Earning, Spending, Saving, and Businesses

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

To a child observing the adult world, a modern economy looks indistinguishable from magic. Plastic cards summon groceries from store shelves, paper bills emerge freely from machines built into brick walls, and tapping a glass screen brings a hot meal to the front door. To teach elementary economics is to replace this illusion of magic with the mechanics of reality. It requires dismantling abstract adult systems into concrete, observable relationships that young learners can map onto their own lives. As a teacher, your task is not merely to define vocabulary, but to reveal the invisible wiring of human cooperation, choice, and trade.

Before we can teach a student how money moves, we must teach them why it moves. The entirety of economic theory rests on a single, inescapable friction: scarcity. Scarcity is the fundamental economic condition of having seemingly unlimited human wants in a world of limited resources. Time, energy, materials, and money are all finite.

Because we cannot have everything, we are forced to categorize our desires and make choices. We distinguish a financial need—something essential for survival, like food, shelter, or basic clothing—from a financial want, which is something desired that is not essential for survival, like a video game or a designer jacket.

Whenever we make a choice in a world of scarcity, something is left behind.

Opportunity Cost

The value of the next best alternative given up when making a financial choice.

If a student spends their allowance on a comic book, the opportunity cost is not the $4 they spent; it is the candy bar they would have bought if they hadn't bought the comic. Teaching opportunity cost early is a pedagogical masterstroke because it transforms "spending" from an isolated event into a comparative decision.

The Physicality of Value: The Coin Misconception

When introducing currency to young minds, you will encounter a persistent cognitive hurdle. Due to their developmental reliance on visual volume, elementary students often confuse the face value of coins with the physical size of the coins. A nickel is physically larger than a dime, so to a second-grader's intuitive logic, the nickel should buy more.

As an educator, you must explicitly break the link between physical size and monetary value. Value is a socially agreed-upon abstraction, not an intrinsic physical property of the metal disk.

Wealth does not spontaneously generate; it is produced. Work is the physical or mental effort used to produce goods and services. When an individual applies their work to the market, they are leveraging their human capital—the specific skills and knowledge possessed by an individual worker. A mechanic's knowledge of engines and a teacher's knowledge of pedagogy are both forms of human capital.

When human capital is put to work, it generates income, which is the money received by an individual in exchange for providing labor or selling goods. In the context of employment, this income typically takes the form of wages, the payments received by workers for the time and effort dedicated to a specific job.

Once a wage is earned, the individual faces a fork in the road:

- Spending: Exchanging money for goods or services to satisfy current needs and wants.

- Saving: The act of keeping a portion of current income for future use.

Saving requires delayed gratification, the ability to resist an immediate reward in favor of a later financial reward. Developmentally, this is immensely difficult for children. To make it tangible, we teach budgeting—the process of creating a plan to balance income with spending and saving. A budget makes the invisible concept of delayed gratification visible on paper.

Few topics in elementary education are as riddled with misconceptions as the banking system. To a child, a bank is either a magical dispensing machine or an oversized piggy bank. Let us systematically dismantle these illusions.

Banks are financial institutions that accept monetary deposits from individuals and businesses.

- A bank deposit is money placed into a financial account for safekeeping or to earn interest.

- A bank withdrawal is the act of taking money out of a financial account.

Individuals typically utilize two distinct types of accounts:

- A checking account is a bank service designed for frequent deposits and withdrawals to pay for daily expenses.

- A savings account is a bank service designed to hold money securely while generating interest.

Correcting Student Misconceptions about Banking

Misconception 1: The Personal Lockbox Elementary students frequently misunderstand bank operations by believing a bank physically locks individual deposits in a personal box. They think if they deposit a $20 bill with a tear in the corner, they will eventually withdraw that exact same torn bill.

The Pedagogical Fix: Teach the bank as a water reservoir. When you pour your bucket of water into the reservoir, it mixes with everyone else's water. When you want your water back, the bank gives you a bucketful of water. It is not the exact same water molecules, but it is the same amount of water.

Misconception 2: The Magic ATM Elementary students often hold the misconception that an ATM machine dispenses free money. They see parents press buttons and receive cash, unaware of the prerequisite labor and deposits.

The Pedagogical Fix: Connect the ATM explicitly to the concept of the checking account and wages. The machine only gives out what the worker has previously earned and deposited. It is a retrieval device, not a printing press.

Misconception 3: The Infinite Plastic Similarly, a common student misconception is that credit cards represent limitless money rather than borrowed funds.

The Pedagogical Fix: Introduce the concept of a loan. Banks provide loans to individuals and businesses using the funds deposited by other customers. When a parent swipes a credit card, the bank is paying the store, and the parent is promising to pay the bank back later.

This brings us to the engine of banking: Interest, which is a fee paid for the use of borrowed money.

- Banks pay interest to depositors as compensation for keeping money in the bank. (They are effectively borrowing the depositor's money to lend out).

- Banks charge interest to borrowers who take out financial loans.

The bank makes its money on the difference. They might pay depositors 2% interest, but charge borrowers 6% interest. Understanding this mechanism shifts the student's view of a bank from a "money warehouse" to a dynamic financial business.

If individuals supply labor and banks supply capital, who actually builds the products we buy? This requires an entrepreneur, an individual who takes a financial risk to start and operate a new business.

Entrepreneurs act as the great synthesizers of the economy. They combine resources such as labor and materials to produce goods or services. But why take the risk? Why spend money on materials and labor with no guarantee of success?

The answer is profit, the financial gain realized when the revenue from a business exceeds the costs of operating that business.

Profit = Total Revenue - Total Costs

This profit motive encourages entrepreneurs to create products that consumers want to buy.

The "Greedy Store Owner" Misconception

A common misconception among young learners is that store owners dictate prices without regard to consumer demand. A student might ask, "If the owner wants to make more money, why don't they just charge $100 for a candy bar?"

The Pedagogical Fix: You must teach students that the profit motive acts as a built-in constraint. Yes, the owner wants to make money, but if they price the candy bar at $100, consumers will exercise their freedom of choice and buy candy elsewhere (or not at all). The profit motive forces the entrepreneur to listen to consumer demand, balancing a price that is high enough to cover costs but low enough to attract buyers.

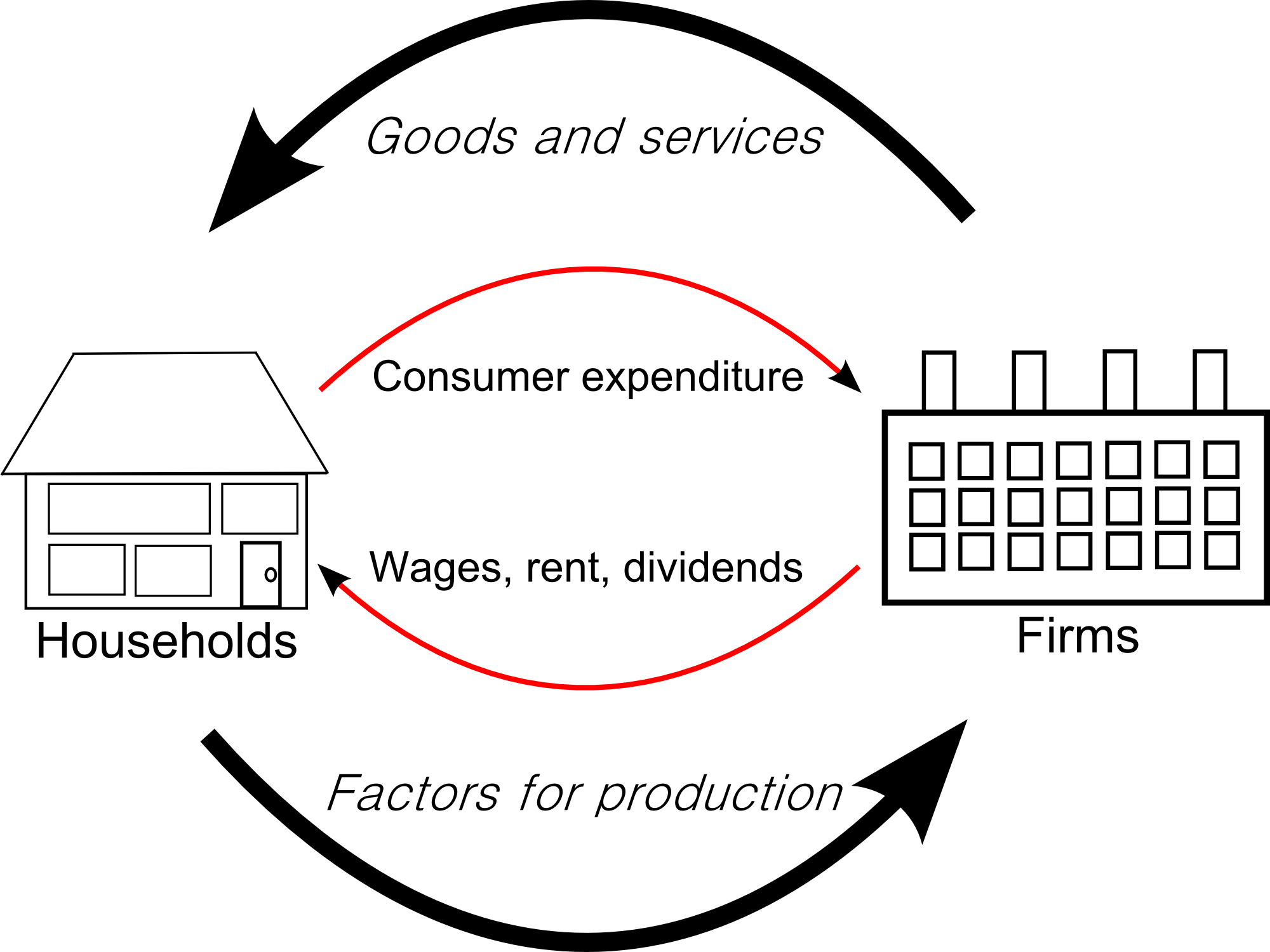

Eventually, you must zoom out and show students how all these isolated concepts connect into a unified system. We visualize this using a circular flow model, which illustrates the continuous movement of money and resources between households and businesses.

Imagine a cardiovascular system, where money is the blood.

- Individuals interact with businesses by exchanging money for the goods and services the businesses produce. (Money flows to businesses).

- Businesses interact with individuals by paying wages in exchange for labor. (Money flows back to individuals).

But this model is incomplete without addressing the infrastructure that makes safe trade possible. This is where the government steps in.

The government requires funding to operate, which it collects via taxes—mandatory financial charges levied by the government on individuals and businesses.

While students might view taxes merely as "money taken away," it is crucial to teach the other side of the equation. The government uses tax revenue to fund public goods and services. Public goods include community resources such as roads, bridges, public schools, libraries, and fire departments. These are goods that are difficult to provide profitably through private businesses because you cannot easily exclude people from using a road or a sidewalk.

By taxing the circular flow, the government builds the literal and figurative roads upon which the economy travels.

When you step into the classroom, remember that you are not just teaching vocabulary terms. You are providing the decoder ring for the adult world.

- Ground scarcity and opportunity cost in their daily choices.

- Link work and human capital directly to the wages they see adults earning.

- Shine a light inside the black box of banks, replacing magical ATMs and infinite credit cards with deposits, loans, and interest.

- Frame entrepreneurs as risk-takers driven by the profit motive, constrained by consumer demand.

- Tie it all together with the circular flow model and demonstrate how taxes fund the public goods that make their community function.

Mastering these concepts ensures you are not just dispensing facts, but cultivating a deep, structural understanding of how the world works.