Anti-Money Laundering (AML)

Consider a counterfeiter attempting to purchase a commercial building with a duffel bag full of illicit hundred-dollar bills. A reputable seller will instantly recognize the fraud or, at the very least, refuse the suspicious physical cash. However, if that same criminal can slowly trickle the illicit cash into a legitimate banking account and then wire the funds to the seller, the money is accepted without question. The funds have been "washed" through institutional plumbing.

This mechanism is the essence of money laundering: the process of disguising the illegal origin of financial proceeds to make the funds appear entirely legitimate. As a prospective securities professional, your daily interactions with client accounts, deposits, and wire transfers place you on the frontline. You are not merely processing paperwork; you are guarding the gates of the global financial system against cartels, terrorists, and organized crime syndicates.

Criminals cannot simply deposit $1 million in illicit drug proceeds at a bank teller's window without triggering immediate alarms. Instead, they must execute a deliberate, three-stage choreography to sanitize their capital. The three traditional stages of money laundering are placement, layering, and integration.

- Placement: This is the first stage of money laundering, involving the physical entry of illicit cash into the financial system. Because physical currency is bulky and suspicious, placement is the most perilous stage for a criminal.

- Layering: Once the funds are inside the banking system, the layering phase begins. Layering is the second stage of money laundering, involving complex financial transactions designed to obscure the source of the illicit funds. A criminal might wire money between multiple international shell companies, buy and sell securities, or purchase high-end assets to create a dizzying audit trail that investigators struggle to follow.

- Integration: This is the final stage of money laundering, where the illegal funds are reintroduced into the legitimate economy. The criminal now has access to "clean" money, which can be legally taxed and spent on legitimate investments, businesses, or real estate without raising suspicion.

Evading the Radar: Structuring and Smurfing

Because a massive cash deposit during the Placement phase is easily detected, criminals rely on a tactic known as structuring. Structuring occurs when an individual intentionally breaks large cash transactions into smaller amounts to evade regulatory reporting thresholds.

Example: If a regulatory threshold requires reporting on cash transactions over $10,000, a criminal holding $25,000 might make three separate deposits of $8,000, $8,500, and $8,500 over several days.

When a criminal enterprise scales this operation up, they often use smurfing. Smurfing is a specific type of structuring involving multiple individuals (the "smurfs") making small deposits on behalf of a single entity. They spread out across different bank branches and institutions on the same day, depositing small amounts of cash into various accounts that eventually funnel back to the ringleader.

The United States has built a robust legal framework to detect and prosecute these maneuvers, leaning heavily on the cooperation of financial institutions.

The foundational bedrock is the Bank Secrecy Act (BSA). Enacted in 1970, the Bank Secrecy Act is the primary US federal law establishing anti-money laundering (AML) reporting and recordkeeping requirements for financial institutions.

However, following the terrorist attacks of September 11, 2001, the US government drastically strengthened the BSA. The USA PATRIOT Act was passed, taking a massive step forward by mandating that all broker-dealers establish formalized, internal anti-money laundering compliance programs. It fundamentally shifted the burden: firms could no longer just react to regulators; they had to proactively hunt for illicit activity within their own walls.

To comply with the USA PATRIOT Act, broker-dealers must build and maintain a rigorous AML compliance program. The regulators do not provide a one-size-fits-all checklist; the program must be tailored to the specific risks of the firm's business model. However, there are rigid structural requirements:

- Senior Management Approval: A broker-dealer's anti-money laundering compliance program must be approved in writing by a member of senior management. This ensures accountability at the executive level.

- Designated Leadership: FINRA Rule 3310 requires member firms to designate an anti-money laundering compliance officer to manage the program. Furthermore, broker-dealers must provide FINRA with the name and contact information for this firm's designated AML compliance officer.

- Ongoing Education: The rules recognize that human awareness is the best defense. Therefore, an AML compliance program must include an ongoing training program for appropriate personnel. (Not every employee needs the exact same training; it is tailored to those who handle accounts and transactions.)

- Annual Verification: You cannot grade your own homework. Broker-dealers must subject the firm's anti-money laundering compliance program to independent testing on an annual basis to ensure it actually works.

- Internal Nature: Interestingly, while firms must have these programs, broker-dealers are not required to file internal anti-money laundering compliance programs with FINRA or the Securities and Exchange Commission (SEC). The regulators will inspect the program during routine audits, but the manual remains an internal firm document.

Before a broker-dealer can monitor a customer's behavior, the firm must verify who the customer actually is.

The Customer Identification Program (CIP)

Broker-dealers must implement a Customer Identification Program (CIP) to verify the identity of any person opening a new account. At an absolute minimum, a CIP requires a firm to collect a customer's:

- Name

- Date of birth

- Physical address (not just a P.O. Box)

- Tax identification number (such as a Social Security Number)

This data must be collected prior to account opening.

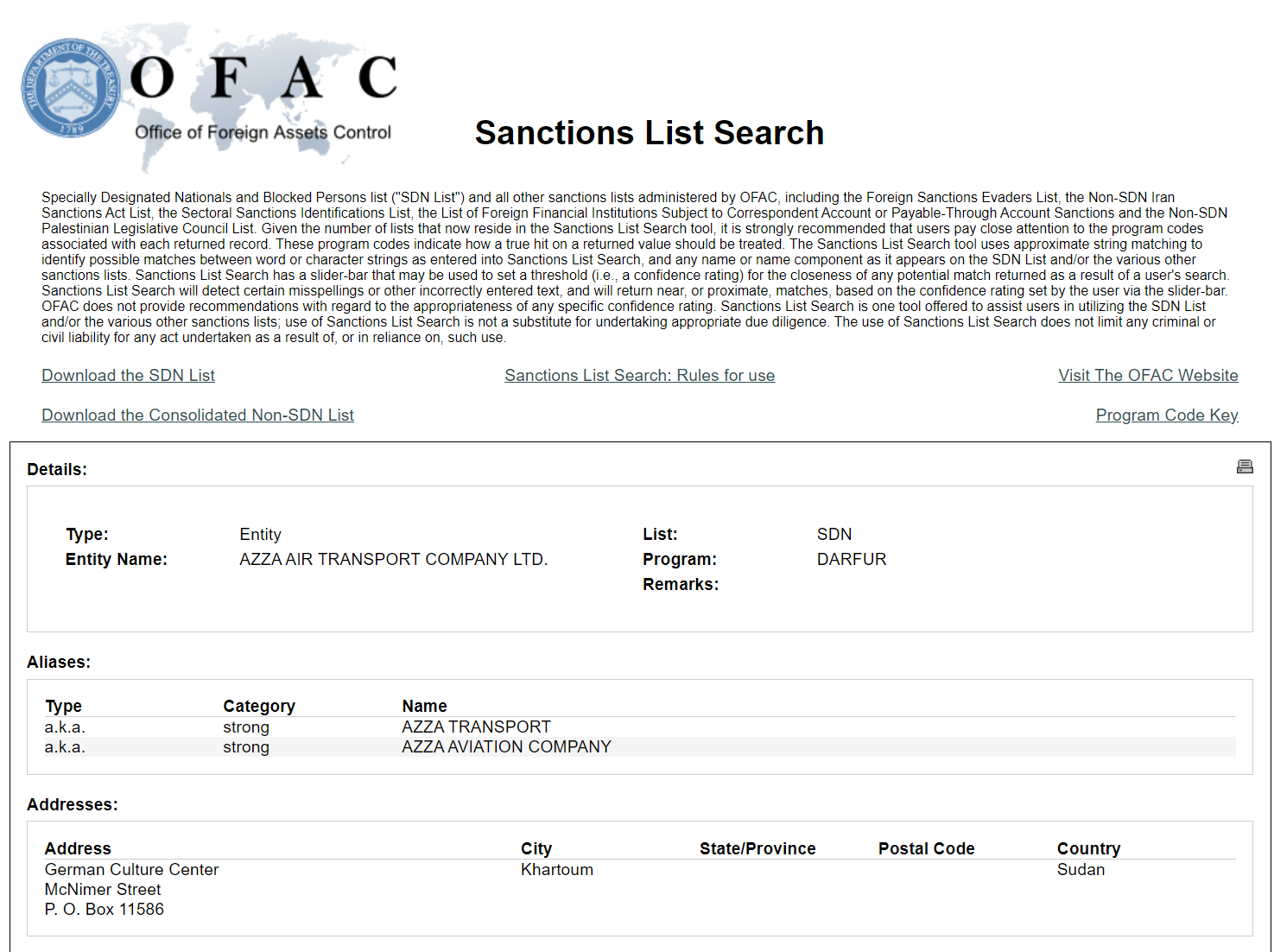

The Office of Foreign Assets Control (OFAC)

Identifying a customer is only half the battle; the firm must ensure they are legally allowed to do business with that person.

The Office of Foreign Assets Control (OFAC) is a division of the US Treasury Department that administers and enforces economic and trade sanctions. OFAC targets hostile foreign nations, terrorists, international narcotics traffickers, and entities involved in the proliferation of weapons of mass destruction.

To do this, OFAC maintains the Specially Designated Nationals and Blocked Persons List (SDN List).

The Absolute Prohibition: US persons and businesses are legally prohibited from conducting financial transactions with individuals or entities on the Specially Designated Nationals List.

Firms must verify the names of new customers against the Specially Designated Nationals List before opening an account. If a firm identifies an existing customer on the SDN List, or if a new customer attempts a transaction and turns up as a match, the firm cannot simply return the customer's money and say "no thank you."

Instead, a broker-dealer must immediately block the transaction and freeze the account if a customer is identified on the Specially Designated Nationals List. Once the assets are frozen, broker-dealers must report these blocked assets to the Office of Foreign Assets Control within 10 business days of the blocking event.

If OFAC is the enforcer of international sanctions, who analyzes the domestic transaction data to catch money laundering?

That responsibility falls to the Financial Crimes Enforcement Network (FinCEN). Like OFAC, FinCEN is a bureau of the US Department of the Treasury. FinCEN collects and analyzes information about financial transactions to combat domestic and international money laundering.

Broker-dealers serve as FinCEN's eyes and ears by submitting mandatory intelligence reports based on specific dollar thresholds and suspicious behaviors.

Currency Transaction Reports (CTR)

A Currency Transaction Report (CTR) is used to track the physical placement of large amounts of cash. A CTR must be filed with FinCEN for any cash transaction exceeding $10,000 executed by a single customer in one business day.

Remember the concept of structuring? To prevent a customer from dodging the $10,000 threshold by dropping off $4,000 in the morning, $4,000 at lunch, and $3,000 in the afternoon, financial institutions must aggregate multiple cash transactions by the same customer on the same day to determine if the Currency Transaction Report threshold is met.

- Deadline: A CTR must be filed within 15 calendar days of the qualifying cash transaction.

Suspicious Activity Reports (SAR)

While CTRs are purely objective (based strictly on a mathematical cash threshold), Suspicious Activity Reports (SARs) require professional judgment.

A SAR must be filed with FinCEN for questionable transactions involving $5,000 or more in funds or other assets. "Questionable" means the transaction lacks a reasonable business purpose, seems designed to evade rules, or is uncharacteristic for that specific client.

- Deadline: A SAR must be filed within 30 calendar days of a firm becoming aware of the suspicious transaction.

- Extension: The deadline to file a SAR is extended to 60 days if a firm knows a suspicious transaction occurred but cannot immediately identify a specific suspect.

Crucial Rule on Non-Disclosure: Financial institutions and associated employees are legally prohibited from disclosing the filing of a Suspicious Activity Report to the subject of the report. If a customer is under investigation via a SAR, tipping them off is a severe federal offense.

The BSA Travel Rule

Finally, the regulators want to ensure that illicit funds cannot be zapped across the globe anonymously. The Bank Secrecy Act travel rule requires financial institutions to collect and retain specific information about the sender and recipient for wire transfers of $3,000 or more. When the money "travels," the data must travel with it.

Summary of Critical Reporting Timelines and Thresholds

| Rule / Report | Agency | Trigger Threshold | Filing / Reporting Deadline | Key Detail |

|---|---|---|---|---|

| CTR | FinCEN | > $10,000 in physical cash in one business day | 15 calendar days | Must aggregate multiple same-day cash deposits by one customer. |

| SAR | FinCEN | $5,000+ in funds/assets (suspicious activity) | 30 calendar days (60 if no suspect) | Strictly prohibited from tipping off the subject. |

| OFAC / SDN | OFAC | Customer matches the SDN List | 10 business days | Must immediately block the transaction and freeze the account. |

| Travel Rule | - | $3,000+ (Wire transfers) | N/A (Recordkeeping rule) | Sender and recipient info must be retained. |

Understanding these mechanics goes far beyond passing the SIE exam. Whenever you process a wire, verify a new client's physical address, or escalate a transaction that "just doesn't look right," you are operating the very machinery that keeps our financial system transparent, solvent, and safe.