Margin Accounts and Trading Rules

Purchasing securities on margin is fundamentally identical to acquiring real estate with a mortgage, with one volatile distinction: the collateral securing the loan fluctuates in value minute by minute. For a broker-dealer agent, managing a client's margin account is not merely a matter of processing paperwork for an extended line of credit; it is an active, structural balancing act between client leverage and systemic risk. When a client borrows capital to amplify their purchasing power, the broker-dealer assumes the role of the lender, requiring strict regulatory guardrails to ensure that a sudden market downturn does not leave the firm holding worthless collateral. These guardrails—dictated by the Federal Reserve, enforced by FINRA, and codified under state law by NASAA—form a rigid framework determining exactly how much credit can be extended, what happens when collateral values plummet, and precisely what legal agreements must be signed before the first borrowed dollar is deployed.

To understand margin, you must first understand its origins. Following the market crash of 1929, the federal government realized that unregulated borrowing to buy stocks posed a catastrophic threat to the national banking system. Consequently, Regulation T is established by the Federal Reserve Board.

At its core, Regulation T governs the extension of credit by broker-dealers to customers for purchasing securities. The Federal Reserve dictates the maximum amount of leverage a broker-dealer can offer to a retail investor. Currently, the Regulation T initial margin requirement for purchasing most equity securities is 50 percent of the purchase price.

If a client wishes to purchase $10,000 worth of a marginable stock, Regulation T requires them to deposit $5,000 in equity. The broker-dealer will lend the remaining $5,000.

But when must this capital actually arrive? Under Regulation T, a customer must deposit the required initial margin within two business days following the regular-way settlement date of the trade. Since modern regular-way settlement for equities is one business day after the trade date (T+1), the Regulation T payment deadline effectively falls on T+3 (trade date plus three business days).

While the Federal Reserve dictates the percentage of leverage, the Financial Industry Regulatory Authority (FINRA) establishes the absolute dollar minimums required to play the game.

FINRA requires a minimum initial equity deposit of $2,000 for a newly opened margin account.

Because of this strict $2,000 floor, the mathematical 50 percent rule of Regulation T does not uniformly apply to very small trades. If a client’s initial margin purchase is mathematically small enough that 50 percent would fall below the $2,000 threshold, FINRA rules override Regulation T:

- If the purchase is between $2,000 and $4,000, the client must deposit exactly $2,000.

- A customer must deposit 100 percent of the purchase price if the initial margin purchase is less than $2,000.

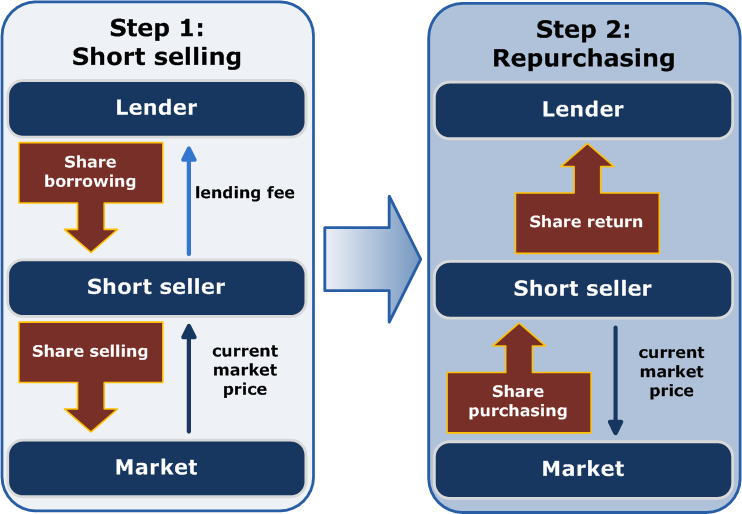

Note on Short Selling: While an investor can purchase stocks in a cash account, short selling of securities must always be executed within a margin account. Because shorting involves borrowing shares to sell them on the open market, it is inherently a credit transaction subject to all initial and minimum margin requirements.

Once the account is funded and the trade is executed, you must continually monitor the health of the position. To do this, you must master two structural concepts: the debit balance and account equity.

- A margin account debit balance represents the amount of money a customer has borrowed from the broker-dealer. Think of this as the principal on the loan. Unless the client pays it off or borrows more, this number remains static (ignoring accrued interest).

- Margin account equity is calculated by subtracting the debit balance from the current market value of the long securities in the account.

Formula: Current Market Value (CMV) – Debit Balance (DR) = Equity (EQ)

If your client buys $10,000 of stock with $5,000 cash and $5,000 borrowed:

- CMV = $10,000

- Debit Balance = $5,000

- Equity = $5,000

If the market value drops to $8,000:

- CMV = $8,000

- Debit Balance = $5,000 (the loan doesn't shrink just because the stock dropped)

- Equity = $3,000

Because the equity in the account absorbs 100 percent of the market losses, an investor's protective cushion can erode rapidly. To protect broker-dealers from taking a loss on the loan, FINRA Rule 4210 establishes the minimum maintenance margin requirements for broker-dealer margin accounts.

- The minimum FINRA maintenance margin requirement for long equity positions is 25 percent of the current market value.

- Because short positions expose the firm to theoretically infinite losses (a stock can rise indefinitely), the minimum FINRA maintenance margin requirement for short equity positions is 30 percent of the current market value.

A maintenance margin call is triggered when the equity in a margin account drops below the minimum FINRA maintenance requirement. However, broker-dealers rarely want to wait until a client is resting exactly on the regulatory edge. Therefore, broker-dealers are permitted to establish internal house maintenance margin requirements higher than the FINRA minimums (e.g., demanding 35 percent maintenance instead of 25 percent).

Satisfying the Call

When a client receives a maintenance margin call, they must act immediately to restore their equity levels. They have two primary ways to do this:

- A customer may satisfy a maintenance margin call by depositing additional cash into the margin account. Every dollar of cash deposited reduces the debit balance by a dollar, thereby raising the equity by a dollar.

- A customer may satisfy a maintenance margin call by depositing fully paid marginable securities into the margin account. Because only a percentage of a marginable security's value counts toward usable equity, the client will generally need to deposit more in securities than they would in cash to meet the same call.

The Ultimate Penalty: Liquidation

What happens if the client ignores the call or cannot be reached? This is where the severe reality of margin trading comes into focus.

A broker-dealer possesses the contractual right to liquidate customer securities to meet an unsatisfied maintenance margin call. Furthermore, because market drops can accelerate rapidly into systemic crashes, a broker-dealer is not required to provide prior notice to a customer before liquidating securities to meet a maintenance margin call.

For a broker-dealer agent, it is crucial to convey this reality to your clients: the firm can and will sell their assets, at the firm's discretion, and the client will not have the luxury of choosing which specific stocks are liquidated.

Because of the extreme power the broker-dealer holds to liquidate assets and charge interest, opening a margin account is a highly formalized legal process. A standard margin account requires the customer to sign a multi-part margin agreement.

From a regulatory perspective under NASAA guidelines, timing is critical. NASAA considers executing a margin transaction without securing a written margin agreement promptly after the initial transaction to be an unethical business practice.

The standard margin agreement consists of three distinct components:

1. The Credit Agreement

The credit agreement component of a margin agreement discloses the terms under which the broker-dealer extends credit. As with any loan, the borrower has a right to know exactly how the financing costs are calculated. Consequently, the credit agreement must detail the specific method used for computing interest on the margin account debit balance.

2. The Hypothecation Agreement

Broker-dealers do not generally fund customer margin loans purely out of their own pockets; they borrow the money from commercial banks. To secure those bank loans, the broker-dealer uses the customer's purchased securities as collateral.

The hypothecation agreement grants the broker-dealer permission to pledge the customer's securities as collateral for a bank loan.

There are strict legal limits to this practice. A broker-dealer may pledge a customer's securities for a loan amount up to 140 percent of the customer's debit balance. If a customer owes the broker-dealer $10,000 (their debit balance), the broker-dealer can only pledge $14,000 worth of that customer's stock to the bank.

Furthermore, state and federal laws enforce strict physical separation of assets:

- A broker-dealer is prohibited from commingling a customer's fully paid securities with margin securities.

- A broker-dealer is prohibited from commingling the securities of different customers as collateral without the written consent of each customer.

Why does this matter? If the broker-dealer goes bankrupt, the bank will seize the pledged collateral. If Customer A's stock is commingled with Customer B's stock, disentangling who owns what becomes a forensic nightmare. Conveniently, the hypothecation agreement provides the required written consent for a broker-dealer to commingle customer securities for collateral purposes.

3. The Loan Consent Agreement

While the credit and hypothecation agreements are mandatory to open a margin account, the loan consent agreement is the only optional component of the standard margin account agreement.

The loan consent agreement allows a broker-dealer to lend a customer's margin securities to other investors or broker-dealers.

Why would a broker-dealer want to borrow a client's stock? To facilitate the market machinery of short selling. Securities lent under a loan consent agreement are typically utilized to facilitate short sales by other market participants.

Because this exposes the client to certain minor risks (such as losing voting rights on the lent shares or receiving substitute payments in lieu of standard dividends), a broker-dealer is prohibited from forcing a customer to sign a loan consent agreement as a mandatory condition of opening a margin account.

Finally, because the mechanics of margin trading inherently invite heavy losses and surprise liquidations, industry regulators refuse to rely solely on fine print hidden inside the margin agreement.

A broker-dealer must provide a margin risk disclosure document to a customer prior to or at the opening of a margin account. This document clearly, plainly outlines the risks—specifically emphasizing the fact that the firm can sell the client's securities without contacting them, that the client is not entitled to an extension of time on a margin call, and that the firm can increase its house maintenance margin requirements at any time without advance written notice.

Memories fade, however, and the risks of leverage do not. Therefore, broker-dealers must deliver the margin risk disclosure document to all margin customers on an annual basis.