Offering Documents and Regulatory Filings

Capital markets function on a singular, uncompromising premise: transparency is the prerequisite for public trust. When a corporation decides to raise capital by selling shares to the public, it is essentially asking strangers to part with their wealth in exchange for a piece of an uncertain future. To prevent this process from devolving into a bazaar of empty promises, the Securities Act of 1933 requires all non-exempt securities to be registered with the SEC. To fulfill this mandate, an issuer must file a registration statement, a comprehensive statutory document that discloses material information about a new securities offering to the SEC.

As a future securities professional, you must master the mechanics of this disclosure process. It dictates exactly what you can say to your clients, what documents you must provide them, and precisely when you must deliver them.

Filing a registration statement triggers a highly choreographed timeline designed to protect the investing public from hype and asymmetrical information.

The Quiet Period and the Cooling-Off Period

The moment an issuer files its registration statement, a regulatory clock begins ticking. The SEC review period for a registration statement is known as the cooling-off period. By statute, the cooling-off period lasts for a minimum of 20 days.

During this time, the quiet period limits the public communication an issuer can make surrounding a new offering. Why? Imagine if a CEO filed technical, mundane financial disclosures with the SEC but simultaneously went on television to make wildly optimistic promises about the company’s stock. The quiet period forces the issuer to let the written facts speak for themselves, preventing them from whipping the public into an unjustified frenzy.

Engaging the Market: Red Herrings and Tombstones

If you cannot officially sell the stock yet, how does Wall Street know if anyone actually wants to buy it? The SEC provides specific, highly regulated tools to gauge market demand during the cooling-off period.

An issuer may distribute a preliminary prospectus during the cooling-off period. In the industry, a preliminary prospectus is commonly known as a red herring. This nickname comes from the bold red disclaimer historically printed on the margin of the cover page, warning readers that the registration is not yet effective.

The Red Herring's Purpose: A preliminary prospectus gathers non-binding indications of interest from potential investors. It allows underwriters to build a "book" of potential buyers without violating the law.

Because the underwriters are still determining how much the market is willing to pay, a preliminary prospectus does not contain the final public offering price. Furthermore, because the SEC is still reviewing the documents, a preliminary prospectus does not contain the effective date of the offering.

Alongside the red herring, an underwriter might publish an advertisement in a financial newspaper. A tombstone advertisement is a basic public announcement of a new securities offering. A tombstone advertisement is permitted during the cooling-off period precisely because it is so stripped down—it contains only the bare facts of the deal, such as the issuer's name, the underwriters, and the size of the offering. Because it lacks any persuasive sales language, a tombstone advertisement is not a binding offer to sell securities.

Modern markets, of course, move faster than print newspapers. Today, issuers often issue electronic communications, such as press releases or web posts about an offering. A Free Writing Prospectus is any written communication distributed by an issuer offering a security. Because these are often ad-hoc updates or summaries, a Free Writing Prospectus does not meet the standard informational requirements of a statutory prospectus. Nevertheless, it must be filed with the SEC and broadly tie back to the core registration statement.

A common misunderstanding among retail investors is that if a security is registered with the SEC, it must be a "good" or "safe" investment. This is fundamentally false.

The SEC reviews registration statements for completeness. More specifically, the SEC reviews registration statements to ensure adequate disclosure of material facts.

Think of a new stock offering as a locked box. The SEC’s job is not to judge the contents of the box; their job is to ensure the issuer writes an accurate, complete label on the outside of the box. If a company is structurally unsound and likely to bankrupt its investors, the SEC will clear the registration as long as the company perfectly and honestly discloses its imminent doom in the paperwork. Therefore:

- The SEC does not approve securities.

- The SEC does not disapprove securities.

Once the SEC is satisfied that the disclosures are complete, the offering is cleared for sale. At this point, the underwriters finalize the pricing.

A final prospectus must be delivered to all purchasers of a new public securities offering. Because the math is now finalized, a final prospectus includes the public offering price. It also includes the effective date of the offering, letting the buyer know exactly when the security became legally available.

From a regulatory standpoint, a final prospectus delivery must occur no later than the settlement date of the transaction. Historically, this meant mailing thick, heavy booklets to thousands of clients. Recognizing the inefficiency of paper in the digital age, the SEC modernized this rule. Today, the SEC access equals delivery rule allows a final prospectus to be delivered via the internet. By simply posting the document publicly on a compliant website, the access equals delivery rule satisfies the regulatory final prospectus delivery requirement.

The traditional corporate prospectus is designed for operating companies. However, investment companies require a different approach. Drowning a retail investor in a 300-page statutory document about a mutual fund often results in the investor reading nothing at all.

To solve this, mutual funds can provide investors with a summary prospectus. A summary prospectus is a shorter version of the full statutory mutual fund prospectus. It is precision-engineered to highlight the data that actually dictates a retail investor's net return. Specifically:

- A summary prospectus discloses mutual fund fees (such as sales loads and expense ratios).

- A summary prospectus discloses mutual fund investment objectives (what the fund is actually trying to achieve).

- A summary prospectus discloses historical mutual fund performance.

The exhaustive registration process of the 1933 Act is expensive and time-consuming. However, not every capital-raising event requires this level of federal oversight. The law carves out exemptions based on either the type of security or the type of transaction.

Exempt Securities

Certain issuers are trusted to such a degree, or regulated by other means, that their securities bypass standard SEC registration:

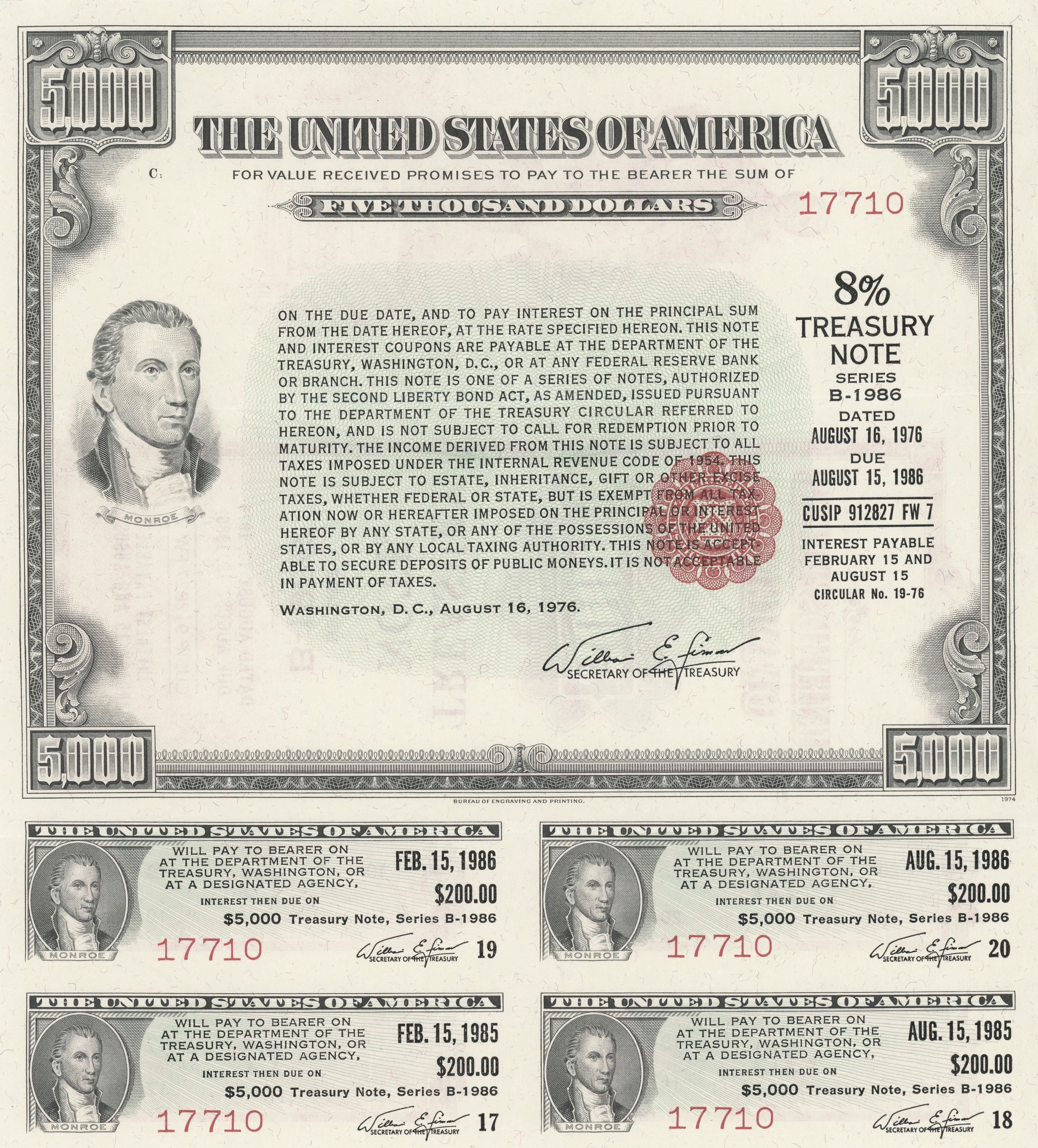

- Sovereign Debt: Securities issued by the United States government are exempt from SEC registration.

- Local Debt: Municipal bonds are exempt from the registration requirements of the Securities Act of 1933. However, municipal issuers still owe investors transparency. Instead of a prospectus, municipal securities issuers use an official statement as the primary disclosure document. For all practical intents and purposes, an official statement serves a similar disclosure purpose to a corporate prospectus.

- Short-Term Debt: Commercial paper with a maturity of 270 days or less is exempt from SEC registration. This exemption exists because commercial paper is used for short-term corporate working capital, not long-term capital formation, and is typically purchased by highly sophisticated institutional buyers.

- Charitable Entities: Securities issued by non-profit organizations are exempt from SEC registration, easing the financial burden on religious, educational, and charitable institutions.

Exempt Transactions

Sometimes, the security itself isn't exempt, but the manner in which it is sold exempts it from the full registration process.

- Regulation D: This rule provides a registration exemption for private placements. In a private placement, securities are sold directly to a select group of wealthy, sophisticated investors rather than the general public. Instead of filing a prospectus, an offering memorandum is the primary disclosure document used in a private placement.

- Rule 147: This rule provides a registration exemption for intrastate securities offerings. If a company in Texas sells stock solely to residents of Texas, the federal government's jurisdiction over interstate commerce is not triggered. (Note that state regulators will still be heavily involved).

- Regulation A: This rule provides a registration exemption for small corporate offerings. It acts as a "mini-IPO," allowing smaller startups to raise capital without absorbing the crushing legal fees of a full registration statement.

Imagine a massive utility company that knows it needs to raise $2 billion over the next three years to build out grid infrastructure. If market interest rates are volatile, forcing them to file a new registration statement every single time they want to issue bonds would cripple their ability to act swiftly when rates are favorable.

The solution is found in the SEC's delayed offering rules. Shelf registrations are governed by SEC Rule 415.

A shelf registration allows an issuer to register a new issue of securities upfront, but permits an issuer to delay the sale of previously registered securities. This mechanism provides issuers with the flexibility to time the market, acting essentially as a "pre-clearance" to issue shares or bonds exactly when conditions are ripe.

A shelf registration is valid for up to three years after the initial effective date. However, over three years, a company's financial realities change. To ensure investors have up-to-date information at the moment they actually buy the stock, a supplemental prospectus is filed with the SEC each time a company takes down shares from a shelf registration.

For the largest, most heavily analyzed companies in the world, the SEC grants even more leeway. Well-known seasoned issuers (WKSIs) qualify for automatic shelf registration. Because these massive entities are already followed by thousands of analysts and file exhaustive quarterly reports, their automatic shelf registrations become effective immediately upon filing with the SEC, bypassing the traditional cooling-off period entirely.

We have focused exclusively on federal regulations and the SEC. But the federal government is not the only authority monitoring the financial markets. State-level securities regulations are commonly referred to as blue-sky laws.

The term originates from an early 20th-century Supreme Court justice who warned of speculative schemes that had no more physical basis than "so many feet of blue sky." Blue-sky laws are designed to protect investors against fraudulent sales practices within a specific state.

Because navigating 50 entirely distinct legal codes would paralyze interstate finance, the Uniform Securities Act provides a model template for individual state blue-sky laws. This model helps standardize the rules across state lines.

For you, the future registered representative, blue-sky laws manifest as a strict three-pronged jurisdictional requirement:

- The Security: Issuers must register new securities in each state where the securities will be offered to the public. State-level registration of securities is required unless a specific state exemption applies.

- The Firm: Broker-dealers must be registered in a state before conducting securities business in that state.

- The Professional: Registered representatives must be registered in a state before conducting securities business in that state.

If you are a registered representative sitting in a New York office, and a prospective client from Florida calls you to buy a newly issued stock, you cannot legally execute that trade unless the stock is blue-skied in Florida, your firm is registered in Florida, and you hold the proper state registration in Florida.

Mastering these layers of disclosure—from the SEC's cooling-off period to the state administrator's blue-sky laws—is what separates a reckless salesperson from a true financial professional. The entire architecture of the capital markets rests on the reliable, systematic delivery of truth to the investor.