Insider Trading and Other Prohibited Activities

Imagine a casino where one player knows the exact sequence of cards remaining in the dealer’s shoe. No one else would willingly sit at that table, and the casino would inevitably collapse. Capital markets operate on a similar, highly fragile premise: investors risk their capital because they believe the underlying mechanics are fair. When financial professionals exploit their access—whether by trading on corporate secrets, hoarding lucrative new stock issues, or manipulating market prices—they destroy the trust that makes global finance possible. Your role as a registered representative is to act as a steward of that trust. The regulations governing prohibited activities are not bureaucratic red tape; they are the structural foundation of market integrity.

At the core of market fairness is the principle that no participant should have an unfair, insurmountable informational advantage. Insider trading is the act of trading a security based on material nonpublic information.

To understand the violation, we must dissect the definition:

Material information is any data that a reasonable investor would consider important when making an investment decision. This could be an impending merger, a catastrophic earnings miss, or the sudden resignation of a CEO.

Nonpublic information is data that has not yet been broadly distributed to the general investing public.

When you combine these two, you have a potent, illegal advantage. To curb this, Congress passed the Insider Trading and Securities Fraud Enforcement Act of 1988, which established severe civil and criminal penalties for insider trading.

The Mechanics of Liability

Insider trading requires a flow of information, which creates two distinct types of liability:

- Tipper liability holds the person sharing the material nonpublic information legally responsible for insider trading. However, a crucial legal standard applies: a tipper must have breached a fiduciary duty for insider trading liability to exist.

- Tippee liability holds the person who actually executes the trade on material nonpublic information legally responsible.

If a corporate insider breaches their duty of trust by leaking a forthcoming earnings report to a friend, and that friend buys options based on the tip, both the tipper and the tippee have committed insider trading.

The Hammer: Penalties and Enforcement

The regulatory hammer for insider trading is designed to be devastating enough to eliminate the temptation.

Civil Penalties: Civil penalties for insider trading can reach up to three times the profit gained from the illegal trade. Alternatively, if the insider sold stock to avoid an impending crash, civil penalties can reach up to three times the loss avoided from the illegal trade. This punitive multiplier is known conceptually as treble damages—a civil penalty allowing courts to fine insider traders up to three times their illicit gains.

Criminal Penalties:

- The maximum criminal fine for an individual convicted of insider trading is $5 million.

- An individual convicted of insider trading can face a maximum criminal prison sentence of 20 years.

- If the violator is an institution, the maximum criminal fine for a corporation convicted of insider trading is $25 million.

To aid enforcement, regulators financially incentivize whistleblowing. Whistleblowers reporting insider trading can receive a bounty of 10% to 30% of the collected civil penalties.

Institutional Defenses: The Chinese Wall

Broker-dealers handle massive amounts of sensitive data daily. Consequently, broker-dealers must establish and enforce written supervisory procedures to prevent the misuse of material nonpublic information.

The primary structural defense is an information barrier—a broker-dealer policy designed to stop the flow of material nonpublic information between internal departments. For instance, if a firm's investment banking wing is underwriting a secret acquisition, that data cannot cross over to the retail trading desk. Historically and commonly within the industry, these information barriers within a broker-dealer are referred to as Chinese Walls.

When a highly anticipated company goes public, the demand for its stock vastly outweighs the supply. If financial insiders were allowed to buy up all these hot shares, the public would be left fighting over table scraps in the secondary market.

To ensure fairness, FINRA Rule 5130 prohibits broker-dealers and associated persons from buying initial public offering (IPO) shares of equity securities.

Who is a Restricted Person?

The rule explicitly designates certain entities and individuals as "restricted."

- Member firms are defined as restricted persons.

- Employees of member firms are defined as restricted persons.

- Immediate family members of member firm employees are defined as restricted persons.

- Furthermore, any individual residing in the same household as a restricted person is classified as a restricted person under FINRA Rule 5130, regardless of their relation.

FINRA’s definition of "immediate family" is highly specific. You must know exactly where the boundary is drawn.

| Classified as Immediate Family (Restricted) | Excluded from Immediate Family (Not Restricted) |

|---|---|

| Spouses | Aunts |

| Children | Uncles |

| Parents | Grandparents |

| Siblings | |

| In-laws |

Exemptions to Rule 5130

Rule 5130 is strictly calibrated to prevent insiders from hoarding equities at their genesis. Therefore:

- FINRA Rule 5130 strictly limits restrictions to the purchase of new issues of common stock.

- Associated persons are permitted to purchase secondary market offerings without violating the rule.

- Associated persons are permitted to purchase initial public offerings of debt securities without violating the rule.

There is also a mathematical exemption: the anti-dilution provision. A restricted person can buy IPO shares to prevent ownership dilution if the restricted person already holds an equity interest in the issuer prior to the public offering.

When a customer opens a brokerage account, they entrust their capital to your firm. FINRA strictly prohibits the unauthorized use of customer funds and strictly prohibits the unauthorized use of customer securities.

One of the cardinal sins in this realm is commingling—the prohibited practice of mixing customer assets with the broker-dealer's proprietary assets. Customer assets must be segregated to protect them in the event the broker-dealer faces insolvency.

Borrowing and Lending Money

The relationship between a registered representative and a client is inherently asymmetrical. Because of this power dynamic, registered representatives are generally prohibited from borrowing money from customers, and similarly prohibited from lending money to customers.

However, life is nuanced, and FINRA allows for strictly defined exceptions.

Exceptions requiring NO broker-dealer approval:

- A registered representative may borrow money from a customer who is an immediate family member.

- A registered representative may borrow money from a financial institution customer regularly engaged in the lending business (e.g., your client is a commercial bank, and you get a standard mortgage).

Exceptions requiring PRIOR WRITTEN APPROVAL from the member firm:

- Borrowing money from a customer based on an outside personal relationship (e.g., a lifelong friend who later became your client).

- Borrowing money from a customer based on an outside business relationship (e.g., you and your client co-own a local real estate venture).

Sharing in Customer Accounts and Guarantees

You are an advisor, not a co-owner of your client's financial destiny. Sharing in the profits and losses of a customer's account requires two critical prerequisites:

- Prior written authorization from the customer.

- Prior written authorization from the employing broker-dealer.

Even with permission, a registered representative's share of profits and losses in a customer account must be proportionate to the registered representative's financial contribution to the account. Note: The proportionate sharing rule for customer accounts does not apply if the account belongs to an immediate family member.

Finally, markets inherently carry risk. Attempting to insulate a client from reality by guaranteeing a customer against a loss in a securities account is strictly prohibited under all circumstances.

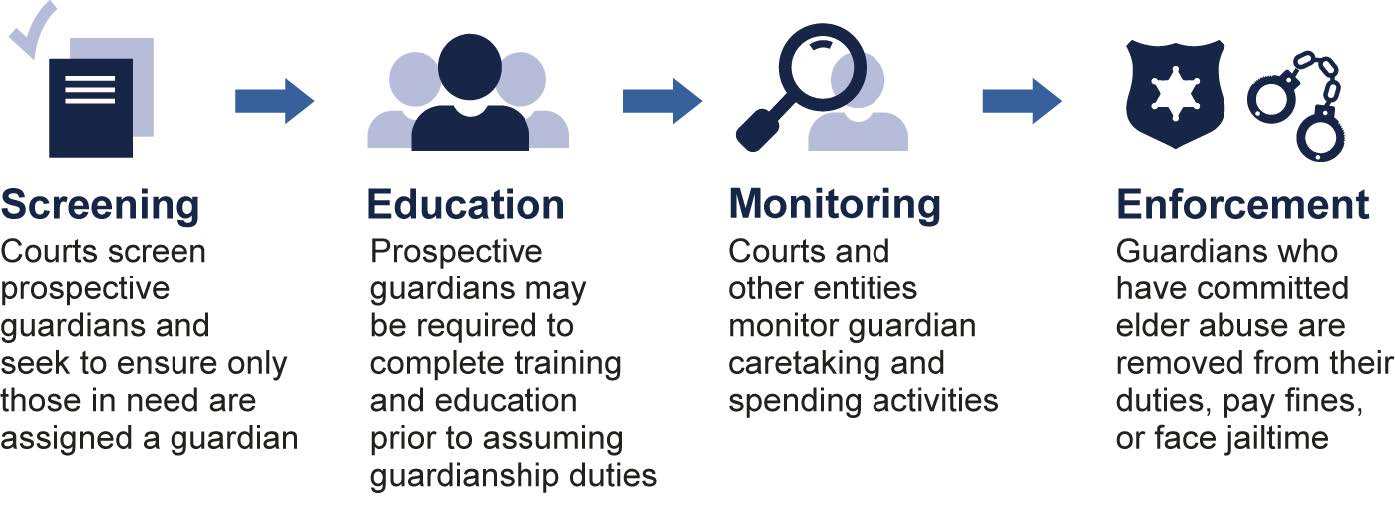

Financial professionals are uniquely positioned to spot cognitive decline or elder abuse before anyone else. FINRA Rule 2165 provides a vital defense mechanism, granting member firms the authority to place temporary holds on accounts when financial exploitation is suspected.

Critically, this rule grants the authority to place temporary holds on three distinct activities:

- Disbursements of funds.

- Disbursements of securities.

- Securities transactions.

Who is Protected?

The rule specifically protects a specified adult, defined as:

- Any person age 65 or older.

- Any person age 18 or older with a reasonably believed mental or physical impairment that limits their ability to protect their own interests.

The Timeline of a Hold

When a firm hits the brakes, the clock starts ticking:

- The initial temporary hold on an account can last for up to 15 business days.

- A temporary hold can be extended for 10 additional business days if an internal review confirms suspected financial exploitation.

- A temporary hold can be extended for an additional 30 business days if the firm has reported the matter to a state authority (like Adult Protective Services).

To assist in these emergencies, member firms must make a reasonable effort to obtain the name of a trusted contact person for retail customer accounts. The trusted contact person is intended to be a resource for the member firm when responding to suspected financial exploitation—acting as an emergency circuit breaker to verify the client's well-being.

In a highly regulated industry, the paperwork is the reality. Falsifying or altering customer documents is a strict violation of FINRA rules, as it completely destroys the audit trail regulators rely upon.

Two specific violations frequently trap careless representatives:

- Forgery is the prohibited act of signing another person's name on a document without that person's explicit authorization.

- A signature of convenience is the prohibited practice of having a customer sign a blank form to be completed by the representative later.

Do not fall into the trap of trying to "save a client time." Using a signature of convenience violates FINRA rules even if the customer grants verbal permission. A signature must always attest to the exact, completed facts on the document at the moment it is signed.

If you manipulate the perceived demand or price of an asset, you are defrauding every other participant in the market.

- Wash trading is the illegal practice of buying and selling the same security to create a false appearance of market activity. Because the trader effectively sells the stock to themselves, there is no real change in beneficial ownership—only the illusion of volume.

- Painting the tape is a similar form of market manipulation involving phantom trades to falsely inflate trading volume, making an asset look artificially liquid or in high demand.

- Front-running is the illegal practice of executing a proprietary trade in an equity security while possessing knowledge of an imminent block customer transaction. If you know a massive institutional buy order is about to drive the price of a stock up, and you buy shares for your own account first, you are stealing the price advantage from your own client.

- False rumors: Associated persons are strictly prohibited from originating or spreading false market rumors to manipulate security prices.

- Free-riding is the prohibited practice of buying a security and selling that security before paying for the initial purchase. A client cannot use the broker-dealer's capital as a free, unauthorized short-term loan to flip a stock for profit without ever actually funding the trade.

As a financial professional, your success must stem from your acumen, your service, and your analytical skill—never from bending the rules of the game. Understanding these prohibitions ensures that the market remains the robust, trustworthy engine of capital it was designed to be.