Economic Principles and Sales Comparison Approach

Value in real estate is not an intrinsic physical property like mass or volume; it is an emergent phenomenon born from human desires colliding with physical and legal constraints. A quarter-acre of dirt in Manhattan commands millions not because the soil is chemically superior to a farm in Nebraska, but because human economic forces converge to assign it worth. For the aspiring real estate professional, understanding value is the mechanism by which you advise clients, negotiate deals, and ultimately earn your livelihood. This guide dissects both the underlying economic engines that generate property value and the precise methodology used to quantify it in the open market.

Before we can measure value, we must understand why it exists at all. To possess value in the real estate market, a property must exhibit four fundamental characteristics.

The Essential Elements of Value (DUST) The essential elements of real estate value are Demand, Utility, Scarcity, and Transferability, often remembered by the acronym DUST.

Let us examine the mechanics of each:

- Demand: It is not enough for someone to simply want a property. Demand in real estate valuation refers to the desire to purchase a property combined with the financial ability to complete the purchase. A thousand people might desire a $5 million mansion, but if only two have the capital, the market demand is two.

- Utility: Utility refers to the ability of a property to satisfy a specific human need or desire. A steeply sloped lot that cannot be built upon lacks utility for residential development, effectively erasing its value for that purpose.

- Scarcity: Scarcity refers to the limited supply of real estate in a given location. Land is finite. If a specific neighborhood is fully developed and highly desirable, the absolute limit on available homes drives value upward.

- Transferability: Transferability refers to the ability to legally and easily transfer ownership rights of a property from one person to another. If a property is locked in an unsolvable legal dispute with a clouded title, its value plummets because the buyer cannot confidently acquire the rights to it.

Market Value vs. Market Price

A critical distinction you will navigate daily is the difference between value and price. Think of value as the economic theory, and price as the historical experiment.

Market value represents an objective estimate based on professional analysis. It is defined as the most probable price a property will bring in a competitive and open market under all conditions requisite to a fair sale. It is what should happen when buyers and sellers act rationally.

Market price, on the other hand, is the actual amount of money paid for a property in a specific transaction. Market price represents a historical factual event. If a buyer, desperate to secure a home before the school year begins, overpays by $50,000 in a bidding war, the market price is recorded at the higher figure, even though the market value remains lower.

Property values do not exist in a vacuum. They are constantly pushed and pulled by a web of economic laws. Understanding these principles allows you to explain to your clients why their property is worth what it is.

Forces of the Market

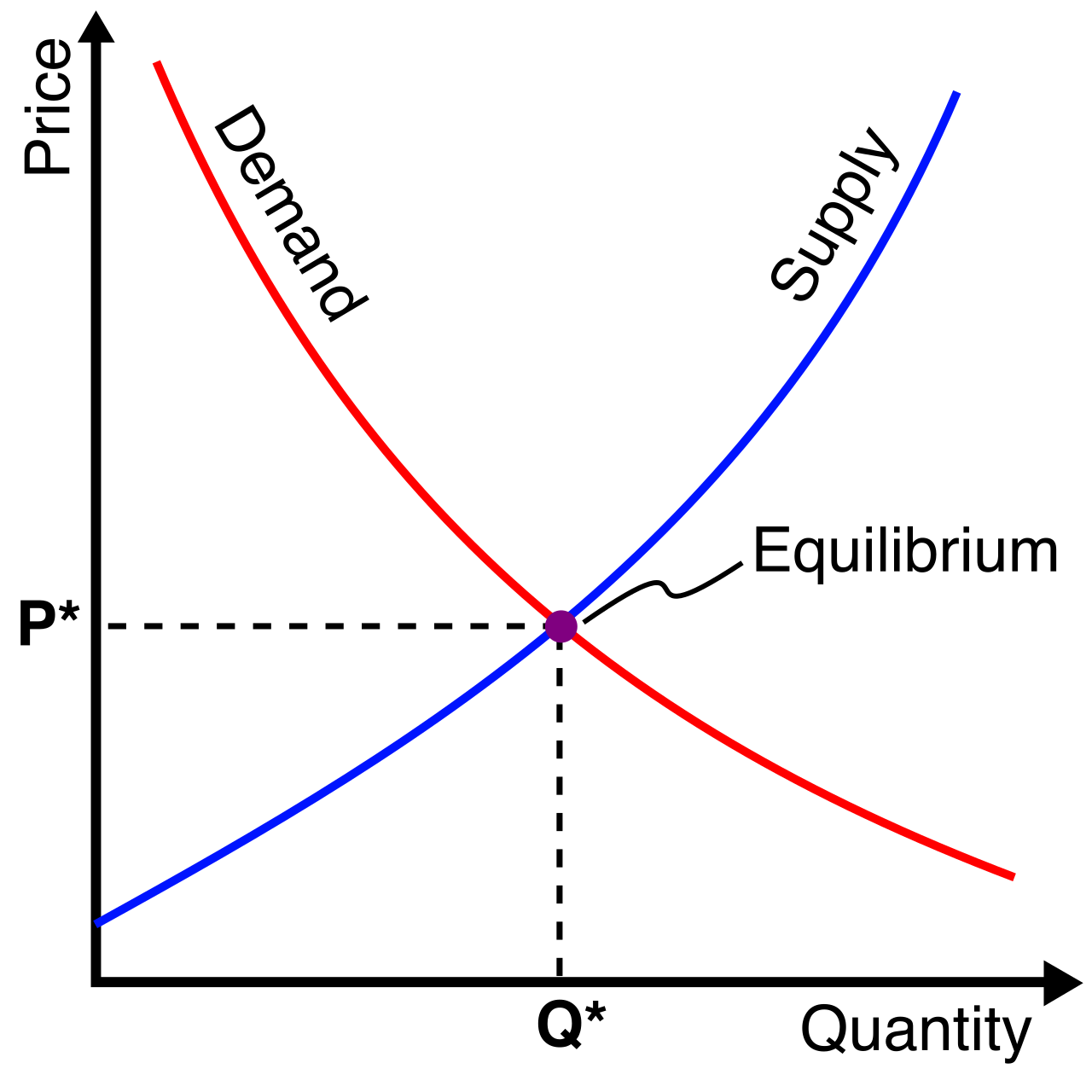

- Supply and Demand: The most foundational law of economics. The principle of supply and demand dictates that property value rises when demand exceeds supply. Conversely, the principle dictates that property value falls when supply exceeds demand.

- Competition: The principle of competition states that high profits in a real estate market will attract new competitors. If a developer makes staggering profits building luxury condos downtown, other developers will swiftly purchase nearby lots to build their own, eventually increasing supply and stabilizing prices.

- Anticipation: The principle of anticipation states that real estate value is created by the expectation of future benefits derived from the property. A dilapidated building surges in value not because of its current state, but because the city announced a massive tech campus is being built across the street. Buyers anticipate future rental income or resale profit.

- Change: The world is not static. The principle of change asserts that physical, governmental, economic, and social conditions constantly affect property value. A new zoning law, a shifting demographic, or a deteriorating local economy will reliably shift valuations.

Neighborhood Dynamics

How a property interacts with its neighbors is crucial to its valuation.

- Conformity: The principle of conformity holds that maximum value is realized when a property is in harmony with its surrounding environment. A modest, three-bedroom home achieves its highest value when surrounded by other modest, three-bedroom homes.

- Regression: Regression is the economic principle where a higher-quality property loses value due to its association with nearby lower-quality properties. If you build a $2 million mansion in a neighborhood of $300,000 homes, the mansion's value will be pulled down by its surroundings.

- Progression: Conversely, progression is the economic principle where a lower-quality property gains value due to its association with nearby higher-quality properties. The "worst house on the best street" benefits immensely from this phenomenon.

Improvements and Components

When homeowners undertake renovations, they often mistakenly believe that spending a dollar automatically adds a dollar of value. As a professional, you must guide them using these three principles:

- Contribution: The principle of contribution states that the value of any property component is measured strictly by its contribution to the whole property's value. Crucially, a property component's construction cost does not necessarily equal the component's added value to the property. Spending $40,000 to install an intricate koi pond may only add $5,000 to the home's final market value.

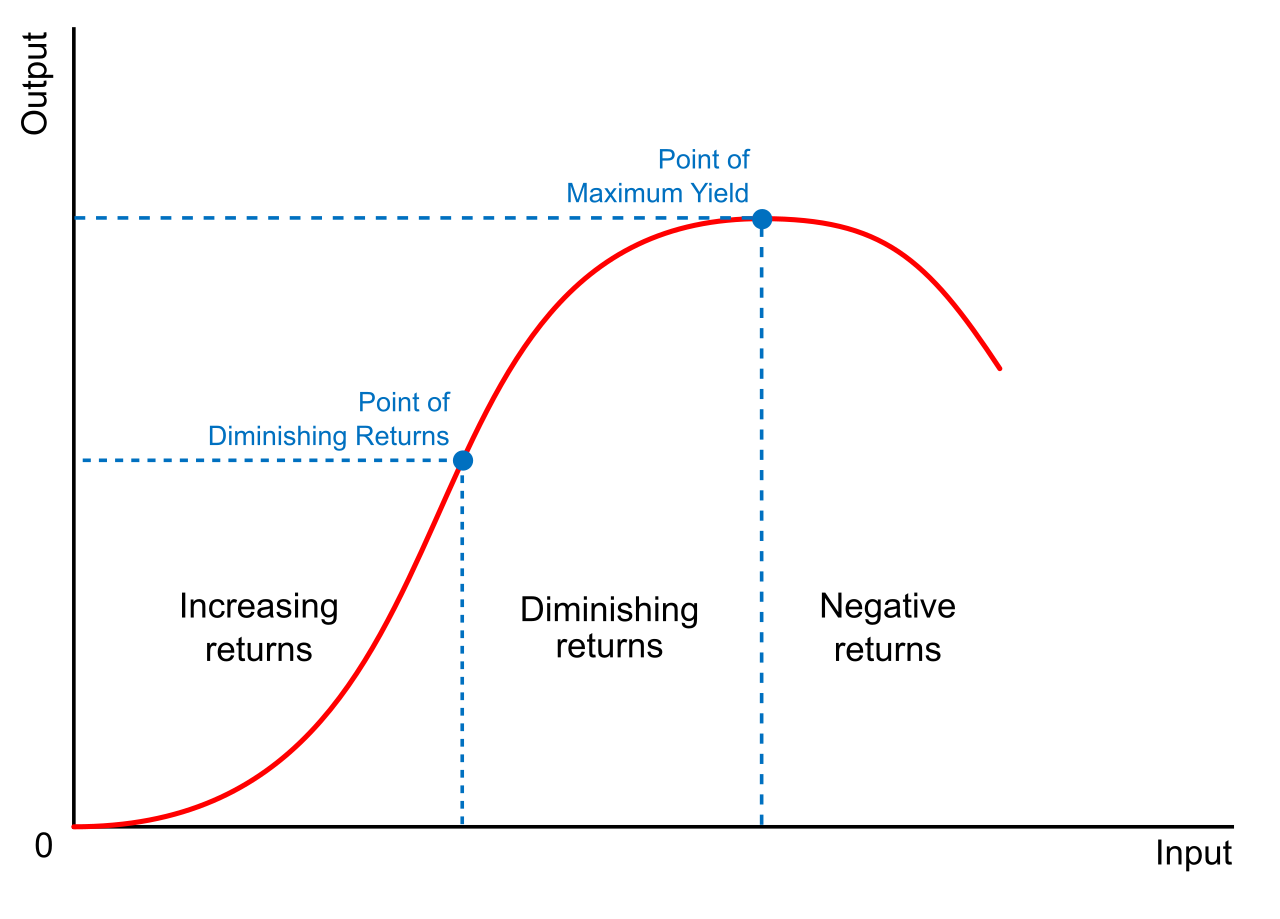

- Increasing Returns: The principle of increasing returns applies when property improvements produce a proportional or greater increase in overall property value. (e.g., adding a second bathroom to a one-bathroom home in a family neighborhood).

- Diminishing Returns: The law of diminishing returns applies when additional property improvements no longer bring a corresponding increase in overall property value. Once a home has four bathrooms, adding a fifth offers a rapidly shrinking return on investment.

Land Dynamics: Assemblage and Plottage

When dealing with land development, the whole is often greater than the sum of its parts.

- Assemblage is the process of merging two or more adjoining parcels of real estate into a single larger tract.

- Plottage is the result—specifically, the increase in total value that results from the successful assemblage of multiple adjoining parcels. If two adjacent lots are worth $50,000 each separately, but merging them allows a developer to build a commercial strip mall, the combined single lot might be worth $150,000. The extra $50,000 is the plottage value.

The Two Pillars of Appraisal

Highest and Best Use Highest and best use is the most profitable, legally permitted, physically possible, and financially feasible use of a property.

A vacant lot downtown might be currently used as a $10-a-day parking lot, but if it is legally zoned for a 10-story office building, its highest and best use is as an office building. Every real estate appraisal must determine and state the highest and best use of the subject property.

The Principle of Substitution The principle of substitution states that a buyer will pay no more for a property than the cost of acquiring an equally desirable substitute.

If there are three identical houses on the same block, a rational buyer will purchase the cheapest one. This powerful, intuitive concept is the engine behind our next major topic: it is the economic foundation of the sales comparison approach to valuation.

The sales comparison approach estimates value by comparing the subject property to recently sold similar properties. Because it relies heavily on what buyers are actually doing in the market, the sales comparison approach is also widely known as the market data approach.

When do we use it? It is the preferred appraisal method for valuing vacant land, and the sales comparison approach is considered the most reliable method for appraising single-family residential properties.

Selecting the Evidence: Comparables

The recently sold similar properties used in an appraisal are officially called comparables (or "comps"). However, you cannot just pick any sale.

An appraiser must select comparable properties that have sold in arm's-length transactions. An arm's-length transaction is a transaction between unrelated parties acting in their own best interests under no undue pressure.

If a father sells his house to his daughter for half its worth, or if a bank liquidates a property to recover a debt quickly, the price does not reflect true market value. Therefore, foreclosures and sales between family members are generally disqualified as arm's-length transactions.

The Mechanics of Adjustment

No two properties are perfectly identical. An appraiser adjusts the sales price of a comparable property to account for physical or market differences between the comparable and the subject property.

Here is the absolute, unbreakable golden rule of the sales comparison approach: Financial adjustments in the sales comparison approach are exclusively applied to the comparable property. An appraiser never adjusts the value of the subject property during the sales comparison approach.

Think of it like an algebra equation where the subject property is the "X" you are trying to solve for. You cannot change X; you can only manipulate the surrounding data to figure out what X is. You are adjusting the comp's price to answer the question: "What would the comparable property have sold for if it had exactly the same features as our subject property?"

The Rules of Adjustment:

- If a comparable property is superior to the subject property in a specific feature, the appraiser subtracts the value of that feature from the comparable's sales price.

- If a comparable property is inferior to the subject property in a specific feature, the appraiser adds the value of that feature to the comparable's sales price.

To quickly recall this on your exam, rely on these two standard memory aids used by real estate professionals for appraisal adjustments:

- CBS, standing for Comp Better, Subtract.

- CIA, standing for Comp Inferior, Add.

What Do We Adjust?

Appraisers make sales price adjustments for several specific categories of differences:

- Market Conditions: Appraisers make sales price adjustments for differences in market conditions based on the time elapsed since the comparable property was sold. (If the comp sold 8 months ago and market prices have risen 5% since then, the comp's price is adjusted upward).

- Location: Appraisers make sales price adjustments for differences in location between the comparable property and the subject property. (e.g., The comp backs up to a loud highway; the subject is on a quiet cul-de-sac. Comp Inferior → Add).

- Physical Characteristics: Appraisers make sales price adjustments for differences in physical characteristics like square footage or the number of bathrooms.

- Conditions of Sale: Appraisers make sales price adjustments for differences in the conditions of sale, such as the inclusion of seller concessions. (If the seller of the comp paid $5,000 toward the buyer's closing costs, the comp's effective price was actually $5,000 lower).

- Financing Terms: Appraisers make sales price adjustments for differences in financing terms between the comparable sale and the subject property, such as instances where the seller provided an unusually low-interest owner-financing deal that inflated the sale price.

A Practical Scenario

- Subject Property: 3 Bedrooms, 2 Bathrooms.

- Comparable Sale: 3 Bedrooms, 3 Bathrooms. Sold for $400,000.

- Analysis: The comp is superior because it has an extra bathroom. Let us assume market data shows a bathroom is worth $10,000.

- Action: Apply CBS (Comp Better, Subtract). We subtract $10,000 from the comparable.

- Adjusted Price: The adjusted value of the comparable is $390,000. This tells us that if the comparable had only 2 bathrooms like our subject, it would have sold for $390,000.

After adjusting three to five comparable properties, you will be left with several different adjusted sales prices. For instance, Comp 1 adjusts to $400,000; Comp 2 adjusts to $405,000; Comp 3 adjusts to $398,000.

How do you establish the final appraised value?

Reconciliation is the final process of analyzing and weighing the adjusted findings from different comparables to arrive at a single estimate of value.

Crucially, a simple mathematical average of the adjusted sales prices of comparable properties is not a valid method for final appraisal reconciliation. Real estate is not an exact science, and all comps are not created equal. Instead of averaging, the appraiser applies weighted logic:

- During reconciliation, an appraiser gives the most weight to the comparable property that required the fewest total adjustments. Fewer adjustments mean the comp was already very similar to the subject, making the data inherently more reliable.

- Furthermore, during reconciliation, an appraiser gives the most weight to the comparable property that is most physically and geographically similar to the subject property.

By applying a deep understanding of economic principles and mastering the precise mechanics of the sales comparison approach, you transform raw market chaos into clear, defensible data for your clients.