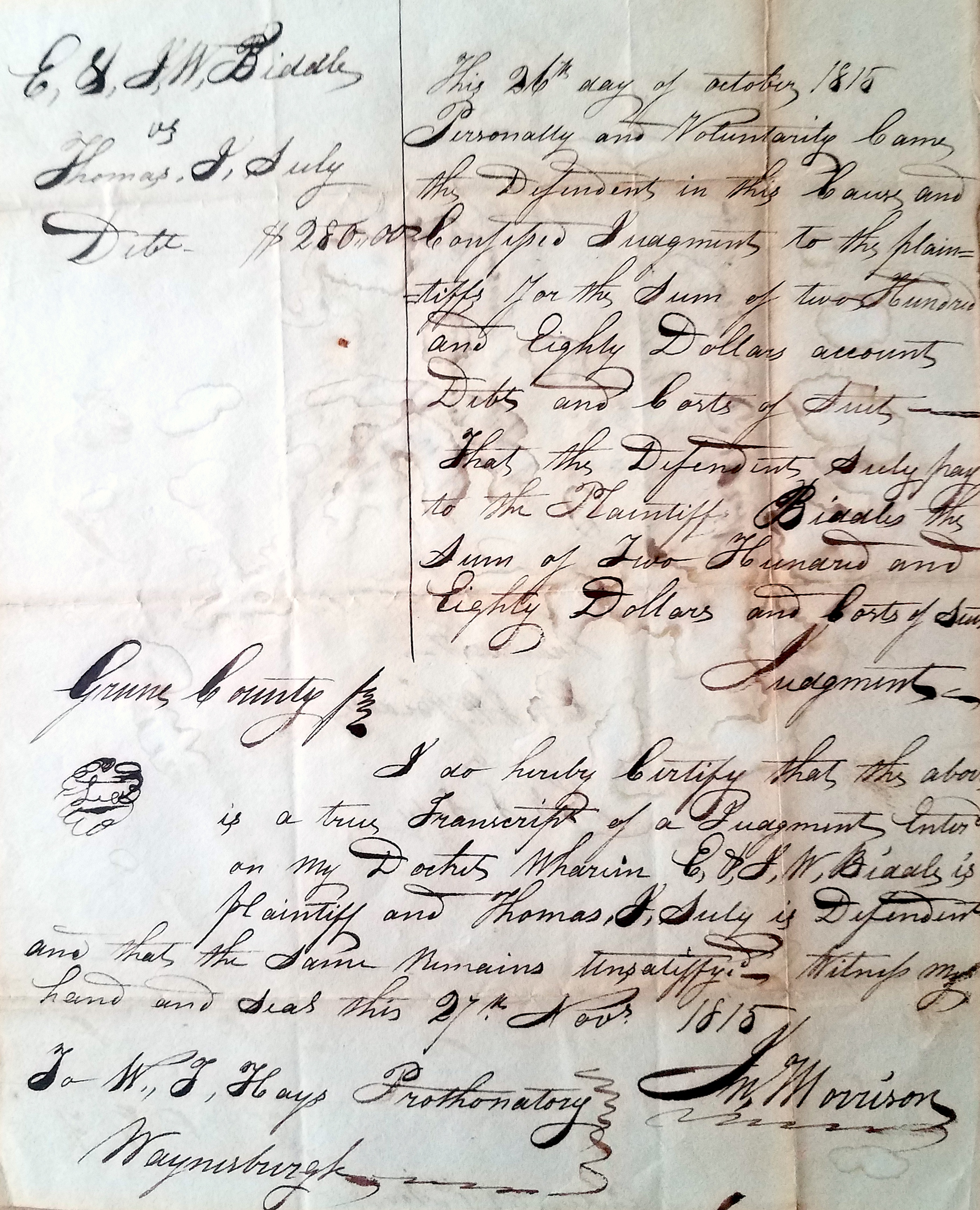

Judgment Liens: A judgment lien is a general lien. A judgment lien is created by a court decree finalizing a lawsuit. If your client is sued for a personal injury claim and loses, the winner can record that judgment. In New York, a judgment lien against real property remains valid for ten years.

An 1815 judicial judgment of debt. A recorded court judgment creates a general involuntary lien that attaches to all real and personal property owned by the debtor within that jurisdiction. -

Estate Tax Liens: An estate tax lien is a general lien. When an individual passes away, an estate tax lien is placed on a deceased person's property to secure the payment of estate taxes. If you are selling a property for an estate, the title company will require proof that the IRS and New York State have issued tax waivers before clearing the title to close.

-

Corporate Franchise Tax Liens: A corporate franchise tax lien is a general lien. It secures the payment of state taxes imposed on corporations for the privilege of doing business in New York. If a corporate seller fails to pay this, their entire portfolio of real estate is encumbered.

-

Internal Revenue Service (IRS) Tax Liens: An Internal Revenue Service tax lien is a general lien. An Internal Revenue Service tax lien results from a person's failure to pay federal income taxes. The IRS casts a massive net over everything the taxpayer owns.

Imagine a property is heavily encumbered, and the owner defaults. The property is foreclosed upon and sold at auction for $400,000. But the owner owed $300,000 on a first mortgage, $150,000 on a second mortgage, and $50,000 to a contractor. The math does not work; someone is going to lose money.

Who gets paid first?

Lien priority generally determines the order in which lienholders are paid if a property is sold. The foundational rule of real estate priority is "first in time, first in right." Lien priority is typically established by the date and time a lien is recorded in the public records. The earlier the timestamp, the higher the priority.

However, the government writes the laws, and the government always ensures it gets paid first. There are massive exceptions to the "first in time" rule:

- Real estate property tax liens take priority over all other recorded liens. Even if a bank recorded a mortgage ten years ago, a property tax lien filed yesterday jumps to the absolute front of the line.

- Special assessment liens take priority over previously recorded mortgages. If the city installs new sidewalks and assesses the property for the cost, that municipal lien supersedes the bank's mortgage.

Occasionally, creditors will negotiate to change this order. A subordination agreement changes the legal priority of existing liens. A subordination agreement allows a later-recorded lien to take precedence over an earlier-recorded lien. This is highly common in refinancing: a second mortgage holder might agree to subordinate their position to a brand-new first mortgage so the homeowner can secure better lending terms, keeping the financial ecosystem moving.

Finally, in your day-to-day work reviewing title reports, you will frequently see a term that causes immediate panic in buyers: Lis Pendens.

Translated from Latin, it means "suit pending." A lis pendens is a recorded notice of a pending lawsuit affecting the title to a specific real property.

Crucially, you must educate your clients on the legal mechanics here: a lis pendens is not a lien itself. It is not an active debt, and it does not allow anyone to force a sale today. Instead, a lis pendens warns potential real estate buyers of a possible future lien against the property. It acts as a glaring red flag in the public record. Because any buyer who purchases the property does so with "constructive notice" of the lawsuit, they will be legally bound by whatever judgment the court eventually hands down. Consequently, a lis pendens makes a property practically impossible to finance or sell until the underlying lawsuit is resolved or dismissed.

As an aspiring real estate professional, mastering these concepts moves you from a mere tour guide to a vital fiduciary. When you understand exactly how liens behave, prioritize, and attach, you possess the structural knowledge required to guide your clients through the complex reality of New York property transfers.