Margin Accounts: Requirements and Initial Margin

Imagine purchasing a $500,000 property by putting down $250,000 in cash and borrowing the remainder from a bank, using the property itself as collateral. This fundamental mechanism of leverage—amplifying buying power through borrowed capital—is the exact premise of a margin account in the securities industry. However, unlike a static mortgage, the financial markets are violently kinetic. The value of the collateral fluctuates by the second. To protect the financial system from cascading defaults, regulators mandate an intricate framework of rules, deposits, and mathematical boundaries. As a General Securities Representative, mastering these mechanics is not just about passing an exam; it is about protecting your firm’s capital and navigating your clients through the volatile realities of leveraged trading.

Before a single dollar is lent, the broker-dealer must establish who is legally permitted to borrow. Not every investor or account type is built for the systemic risks of margin.

Because margin amplifies risk, margin accounts must be approved by a registered principal of the broker-dealer. This principal approval for a new margin account must occur before or promptly after the initial transaction.

As a representative, you will encounter clients who want to use margin in accounts where it is strictly forbidden or highly restricted. You must know these boundaries:

-

Fiduciary and Retirement Accounts: Individual Retirement Accounts (IRAs) cannot be used to trade on margin to borrow money for purchasing securities. The IRS strictly prohibits borrowing against retirement assets. Similarly, custodial accounts established under the Uniform Gifts to Minors Act (UGMA) or the Uniform Transfers to Minors Act (UTMA) generally prohibit the use of margin. You cannot gamble a minor's financial future on leveraged trades.

-

Corporate Accounts: These are permitted to use margin, but only if margin trading is not specifically restricted by the corporate charter. You must review their governing documents first.

-

Pattern Day Traders: For clients executing four or more day trades in five business days, the stakes are exceptionally high. Consequently, pattern day traders are subject to a minimum equity requirement of $25,000 to trade on margin, rather than the standard limits.

Highly volatile trading activity requires stricter safeguards; pattern day traders must maintain a minimum of $25,000 in equity to use margin and survive extreme market swings.

To open a margin account, a client must sign specialized documentation. Think of this paperwork as the legal plumbing that allows cash and securities to flow safely between the client, the broker-dealer, and the banks.

The mandatory paperwork to open a margin account involves two primary documents, with a third optional component.

1. The Credit Agreement (Mandatory)

When a client borrows money, they must pay interest. A margin account credit agreement discloses the terms under which a broker-dealer extends credit to a customer. Specifically, it must detail exactly how interest is calculated on a customer's debit balance and must outline the conditions under which interest rates may change.

2. The Hypothecation Agreement (Mandatory)

Broker-dealers do not always lend their own cash. Often, they borrow cash from a bank to lend to your client. To secure that bank loan, the broker-dealer pledges the client's purchased securities as collateral. A margin account hypothecation agreement permits a broker-dealer to pledge customer securities as collateral for a bank loan.

However, the broker-dealer cannot pledge the client's entire portfolio if the client only borrowed a small amount. FINRA rules prohibit a broker-dealer from pledging customer securities in excess of 140 percent of the customer's debit balance. If a client borrows $10,000, the broker-dealer can pledge up to $14,000 of the client's securities to the bank to secure that loan.

3. The Loan Consent Form (Optional)

A loan consent form is an optional component of a margin agreement. When signed, it allows a broker-dealer to lend a customer's margin securities to other customers for short sales. If your client refuses to sign this, they can still open a margin account; their shares simply remain segregated from the firm's lending pool.

Leverage is a double-edged sword, and clients often focus only on the edge that cuts in their favor. To enforce reality, broker-dealers must provide a Margin Risk Disclosure Document to customers at or prior to opening a margin account, and they must provide existing margin customers with this document on an annual basis.

The disclosures in this document are unforgiving and essential:

- It informs customers about the potential to lose more funds than the original margin account deposit.

- It warns that a firm can force the sale of securities without contacting the customer to meet a margin call.

- It clarifies that a customer is not entitled to an extension of time to meet a margin call.

- It states that a firm can increase house maintenance margin requirements at any time without advance written notice.

When your client calls, irate that their positions were liquidated while they were in a meeting, this document is your legal and professional shield.

Who decides how much credit can be extended? Not FINRA, and not the SEC. Regulation T of the Federal Reserve Board governs the extension of credit by broker-dealers to customers.

Regulation T sets the initial margin requirement for purchasing securities, whereas FINRA rules establish the minimum maintenance margin requirement for holding open margin positions once the trade is executed.

Regulation T requires an initial margin deposit of 50 percent of the market value for non-exempt equity securities. However, the Federal Reserve does not care about all securities. Low-risk debt instruments, specifically United States Treasury securities and Municipal bonds, are completely exempt from Regulation T margin requirements.

Deadlines and Violations

Under the standard T+1 settlement cycle, the actual settlement of the trade happens the next day. However, the Regulation T payment deadline for margin accounts and cash accounts is trade date plus three business days (T+3).

If a client misses this deadline:

- A broker-dealer may apply to FINRA for an extension of time if a customer fails to meet a Regulation T payment deadline.

- If no extension is granted, a broker-dealer must liquidate the unpaid position.

- Consequently, a customer's account is frozen for 90 days if an unpaid position is liquidated due to a missed Regulation T payment deadline.

- A customer with a frozen account isn't banned from trading, but they lose the privilege of credit: they must have fully cleared cash in the account before executing any new purchase orders.

When a client buys stock on margin, we call it a "long" account. The accounting here is beautifully simple.

Equity = Long Market Value (LMV) – Debit Balance

- In a long margin account, the Long Market Value represents the current market price of the purchased securities.

- The Debit Balance represents the amount of money the customer has borrowed from the broker-dealer.

- Equity represents the client's actual ownership value in the account.

Initial Margin Requirements for Long Accounts

While Regulation T demands 50%, FINRA enforces its own absolute minimums. FINRA requires a minimum equity deposit of $2,000 to open a new margin account. This creates a tiered system for new accounts:

- Purchases under $2,000: A customer purchasing less than $2,000 of securities in a new margin account must deposit 100 percent of the purchase price. (You cannot deposit $2,000 for a $800 trade).

- Purchases between $2,000 and $4,000: If a customer purchases between $2,000 and $4,000 of securities in a new margin account, the initial deposit requirement is exactly $2,000. (Even though 50% of $3,000 is $1,500, the FINRA minimum overrides it).

- Purchases over $4,000: If a customer purchases over $4,000 of securities in a margin account, the standard 50 percent Regulation T deposit requirement determines the initial deposit amount.

Meeting a Margin Call

If an account falls below required thresholds, a margin call is issued. A customer can meet a Regulation T margin call by depositing cash equal to the margin call amount. Alternatively, if they don't have cash, a customer can meet a Regulation T margin call by depositing fully paid marginable securities valued at twice the margin call amount.

Why twice the amount? Because under Regulation T, securities only have a 50% loan value. Fully paid marginable securities can be transferred into a margin account and used as collateral to meet a margin call without depositing additional cash, preserving the client's liquidity.

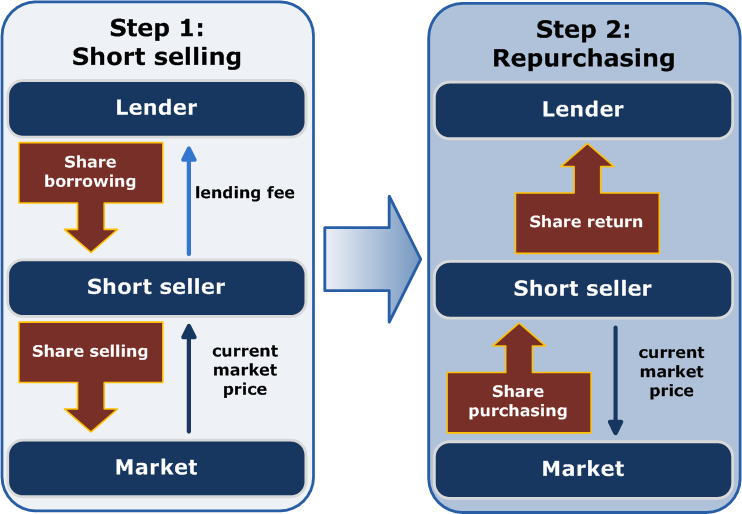

Short selling is an inherently perilous strategy with unlimited theoretical risk. Therefore, all short sales must be executed in a margin account.

An investor executing a short sale borrows shares from a broker-dealer to sell the borrowed shares in the open market, hoping to buy them back later at a lower price.

The accounting flips for short sales:

Equity = Credit Balance – Short Market Value (SMV)

- In a short margin account, the Short Market Value represents the current market price of the borrowed and sold securities.

- In a short margin account, the Credit Balance is the sum of the short sale proceeds and the customer's initial margin deposit. It is a static number unless the client adds or removes funds.

Initial Margin Requirements for Short Accounts

Because of the risk, FINRA is unyielding on short accounts. The FINRA minimum initial deposit for a new short margin account is $2,000.

Unlike long accounts, the $2,000 FINRA minimum deposit for short sales applies regardless of how small the initial short sale is. There is no "100% of the purchase price" exception here. The initial margin deposit for a short sale is always the greater of the 50 percent Regulation T requirement or the $2,000 FINRA minimum.

Let's apply this:

- A $3,000 short sale requires an initial deposit of $2,000 because the FINRA minimum exceeds the 50 percent Regulation T requirement ($1,500).

- A $5,000 short sale requires an initial deposit of $2,500 based on the 50 percent Regulation T requirement.

There is one highly specific exception for "cheap stock." The initial margin requirement for shorting stocks priced below $5.00 per share is the greater of $2.50 per share or 100 percent of the market value. Shorting penny stocks is exceptionally volatile, and the rules demand massive proportional collateral.

When a client's investments appreciate, their equity grows. Excess equity is the amount of equity in a margin account that exceeds the 50 percent Regulation T requirement.

When this happens, the excess equity in a margin account is credited to the Special Memorandum Account (SMA).

The SMA is widely misunderstood by novice investors. It is not a cash pile. The Special Memorandum Account represents a line of credit that a customer can use to purchase additional securities or withdraw as cash.

What happens when a client uses their SMA?

- Withdrawing Cash: Funds can be withdrawn from the Special Memorandum Account as cash. Doing so acts exactly like taking a cash advance on a credit card: withdrawing cash from the Special Memorandum Account increases the debit balance in a margin account, and consequently, decreases the overall equity in a margin account.

- Purchasing Securities: Clients can also use SMA to buy more stock. buying power in a standard margin account is equal to twice the amount of excess equity. (If you have $1,000 in SMA, you can buy $2,000 of stock). Purchasing securities using the Special Memorandum Account increases the debit balance (you are borrowing the money), but fundamentally, it does not immediately change the overall equity in a margin account. You added $2,000 of market value and $2,000 of debit. The net equity remains identical the moment the trade executes.

Finally, as a representative, you must know what can actually be bought with borrowed money. Not all financial products possess the liquidity or stability required to serve as collateral.

-

Options: Because they are highly volatile and depreciating assets, standard options contracts with expiration dates of nine months or less cannot be purchased on margin. A customer purchasing a standard options contract must deposit 100 percent of the options premium.

-

LEAPS: However, Long-Term Equity Anticipation Securities (LEAPS) options with more than nine months to expiration can be purchased on margin. The initial margin requirement for these longer-term options is 75 percent of the purchase price.

-

Mutual Funds: Because they are continuously offered under a prospectus, mutual funds cannot be purchased on margin. However, they possess collateral value over time: mutual funds become marginable securities after being held fully paid in a cash account for 30 days.

Because mutual funds are continuously offered to the public via a prospectus, they function similarly to new issues and cannot initially be purchased on margin. -

New Issues (IPOs): Similar to mutual funds, new issues of securities cannot be purchased on margin. The underwriter must collect full payment to stabilize the offering. However, new issues of securities become marginable 30 days after the initial public offering.

Mastering these rules transforms you from an order-taker into a professional risk manager. When you fully understand how the Debit Balance interacts with the Market Value, and how Regulation T interfaces with FINRA's strict minimums, you ensure your clients can leverage opportunities safely within the structural boundaries of the market.