Fundamental Economic Concepts

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Consider the complex ecosystem of an elementary school playground. A third-grader trades a highly coveted holographic trading card for a handful of colorful erasers. This seemingly trivial exchange is not merely child's play; it is a profound demonstration of resource allocation, subjective value, and market mechanics. To teach economics to young minds is to reveal the invisible architecture that governs their daily interactions. They are already consumers, traders, and laborers in their own right. Our task as educators is to equip them with the precise conceptual framework required to elevate their intuitive actions into formal economic reasoning. To teach this content effectively, you must master not only the macroeconomic laws of the world but the specific cognitive hurdles a child faces when first encountering them.

At the bedrock of all economic theory lies a singular, unavoidable paradox: human economic wants are virtually unlimited, yet the productive resources available to satisfy human wants are strictly limited.

This collision between the infinite human imagination and the finite physical world creates scarcity. Scarcity is the fundamental economic condition where limited resources cannot satisfy unlimited human wants. It is the engine of all economic activity because scarcity forces individuals and societies to make choices regarding resource allocation. If we had infinite resources, economics would not exist; there would be no need to make decisions about what to produce or consume.

To help elementary students categorize their unlimited desires, we divide the things they consume into two distinct classifications:

- Needs are defined as items strictly necessary for basic human survival. Specifically, food, potable water, and basic shelter are classified as fundamental economic needs.

- Wants are defined as items that people desire but do not strictly require for biological survival (e.g., toys, video games, vacations).

When a child uses a pencil or listens to a teacher, they are interacting with the end result of production—the formal process of creating economic goods and services. The individuals or businesses that make goods or provide services are producers, while the individuals or groups who purchase and use goods and services are consumers.

What exactly is being produced and consumed?

- Goods are tangible physical objects produced to satisfy human wants or needs (e.g., the desk, the textbook, an apple).

- Services are intangible actions performed by people to satisfy human wants or needs. For example, teaching, haircutting, and medical care are examples of economic services.

Productive Resources

To initiate production, producers require ingredients. Productive resources are the fundamental inputs utilized to produce economic goods and services. Economists categorize productive resources into natural resources, human resources, and capital resources, driven by a fourth element known as entrepreneurship.

| Resource Type | Definition | Classroom Example / Fact |

|---|---|---|

| Natural | Unaltered gifts of nature utilized directly in the production process. | Water, timber, minerals, and fertile soil. |

| Human | The physical and mental effort contributed by people toward production. | The labor of a teacher creating a lesson plan, or a farmer harvesting crops. |

| Capital | Human-made physical goods used repeatedly to produce other goods and services. | Machinery, hand tools, and factory buildings are classified as capital resources. |

| Entrepreneurship | The human effort of taking calculated financial risks to organize productive resources into a business. | A bakery owner deciding to buy ovens (capital) and hire bakers (human) to make bread. |

Pedagogical Warning: Elementary students commonly misidentify human-made outdoor structures as naturally occurring natural resources. Because a wooden park bench or a metal playground slide is located "in nature" outdoors, young minds often categorize them as natural. You must explicitly teach that once human effort alters a material into a tool or structure used repeatedly, it becomes a capital resource.

Because we live under the fundamental condition of scarcity, every action requires a trade-off. A foundational rule of economics is that every economic choice inherently involves a cost.

However, the economic definition of cost is much broader than the amount of money handed to a cashier. Opportunity cost is the specific value of the single next best alternative given up when a choice is made.

If a student has 30 minutes of free time and chooses to play kickball instead of reading a book or drawing a picture, the opportunity cost is the value of the single next best alternative—let's say, reading the book. Crucially, opportunity cost excludes the combined value of all unselected alternatives. The cost of playing kickball is just the foregone reading, not the reading plus the drawing. You cannot simultaneously read and draw in that 30-minute block anyway, so you only sacrifice the single most valuable alternative you would have chosen.

Pedagogical Warning: Elementary students often erroneously confuse the concept of opportunity cost with the exact monetary price tag of an item. If a student buys a

\$5toy, they will tell you the opportunity cost is\$5. You must correct this: the opportunity cost is the comic book or the candy they could have purchased with that\$5instead.

No single person possesses the natural, human, and capital resources to produce everything they want. This necessitates a highly orchestrated system of cooperation.

At the heart of this cooperation is the division of labor, a production method where a complex process is broken down into smaller, distinct tasks. When tasks are divided, it allows for specialization—the economic focus of individuals or groups on producing a single specific good or service.

Why do we specialize? Because specialization generally increases overall economic efficiency and productivity. A worker who spends all day attaching tires to a car will do it far faster and with fewer errors than a worker trying to build an entire car from scratch. However, this efficiency creates a structural vulnerability: economic interdependence, which is the reliance of individuals or groups on others to provide necessary goods and services. Specialization directly increases economic interdependence among individuals and nations. If you only make tires, you must rely on the farmer for food and the tailor for clothes.

Facilitating Exchange

Because of interdependence, we must trade. Trade is the voluntary exchange of goods and services between independent parties.

Historically, humanity relied on barter, which is the direct exchange of goods and services without utilizing any form of money (e.g., trading three chickens for a pair of shoes). Barter is highly inefficient because it requires a "double coincidence of wants"—the shoemaker must happen to want chickens at the exact moment the chicken-farmer needs shoes.

To solve this, society created money. Money functions as a generally accepted medium of exchange to facilitate trade. It eliminates the friction of barter.

Pedagogical Warnings on Money:

- Intrinsic vs. Assigned Value: A common elementary student misconception is that physical money has intrinsic material value rather than assigned value. They often believe a

\$20bill is physically made of precious materials, rather than understanding it is just paper and ink that society agrees has value.- The Source of Money: Young students frequently believe that commercial banks freely distribute money to the public. They see their parents go to an ATM, push a button, and receive cash, leading to the assumption that banks give away money rather than holding and returning earned wages.

When buyers and sellers come together, they form a market. A market is any physical or virtual mechanism where buyers and sellers interact to execute trades.

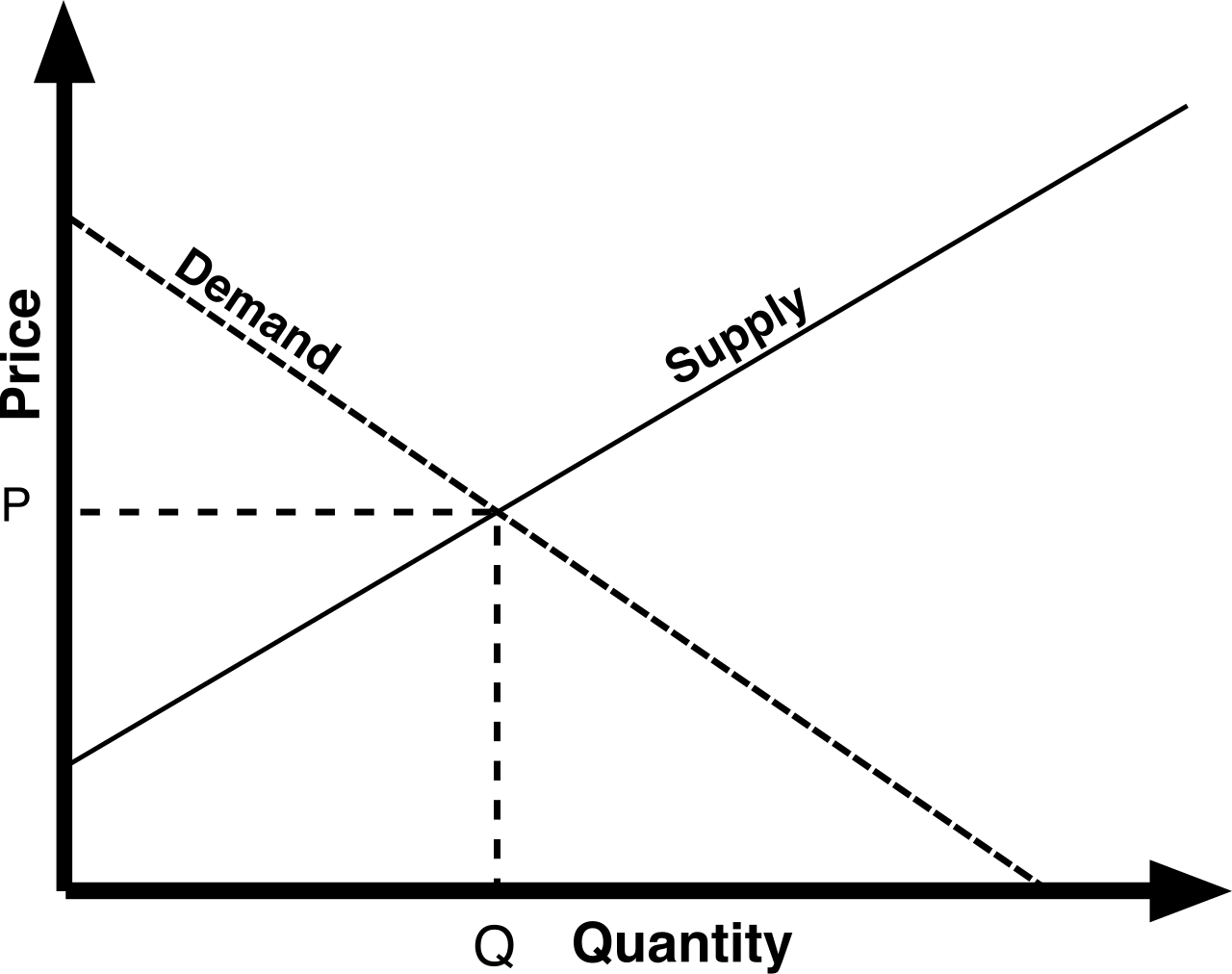

Within this market, two invisible forces interact to establish prices: supply and demand.

Understanding Demand (The Consumer's Role)

Demand represents the quantity of a good or service consumers are willing to buy at various prices. Consumer behavior is highly predictable and is codified in the law of demand:

- The law of demand states that consumers purchase a larger quantity of a product at lower prices. (Everyone wants a video game when it goes on clearance).

- Conversely, the law of demand states that consumers purchase a smaller quantity of a product at higher prices.

Understanding Supply (The Producer's Role)

Supply represents the quantity of a good or service producers are willing to offer for sale at various prices. Producer behavior is the mirror image of consumer behavior, codified in the law of supply:

- The law of supply states that producers offer more of a product for sale at higher prices. (If consumers are willing to pay

\$100for a toy, factories will work overtime to produce it). - Conversely, the law of supply states that producers offer less of a product for sale at lower prices.

Finding Equilibrium

Market prices are determined by the ongoing interaction of supply and demand forces. They are not randomly assigned; they are negotiated through mass behavior.

When the market functions perfectly, it reaches an equilibrium price, which is the specific price point where the quantity demanded exactly equals the quantity supplied. At equilibrium, the market clears—every producer sells their goods, and every consumer who wants one at that price gets one.

However, markets are dynamic and often experience disequilibrium:

- A shortage occurs when the quantity demanded of a good exceeds the quantity supplied at a specific price. (This happens when prices are set artificially low, causing a frenzy of buyers but little incentive for producers).

- A surplus occurs when the quantity supplied of a good exceeds the quantity demanded at a specific price. (This happens when prices are set too high, leaving products sitting on store shelves).

Pedagogical Warning: Children often hold the economic misconception that a high price naturally guarantees a high volume of consumer demand. Because they equate "expensive" with "luxurious" or "desirable," they falsely assume that if a store sets a price to

\$1,000for a sneaker, thousands of people will naturally flock to buy it. You must teach them that while high demand can cause high prices, arbitrarily setting a high price actually reduces the quantity demanded according to the law of demand.