When a fire destroys a ten-year-old roof on a Staten Islandcolonial, the fundamental question of property insurance arises: does the insurance company pay to install a brand-new roof, or do they hand over the cash value of a ten-year-old pile of shingles? The difference between those two outcomes represents tens of thousands of dollars, and as a real estate professional guiding a buyer through their largest financial transaction, understanding how those dollars are calculated, collected, and protected is a critical component of your practice. Property insurance is not merely a peripheral safeguard; it is the financial mortar that holds a mortgage agreement together. Without it, lenders will not lend, closings will not happen, and buyers remain exposed to catastrophic loss.

A historic colonial home on Staten Island. The replacement materials and specialized labor required to rebuild older properties highlight the financial stakes between Actual Cash Value and Replacement Cost policies.

To navigate these waters effectively, a real estate salesperson must understand the mechanics of property insurance valuation, the strict requirements lenders impose at the closing table, and the precise boundaries of their own professional licensure.

At the core of property insurance are two distinct methodologies for calculating the payout after a covered peril (such as fire, wind, or theft). As an agent, you must understand these concepts to explain why a buyer's insurance premiums might vary drastically between different policy quotes.

Severe wind damage to a residential home. Property insurance policies dictate exactly how the financial cost of repairing such covered perils will be calculated and paid out.

Think of replacement cost as a financial time machine that repairs the damage using today's prices, completely ignoring the wear and tear the property had previously suffered.

Replacement cost is the current market cost to rebuild or repair a property using materials of similar kind and quality. Crucially, replacement cost insurance coverage does not subtract depreciation when calculating an insurance payout.

If that ten-year-old Staten Island roof is destroyed, a replacement cost policy pays the modern, current-market price to hire roofers and install brand-new, comparable shingles. The homeowner is made whole based on the reality of today's construction costs.

Actual Cash Value (ACV)

In contrast, Actual Cash Value takes a strictly mathematical approach to the passage of time.

Actual cash value (ACV) represents the replacement cost of a property minus any accumulated physical depreciation.

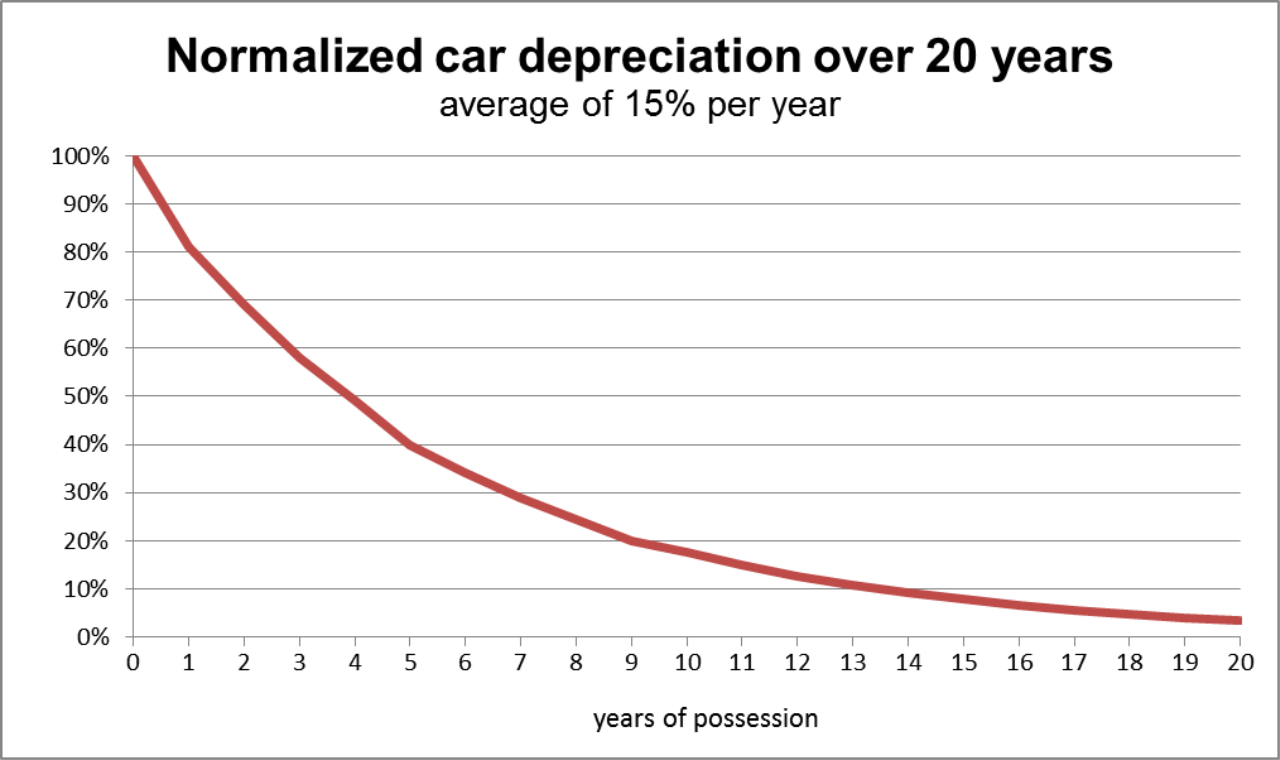

Depreciation in actual cash value calculations accounts for the specific age and condition of the damaged property. If a roof was expected to last 20 years and is destroyed in year 10, it has lost half its value. An ACV policy calculates the cost of a brand-new roof and subtracts 50%. The homeowner receives a check for the remaining value, which means they will have to pay the difference out of their own pocket to hire a modern contractor.

A depreciation curve demonstrating how an asset loses measurable value over a 20-year lifespan. Actual Cash Value applies this exact mathematical principle to property components, subtracting accumulated wear and tear from the final insurance payout.

Because the insurance company takes on less financial risk by factoring in depreciation, actual cash value insurance policies generally result in lower premium costs compared to replacement cost policies.

Valuation Comparison Table

Feature

Replacement Cost

Actual Cash Value (ACV)

Calculation

Cost to rebuild today with similar materials.

Replacement Cost minus physical depreciation.

Depreciation

Ignored.

Subtracted based on age and condition.

Out-of-Pocket Risk

Lower (payout covers modern construction costs).

Higher (buyer covers the depreciation gap).

Premium Cost

Higher.

Lower.

If a buyer is paying all cash, insurance is highly advisable but legally optional. However, the vast majority of your clients will be financing their purchases. You must understand property insurance through the eyes of the bank.

Fundamentally, property insurance protects the financial interests of both the homeowner and the mortgage lender against covered perils. To a lender, the house is collateral. If the collateral burns to the ground and there is no insurance, the borrower will likely default on the loan, leaving the bank with a worthless pile of ash.

A structure fire resulting in a total loss. Because a home serves as collateral for a mortgage loan, lenders mandate property insurance to guarantee they can recover their funds if the property is completely destroyed.

Therefore, lenders typically require homebuyers to secure property insurance before finalizing a residential mortgage loan. A real estate agent must advise homebuyers that securing this insurance is a strictly mandatory step for obtaining a mortgage.

How much coverage does the bank demand? The minimum property insurance coverage required by a lender is usually equal to the outstanding mortgage balance. If a buyer takes out a $400,000 mortgage, the lender will insist on at least $400,000 in coverage to ensure their specific financial exposure is insulated.

Understanding the theory of insurance is fine, but you operate in the practical reality of real estate transactions. You must prepare your buyers for how insurance impacts their upfront closing costs and their ongoing monthly budget.

The Closing Table Requirements

A real estate agent should provide general information about the purpose of property insurance early in the home buying process to set proper financial expectations. Do not let your buyer discover these costs a week before closing.

To physically get the keys, the buyer must satisfy the lender's stringent upfront demands. Homebuyers must typically provide a valid insurance binder and proof of payment at the real estate closing. A binder is a temporary document proving that coverage has been initiated.

An 18th-century fire insurance contract. While modern policies are more complex, the core requirement remains unchanged: buyers must provide formal, documented proof of an insurance agreement at the closing table.

Furthermore, the lender will not allow the buyer to pay their insurance month-to-month right out of the gate. Lenders usually require the homebuyer to prepay the first full year of property insurance premiums prior to or at the real estate closing. This is a significant cash requirement that your buyer needs to have budgeted.

The Escrow Account and PITI

Once the first year is paid, how does the lender guarantee the buyer will keep paying the premium in year two, year three, and beyond? They take control of the payments.

A real estate agent should inform a buyer that property insurance premiums are often collected through a lender-managed escrow account.

Escrow Account: Lenders establish an escrow account to hold borrower funds specifically designated for paying annual property taxes and insurance premiums.

The mechanics are elegant and simple. The monthly insurance payment deposited into an escrow account is calculated as one-twelfth of the annual property insurance premium. If the annual premium is $1,200, the lender adds $100 to the buyer's monthly mortgage bill. The lender holds that $100 in the escrow account, and when the annual insurance bill comes due the following year, the lender pays it directly on the borrower's behalf.

A real estate agent must explain that a specific portion of the buyer's monthly mortgage payment will be allocated to this insurance escrow account. By doing so, you clarify that the cost of property insurance directly increases the buyer's total monthly housing expense.

In real estate, we refer to this total monthly burden using a specific acronym:

PITI: The total monthly housing expense including Principal, Interest, Taxes, and Insurance.

When a client asks, "What will my monthly payment be?", they are usually thinking only of Principal and Interest. It is your job to remind them of the "T" and the "I".

As an engaging, knowledgeable professional, your instinct will be to help your client solve every problem. However, New York State law establishes a bright, rigid line regarding your scope of practice when it comes to insurance.

You are the architectural guide of the transaction; you map out the territory, but you do not build the bridge.

A real estate salesperson is strictly prohibited from providing specific insurance advice or selling insurance without holding a valid insurance license.

If a client asks you, "Should I get an Actual Cash Value policy or a Replacement Cost policy to save money?" or "Do you think $500,000 in coverage is enough for this neighborhood?", you must immediately step back. Answering those questions crosses the line into unlicensed practice.

Instead, a real estate agent must advise clients to consult a licensed insurance broker or agent for specific policy recommendations.

Your professional duty is twofold:

Explain the Process: Teach them why the lender needs it, how the escrow account works, and when the binder and pre-payments are due at closing.

Refer the Specifics: Guide them to a licensed insurance professional who can legally analyze their risk profile, calculate depreciation, and recommend the exact policy tailored to their needs.

Mastering this distinction protects your client from inadequate coverage, protects the transaction from closing delays, and most importantly, protects your real estate license from state disciplinary action.