Specific Liens

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

A deed transfers the physical earth and the structure upon it, but the title carries the invisible financial anchors attached to that specific patch of soil. In the mechanics of real estate, ownership is rarely absolute; it is subject to a web of claims, debts, and obligations. When an individual purchases a property, they are not just buying walls and a roof; they are inheriting the legal history of that parcel. If a previous owner failed to pay their property taxes, ignored a contractor's invoice, or took out a mortgage, those financial obligations do not vanish when the keys change hands. They are bolted to the property itself in the form of liens.

To understand how real estate transactions actually function, we must first dissect the fundamental mechanism of a lien.

A lien is a financial encumbrance placed on a real estate parcel to secure the payment of a debt.

When a lien is filed, the property itself becomes the collateral. However, not all liens behave identically in the eyes of the law. The crucial distinction lies in the scope of the lien's grip on the debtor's assets: specific versus general.

A general lien attaches to all of a debtor's real and personal property assets. For example, if a homeowner faces a lawsuit for an unpaid credit card debt and loses, the resulting judgment lien is classified as a general lien rather than a specific lien. It blankets everything they own: their bank accounts, their vehicles, and any real estate they hold.

Conversely, a specific lien attaches exclusively to a single, specifically identified parcel of real estate. A specific lien does not affect the property owner's other real estate holdings or personal property. If a homeowner has a specific lien on a townhouse in Manhattan, it has no legal bearing on their vacation home in the Catskills or their investment portfolio.

Liens are further categorized by how they are conceived:

- A voluntary lien is created intentionally by the property owner's own actions, usually as a calculated trade-off to access capital.

- An involuntary lien is created by law without the property owner's consent, typically as a punitive or corrective measure for an unpaid obligation.

As a real estate professional, you will navigate four primary specific liens on a near-daily basis. Each has a distinct origin and purpose in the real estate economy.

1. The Mortgage Lien

The most common encumbrance is the mortgage lien, which is a specific, voluntary lien given to a lender as security for a real estate loan. When a client purchases a $750,000 home and borrows $600,000, the bank does not simply hand over the cash based on a handshake. The buyer intentionally grants the bank a mortgage lien against the newly acquired property. If the buyer defaults, the bank has a specific, legally actionable path to recoup its capital.

2. The Real Estate Tax Lien

A real estate tax lien is a specific, involuntary lien placed on a property for unpaid municipal property taxes. Municipalities rely on property taxes to fund essential operations. When an owner fails to pay, the local government does not sue the owner personally; it places a lien directly on the property.

3. The Special Assessment Lien

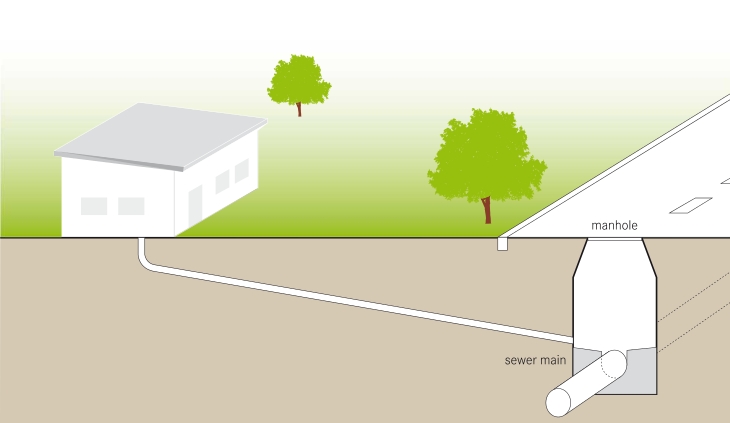

Similar to a tax lien, a special assessment lien is a specific, involuntary lien imposed to fund public improvements that directly benefit a specific property. If a city installs new municipal sewer lines or paved sidewalks on a residential block, the properties directly benefiting from that upgrade are assessed a proportionate share of the cost. The lien ensures the municipality is reimbursed for the localized improvement.

4. The Mechanic's Lien

A mechanic's lien is a specific, involuntary lien filed by an individual or entity that provided labor or materials to improve real property. If a homeowner hires a contractor to renovate a kitchen and refuses to pay the final $25,000 invoice, the contractor can file a mechanic's lien against the home. This effectively weaponizes the property's title against the non-paying owner.

New York maintains incredibly strict procedural physics governing mechanic's liens. A single procedural error will render the lien legally void. For real estate practitioners, understanding these precise rules is critical, as a valid mechanic's lien can halt a multi-million dollar closing.

First, consider the timeline for filing. The clock begins ticking on the last date labor or materials were provided to the property.

| Property Classification | New York Filing Deadline |

|---|---|

| Single-Family Residential | Must be filed within four months of the last date labor or materials were provided. |

| Commercial Property | Must be filed within eight months of the last date labor or materials were provided. |

Filing the document is merely the first step. A New York mechanic's lien document must be formally notarized to be considered legally valid for recording. Furthermore, the law dictates exactly what can be claimed: indirect or consequential damages cannot be legally included in a New York mechanic's lien claim amount. If a contractor suffered lost profits or administrative delays because of a dispute with the owner, they cannot pad the lien with those figures; the lien must strictly reflect the value of the actual labor and materials integrated into the property.

Once filed, the lienholder faces immediate procedural obligations:

- Notice: A property owner must be formally served with a copy of a New York mechanic's lien within 30 days of the lien's filing date.

- Verification: Proof of service for a New York mechanic's lien must be filed with the county recorder to maintain the lien's legal validity. Failure to file this proof extinguishes the lien entirely.

If perfectly executed, a New York mechanic's lien is initially valid for exactly one year from the exact date of filing. However, it is not a permanent fixture. If the dispute remains unresolved as the expiration approaches, under New York law, an active mechanic's lien can be formally extended beyond the initial one-year validity period by filing an extension with the county clerk.

Specific liens are not just theoretical constructs; they are mechanical barriers to the transfer of real estate. Filing a specific lien creates a formal cloud on the property's title.

A cloud on title is any document, claim, unreleased lien, or encumbrance that might invalidate or impair the title to real property or make the title doubtful.

A cloud on title caused by an active lien can block a property owner from successfully selling or refinancing the encumbered property. Buyers will not purchase a home burdened by someone else's debt, and new lenders will not issue a mortgage if their security interest is threatened by existing claims.

Consequently, a title search is conducted before a real estate closing to identify any recorded specific liens attached to the subject property. This search investigates public land records to ensure the seller has the right to transfer the property free and clear. Occasionally, a title search will uncover a lis pendens. While not a lien itself, a lis pendens is a recorded public notice indicating that a lawsuit affecting the title to a specific real estate parcel is currently pending. It serves as a stark warning to prospective buyers that the property is entangled in active litigation.

To resolve these issues, during a real estate closing, outstanding specific liens must typically be paid off to transfer a clear title to the property buyer. The closing attorney or title company takes the buyer's funds, pays the outstanding lienholders (such as the seller's original mortgage lender or an unpaid contractor), and demands a release.

A release of lien is a legal document issued by a lienholder confirming that a specific debt has been fully satisfied. However, merely holding the document is insufficient. Recording a release of lien removes the associated financial encumbrance from the property's public title records, officially clearing the cloud on the title and allowing the transaction to proceed.

If a property owner defaults on their obligations and the property is forced into foreclosure, a vital question arises: if the sale proceeds are insufficient to pay all creditors, who gets paid first?

Lien priority determines the exact order in which lienholders receive payment if a property is sold in a foreclosure proceeding. The fundamental doctrine governing this hierarchy is the "first in time, first in right" rule. This rule establishes that lien priority is generally determined by the exact date and time a lien is recorded in public land records. A mortgage recorded in 2018 will be paid before a mechanic's lien recorded in 2022.

However, the state exerts its own authority over this timeline, creating strict exceptions known as "super priority" liens.

- Real property tax liens hold super priority status over all other recorded liens. No matter when a mortgage was recorded, real property tax liens take priority over previously recorded mortgage liens in New York. The government always eats first.

- Similarly, special assessment liens hold super priority status over previously recorded mortgages and mechanic's liens, protecting the municipality's investment in public infrastructure.

Finally, New York law makes a specific and highly tested accommodation regarding condominiums. In New York, a condominium association's lien for unpaid common charges is legally subordinate to a recorded first mortgage on the unit. This means if a condo is foreclosed upon, the bank holding the first mortgage will be paid before the condo board recovers its unpaid monthly common charges, regardless of the recording dates.

Because priority is so vital to lenders, there are times when the rigid "first in time" rule must be artificially rearranged to facilitate modern financial transactions. This is achieved through a specific legal tool.

A subordination agreement is a legal contract where a superior lienholder voluntarily agrees to lower the lienholder's priority position behind a junior lienholder.

By executing this contract, a subordination agreement directly alters the standard "first in time, first in right" recording priority rule.

To understand why a lender would ever willingly step backward in line, consider a common scenario: mortgage refinancing. Subordination agreements are frequently used in mortgage refinancing to ensure a new primary mortgage lender secures the first-lien position.

Imagine a homeowner has a $400,000 primary mortgage (recorded in 2015) and a $50,000 Home Equity Line of Credit (HELOC, recorded in 2018). In 2026, the homeowner wishes to refinance the primary mortgage to secure a lower interest rate. They take out a new $400,000 mortgage to pay off the 2015 loan.

According to the "first in time" rule, the moment the 2015 loan is paid off and released, the 2018 HELOC slides into the first-priority position. The new 2026 primary mortgage would be stuck in second place. No rational bank will issue a $400,000 primary loan and accept a second-lien position behind a HELOC.

To solve this, the new lender requires the HELOC lender to sign a subordination agreement. The HELOC lender agrees to subordinate their 2018 claim to the new 2026 mortgage. The queue is artificially reordered, the new primary lender secures their required first-lien position, and the refinance successfully closes. Understanding the mechanics of subordination allows you to explain to a client exactly why their refinance requires additional paperwork from their secondary lender, bridging the gap between abstract property law and their practical reality.