Retirement Plans and ERISA

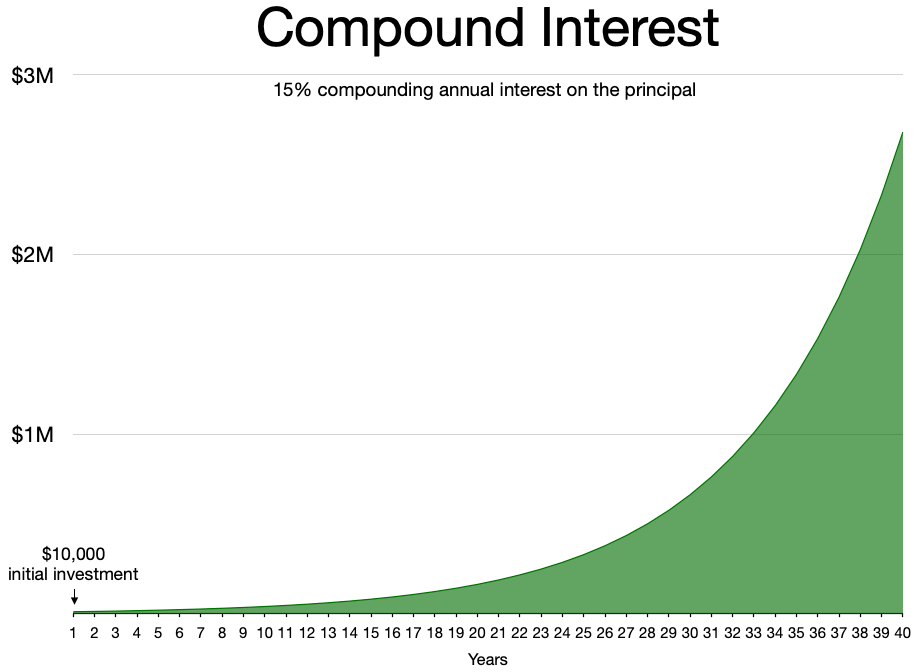

Capital accumulation is fundamentally a battle against the friction of taxation. Every time a financial asset generates yield, the tax code introduces drag, bleeding out the mathematical power of compound growth over decades. Retirement accounts and education savings plans are legally engineered vacuum chambers—environments where your clients' capital can compound entirely free from the annual drag of federal taxes. As a securities representative, your role is akin to a thermal engineer: you must guide client capital into the correct structural chambers without triggering explosive penalties, ensuring maximum energy is preserved for their retirement or educational needs.

To master these accounts for the Series 7, you must stop memorizing disconnected rules and start understanding the underlying physics of how the IRS tracks and taxes money.

To understand retirement accounts, you must first understand the concept of cost basis. In a retirement account, cost basis strictly represents the after-tax money that has already been taxed prior to being contributed. The IRS never taxes the same dollar twice.

Observe how this dictates the two primary categories of retirement plans:

- Standard Qualified Retirement Plan: This system uses pre-tax dollars for contributions and provides tax-deferred growth on all investments. Because the money went in before taxes were paid, the account has a cost basis of zero. Therefore, distributions taken from a fully funded pre-tax qualified retirement plan are taxed entirely as ordinary income.

- Standard Non-Qualified Retirement Plan: This system requires the use of after-tax dollars to fund the account. Since taxes were already paid on the seed money, the account has a positive cost basis. Consequently, only the accumulated earnings portion of a non-qualified retirement plan distribution is taxed as ordinary income upon withdrawal. The principal comes back out tax-free.

When a client sits across from you to open an IRA, you are dealing with capital on a purely individual level. The rules governing these accounts are strict, and violations carry heavy mathematical consequences.

The Traditional IRA: The Pre-Tax Engine

To gain entry into a Traditional IRA, an individual must have earned income—money generated from actively working, like W-2 wages or self-employment profits. Passive or external income sources do not qualify. Specifically, alimony is not considered earned income, child support is not considered earned income, and investment income is not considered earned income for the purpose of Traditional IRA contributions.

If a client accidentally overfunds their account, the IRS applies friction: excess contributions to an IRA are subject to a 6 percent annual penalty tax until the excess is removed.

However, the tax code recognizes that older individuals have less time for their capital to compound. Therefore, catch-up contributions allow individuals aged 50 and older to contribute an additional amount to an IRA above the standard annual limit.

Accessing Traditional IRA Capital: Penalties and RMDs

The IRS defers taxes on Traditional IRAs with the strict expectation that the money is used for retirement. Traditional IRA distributions made before the account owner reaches age 59.5 are generally subject to a 10 percent early withdrawal penalty.

But there are logical exemptions. The 10 percent early withdrawal penalty for Traditional IRAs is waived for:

- First-time home purchases, up to a 10,000 dollar lifetime limit.

- Qualified higher education expenses.

- In the event of the death or disability of the account owner.

Eventually, the IRS demands its deferred tax revenue. The SECURE 2.0 Act raised the required minimum distribution (RMD) age for Traditional IRAs to 73 starting in the year 2023. If your client forgets to take this withdrawal, the penalty is severe: the standard penalty for failing to take a required minimum distribution (RMD) from a Traditional IRA is 25 percent of the shortfall amount. However, the IRS offers a grace mechanism—the required minimum distribution (RMD) penalty can be reduced to 10 percent if the shortfall is corrected within a specific correction window.

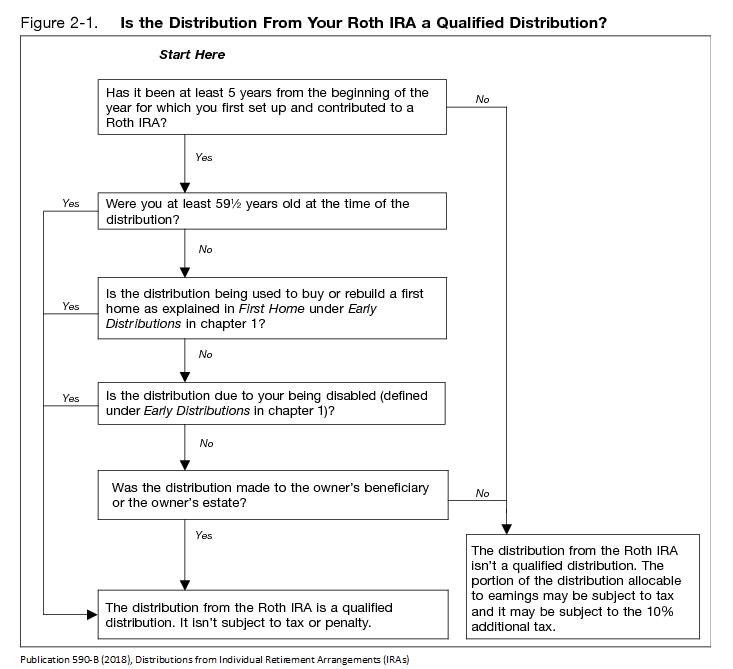

The Roth IRA: The After-Tax Vault

The Roth IRA flips the physics of the Traditional IRA. Contributions to a Roth IRA are always made with after-tax dollars, meaning they are never tax-deductible. Because the IRS gets paid upfront, the back-end benefits are massive: qualified distributions from a Roth IRA are completely tax-free at the federal level.

Furthermore, because the IRS has already collected taxes on the seed money, Roth IRAs do not require the original account owner to take required minimum distributions (RMDs) at any age.

However, this environment is restrictive:

- High-income earners are prohibited from contributing directly to a Roth IRA based on modified adjusted gross income (MAGI) limits.

- To unlock tax-free earnings, the distribution must be qualified. A Roth IRA distribution is considered qualified only if the specific account has been open for at least five consecutive years and meets the age requirement for being qualified, which means the account owner is at least 59.5 years old.

Clients change jobs and banks constantly. Moving retirement money safely is a core day-to-day reality for a registered representative. There are two distinct mechanisms for moving this capital, and confusing them will trigger catastrophic tax bills for your clients.

Trustee-to-Trustee Transfers

A trustee-to-trustee transfer moves retirement assets directly between financial institutions without the account owner taking possession. Because the client never touches the money, there is no risk of them spending it. Thus, there is no limit on the number of trustee-to-trustee transfers an individual can perform in a single calendar year. This is always the preferred method.

Rollovers

A rollover occurs when an individual takes personal possession of retirement funds and subsequently deposits them into another qualified plan. The IRS views personal possession as highly suspicious. Therefore:

- An IRA rollover must be completed within 60 days of the initial withdrawal to avoid taxes and penalties.

- An individual is limited to performing exactly one IRA rollover per 12-month period.

- The Withholding Trap: Employers are required to withhold 20 percent for taxes if a distribution from an employer-sponsored plan is paid directly to the employee instead of being processed as a direct rollover. The client must make up that 20 percent out of their own pocket within 60 days to complete the rollover, or the withheld amount is treated as a taxable distribution.

Before 1974, private pensions frequently collapsed, leaving workers with nothing. To fix this, Congress created the Employee Retirement Income Security Act (ERISA), a federal law establishing minimum standards for retirement and health plans in private industry.

Notice the specific jurisdiction: ERISA applies to private industry. ERISA regulations do not apply to government employer retirement plans, and ERISA regulations do not apply to municipal employer retirement plans.

ERISA Eligibility and Protection

If a private employer offers a qualified plan, they cannot discriminate against rank-and-file workers. ERISA requires private-sector employer plans to allow participation by employees who are at least 21 years old and who have completed at least one year of service. A year of service under ERISA guidelines is strictly defined as 1,000 hours of work during a 12-month period.

Fiduciary Duty and the 404(c) Safe Harbor

ERISA requires plan fiduciaries to manage plan assets solely in the interest of the plan participants and beneficiaries. Furthermore, employers must provide plan participants with a Summary Plan Description detailing the plan's features and funding mechanisms under ERISA guidelines.

But what if the stock market crashes and employees lose their retirement savings? Can they sue the employer? They can, unless the employer utilizes the ERISA Section 404(c) Safe Harbor provision, which protects employers from fiduciary liability for investment losses if employees are allowed to direct their own investments.

To qualify for the ERISA Safe Harbor provision, an employer must offer at least three different investment alternatives with materially varying risk and return characteristics (e.g., a money market fund, a bond fund, and an equity growth fund).

Employer plans split into two fundamental architectures regarding who shoulders the investment risk.

| Feature | Defined Benefit Plan | Defined Contribution Plan |

|---|---|---|

| Core Concept | Promises a specific monthly payout at retirement based on variables like salary, age, and years of service. | Specifies the amount the employer will contribute to the plan on an ongoing basis without guaranteeing a specific retirement payout. |

| Risk Bearer | The employer bears all investment risk. | The employee bears all investment risk. |

| Mechanism | Requires the services of an actuary to calculate necessary annual employer funding contributions. | The ultimate retirement benefit depends entirely on the performance of the chosen investments over time. |

As a representative, you will encounter various tax codes used as shorthand for different employer plans. You must match the plan to the specific type of employer.

Corporate and Private Sector Plans

- 401(k) Plan: Allows eligible employees to make pre-tax elective deferrals directly from their salary into a defined contribution retirement account.

- Profit-Sharing Plans: These are highly flexible for the employer. Profit-sharing plans legally allow employers to skip contributions during years of low corporate profitability. However, when contributions are made, they must be allocated among participating employees based on a predetermined and non-discriminatory formula.

Specialized Entity Plans

- 403(b) Plan: A tax-advantaged retirement plan exclusively available for public school employees and employees of 501(c)(3) tax-exempt organizations (like charities and churches). Due to their historical structure, 403(b) retirement plans are commonly referred to as Tax-Sheltered Annuities (TSAs).

- 457 Plan: A non-qualified deferred compensation plan primarily designed for state and local government employees.

Small Business and Self-Employed Plans

- Keogh Plans: Qualified retirement plans designed specifically for self-employed individuals and unincorporated businesses. You will frequently see them tested under their alternative name: Keogh retirement plans are also formally known as HR-10 plans.

- Simplified Employee Pension (SEP) IRA: This allows employers to make direct, tax-deductible contributions to an employee's traditional IRA. Crucially, in a SEP IRA, only the employer is permitted to make funding contributions.

- SIMPLE IRA (Savings Incentive Match Plan for Employees): This plan is available exclusively to small businesses employing 100 or fewer employees.

Securing capital for higher education operates on similar principles to retirement savings. The Series 7 heavily tests the contrast between the highly flexible 529 plan and the highly restrictive Coverdell ESA.

The 529 Plan: The Heavy Hauler

A 529 plan is a state-sponsored municipal fund security specifically designed to save for future education costs. Because it is municipal in nature, the rules are highly favorable to the donor:

- Contributions to a 529 plan are strictly made with after-tax dollars.

- Earnings accumulated within a 529 plan grow on a tax-deferred basis at the federal level.

- Withdrawals from a 529 plan are entirely tax-free at the federal level when the funds are used for qualified education expenses.

- Flexibility is key: up to 10,000 dollars per year can be withdrawn tax-free from a 529 plan to pay for elementary or secondary school tuition expenses.

- Control: The donor maintains complete legal control over a 529 plan and has the authority to change the designated beneficiary to another family member.

- Funding Power: To accelerate compound growth, 529 plans allow a contributor to front-load up to five years' worth of the annual gift tax exclusion in a single lump sum without incurring immediate gift taxes.

The Coverdell Education Savings Account (ESA): The Delicate Tool

In stark contrast to the massive capacity of a 529 plan, a Coverdell Education Savings Account (ESA) is highly restrictive.

- It enforces a strict maximum annual contribution limit of 2,000 dollars per designated beneficiary.

- Just like a 529, contributions made to a Coverdell Education Savings Account are not tax-deductible.

- Coverdell Education Savings Account contribution limits are phased out and ultimately eliminated for high-income earners.

- The Clock is Ticking: All new contributions to a Coverdell Education Savings Account must permanently cease when the beneficiary reaches age 18. Furthermore, the funds held in a Coverdell Education Savings Account must be fully distributed or rolled over to another beneficiary by the time the original beneficiary reaches age 30.

Why this matters for your daily practice: When a client's child turns 17, and the client receives an inheritance they want to dedicate to education, you instantly know a Coverdell is functionally useless due to the age cutoff and the 2,000 dollar limit. You will immediately direct them to a 529 plan, utilizing the 5-year front-loading provision to shelter the capital. Understanding these structural boundaries isn't just about passing the Series 7—it is the exact mechanism by which you provide value and protect your clients' wealth.