Customer Account Registrations

When a client hands you their life savings, they are not merely opening a receptacle for their cash; they are establishing a legally binding architecture for their property. As a registered representative, your first duty is to understand how this architecture dictates control, taxation, and inheritance. If you assign the wrong account type, you might accidentally subject a family to a brutal probate process, incur massive tax penalties, or violate federal law. We must study account registrations not as bureaucratic paperwork, but as the fundamental physics of ownership in the financial system.

Every financial account requires a precise answer to three questions: Who can trade? Who receives the money? What happens when the owner dies?

The Individual Account

An individual account is the simplest structure. It is owned by a single person who has sole trading authority over the assets. When that owner dies, the assets in a standard individual account pass directly to the owner's estate.

Passing to an estate means the assets are subject to probate—a public, often lengthy, and expensive legal process where a court validates a will and distributes assets. However, a client can attach a mechanism to bypass this friction. A Transfer on Death (TOD) designation allows an individual account owner to name specific beneficiaries to receive the account assets upon the owner's death.

Why this matters: A TOD designation allows account assets to legally bypass the probate process entirely, transferring directly to the beneficiary. But do not confuse probate with taxation. Assets passing to a beneficiary through a TOD designation remain subject to estate taxes. The TOD changes the legal transfer mechanism, not the tax liability.

If a client wishes to maintain personal anonymity for security or privacy reasons, they can open a brokerage account identified only by a number or symbol. However, Wall Street is not a Swiss bank movie trope. Opening a numbered or symbol account strictly requires the customer to provide the broker-dealer with a written statement legally acknowledging ownership of the account.

Joint Accounts

When multiple people share an account, the dynamics of control shift. Opening a joint account requires the signatures of all joint account owners. Yet, for day-to-day operations, the system is designed for fluidity: any single owner of a joint account has the authority to initiate trades within the account, and any single owner has the authority to request distributions.

Here is the vital safeguard: while one person can ask for the money, the firm cannot hand it exclusively to them. Distributions from a joint account must be made payable to all joint owners, and checks issued from a joint account must be mailed to the primary address registered on the joint account.

The critical difference between joint account types revolves around what happens when an owner dies.

| Account Type | Ownership Split | What happens at death? | Probate Status |

|---|---|---|---|

| Joint Tenants with Right of Survivorship (JTWROS) | All owners hold an equal and undivided interest in the account assets. | The deceased owner's share automatically passes to the surviving account owners. | Bypasses the probate process. |

| Tenants in Common (TIC) | Owners can hold unequal fractional ownership interests (e.g., 70/30 split). | The deceased owner's share passes to the deceased owner's estate. | Subject to the probate process. |

Often, the person making the trades is not the ultimate owner of the assets. In these fiduciary relationships relationships, you must always look for the underlying legal document granting authority.

Business Accounts

Corporations and partnerships are legal entities, but entities cannot pick up a phone to place a trade—people do.

- Corporate Accounts: Opening a corporate brokerage account requires a corporate resolution to formally identify the individuals authorized to trade on behalf of the corporation. If the corporation wants to trade on margin (borrowing money to buy securities), it additionally requires a corporate charter confirming the corporation is legally permitted to borrow on margin.

- Partnership Accounts: Opening a partnership account requires a formal partnership agreement. This agreement specifies which individual partners have the legal authority to execute trades on behalf of the partnership.

Trust Accounts

A trust account is a legal arrangement managed by a designated trustee for the benefit of one or more beneficiaries. The trustee acts as a fiduciary and must manage the assets strictly according to the terms set forth in the trust agreement.

- A revocable trust allows the creator (the grantor) of the trust to alter or cancel the trust at any time during their lifetime.

- An irrevocable trust cannot be easily altered or canceled by the creator once the trust has been established, which often provides different tax and asset-protection benefits.

Custodial Accounts (UGMA and UTMA)

Minors cannot legally enter into binding financial contracts. A custodial account solves this by allowing an adult to manage financial assets for a minor until the minor reaches the age of majority.

The structure of these accounts is rigid to protect the child:

- A custodial account is strictly limited to one custodian and one minor beneficiary. You cannot open a single account for three siblings.

- Contributions made to a Uniform Gifts to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA) account constitute irrevocable gifts. The donor cannot take the money back.

- The accounts are registered under the minor's Social Security Number. Consequently, taxes on the investment earnings are the legal responsibility of the minor, not the custodian.

- Because fiduciaries cannot take reckless risks with a child's money, margin trading is strictly prohibited in UGMA and UTMA custodial accounts.

- Control of the account automatically transfers from the custodian to the beneficiary when the beneficiary reaches the age of majority specified by state law.

UGMA vs. UTMA: What can they hold?

- UGMA accounts are limited to holding financial assets like cash, stocks, bonds, and mutual funds.

- UTMA accounts can hold a wider variety of asset classes. Notably, UTMA accounts are legally permitted to hold physical real estate and fine art.

Discretionary Accounts

What if a customer wants you, the registered representative, to trade on their behalf?

A discretionary account allows a registered representative to execute trades without receiving prior approval from the customer for each individual transaction. Because this is an immense transfer of power, it requires strict oversight:

- Establishing a discretionary account requires prior written authorization from the account-holding customer.

- Discretionary trading authority requires approval from a registered principal (your manager) before the first discretionary trade is executed.

The 3 A's of Discretion: A registered representative exercises discretionary authority if they choose the specific security (Asset), the transaction size (Amount), or whether to buy or sell (Action). Conversely, a registered representative choosing only the time or the price of a trade does not constitute the use of discretionary authority.

The U.S. government offers tax incentives to encourage citizens to save for retirement. Understanding the mechanics of Individual Retirement Accounts (IRAs) and corporate plans is essential, as millions of Americans rely on them.

Traditional IRAs: The Upfront Deduction

A Traditional Individual Retirement Account (IRA) is a personal tax-advantaged account that allows eligible individuals to make pre-tax, tax-deductible contributions. To participate, an individual must have documented earned income (wages, salaries, bonuses—not passive investment income). Under the SECURE Act, the government eliminated the maximum age restriction for making new contributions to a Traditional IRA. Additionally, to help older workers accelerate their savings, individuals aged 50 and older are legally permitted to make additional annual "catch-up" contributions.

Once inside the Traditional IRA, investment earnings grow on a tax-deferred basis. You pay no taxes on capital gains or dividends year-to-year.

However, the IRS eventually demands its cut. Because the money went in pre-tax, distributions taken from a Traditional IRA are taxed as ordinary income in the year they are withdrawn.

If you take money out too early, the IRS punishes you. Withdrawals made from a Traditional IRA before the account owner reaches age 59.5 are generally subject to a 10 percent early withdrawal penalty. This 10 percent penalty is waived only for specific IRS exceptions, such as first-time home purchases or qualified higher education expenses.

Conversely, if you leave the money in too long, the IRS forces your hand. Required Minimum Distributions (RMDs) mandate that Traditional IRA owners must begin withdrawing minimum specified amounts from their accounts by a statutory age. Recently, under the SECURE 2.0 Act, the starting age for RMDs from a Traditional IRA was raised to age 73.

Roth IRAs: The Back-End Reward

A Roth Individual Retirement Account (IRA) flips the traditional tax logic upside down.

Contributions to a Roth IRA are made exclusively with after-tax dollars, meaning contributions do not provide an upfront tax deduction for the contributor. However, the immense benefit comes later: qualified distributions taken from a Roth IRA are completely free from federal income tax.

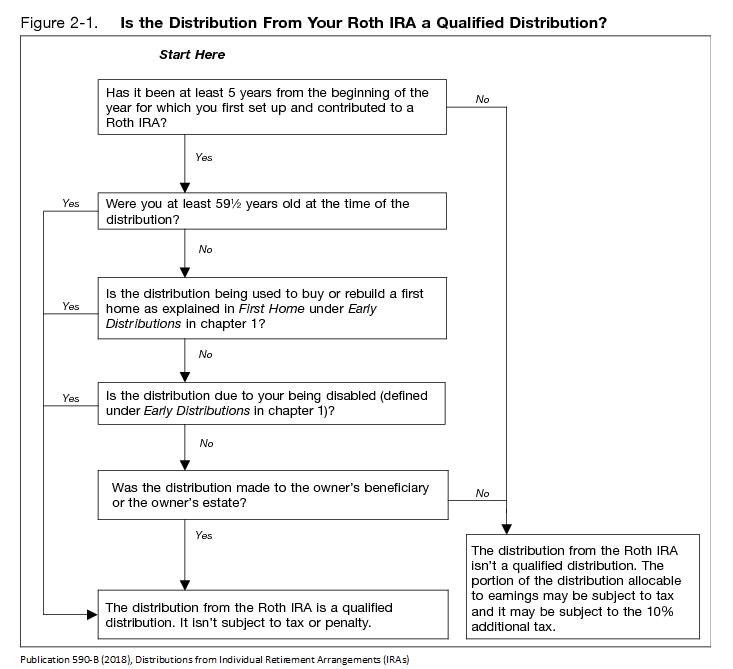

To earn this tax-free status, the distribution must be "qualified." This requires two conditions to be met simultaneously:

- The Roth IRA must have been open for a minimum of five continuous years.

- The Roth IRA owner must be at least 59.5 years old (or meet another specific qualifying condition such as death or disability).

Because the IRS already taxed the seed money, Roth IRAs enjoy two massive structural advantages over Traditional IRAs. First, Roth IRAs are exempt from Required Minimum Distributions (RMDs) during the original account owner's lifetime. Second, high earners are locked out; eligibility to contribute to a Roth IRA is phased out for individuals whose modified adjusted gross income exceeds certain IRS limits.

Corporate Retirement Plans (ERISA)

When employers sponsor retirement plans, they fall under the jurisdiction of the Employee Retirement Income Security Act (ERISA). ERISA establishes federal guidelines to protect employees participating in private-sector retirement plans.

To maintain their tax-advantaged "qualified" status, these corporate retirement plans must satisfy minimum participant standards established by ERISA. Crucially, they must strictly adhere to non-discrimination rules to ensure the plan does not unfairly favor highly compensated employees (executives) over rank-and-file workers. Like Traditional IRAs, Required Minimum Distributions (RMDs) rules apply to all qualified corporate retirement plans.

Contributions made by an employee to a qualified corporate retirement plan are typically deducted from payroll with pre-tax dollars, and the investment earnings accumulating within the plan grow on a tax-deferred basis.

There are two primary types of employer plans, defined entirely by who bears the risk:

1. Defined Benefit Plans A defined benefit plan (traditionally known as a pension) guarantees an employee a specific retirement payout based on a set formula involving salary history and total years of service. In a defined benefit corporate retirement plan, the sponsoring employer assumes all the investment risk associated with funding the required payouts.

2. Defined Contribution Plans In a defined contribution corporate retirement plan, the individual employee assumes the investment risk associated with the account's performance. The payout at retirement depends entirely on how much was contributed and how well the investments performed.

- A 401(k) plan is a specific type of defined contribution qualified retirement plan sponsored by a for-profit corporate employer.

- A 403(b) plan is a tax-advantaged defined contribution retirement plan specifically designed for employees of public schools and certain tax-exempt organizations (like charities and hospitals).

The Rollover Mechanism

When an employee leaves a job, they don't have to leave their retirement savings behind. An individual can legally transfer funds from an employer-sponsored retirement plan directly into an Individual Retirement Account (IRA) through a process known as a rollover.

If the firm sends the check directly to the new IRA custodian, it is a direct rollover and poses no tax risk. However, if the firm cuts the check to the employee to deposit themselves, it triggers an indirect rollover. An indirect retirement account rollover must be completed within 60 days of receiving the funds to successfully avoid early withdrawal tax penalties. Miss that 60-day window by even 24 hours, and the IRS will treat the entire balance as a taxable distribution, complete with early withdrawal penalties. Physics—and tax law—are entirely unforgiving of delays.