Alternative investments and liquidity risk

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Imagine trying to sell a unique, hand-built vintage automobile at 2:00 PM on a Tuesday because you require immediate cash to pay an unexpected tax bill. The car possesses tremendous intrinsic value, but the market of ready, willing, and able buyers at that exact moment is virtually nonexistent. You face a stark choice: wait months to find the right buyer through specialized channels, or accept a massive, painful discount to liquidate it today. This fundamental friction—the inability to convert an asset to cash rapidly without a significant loss in value—is the defining characteristic that separates traditional stocks and bonds from the vast, complex universe of alternative investments.

When constructing a portfolio, financial planners introduce alternative investments because they behave differently than the broader stock and bond markets. Alternative investments generally have low correlation with traditional equity and fixed-income markets. When equities zig, alternatives often zag, or simply ignore the broader market movements altogether. Because of this non-correlated behavior, adding alternative investments to a traditional portfolio typically improves overall portfolio diversification.

But nature demands a trade-off. In exchange for this diversification, alternative investments generally exhibit higher liquidity risk than publicly traded stocks and bonds.

Liquidity risk is the probability that an investor cannot sell an asset quickly without accepting a heavily discounted price.

Because rational investors dislike having their wealth trapped, they demand compensation. Investors demand a liquidity premium in the form of higher expected returns as compensation for holding illiquid assets. If an investor is going to lock their money away, the expected payoff must mathematically justify the loss of flexibility.

Real estate is intrinsically illiquid—you cannot sell a fraction of a skyscraper to fund a child’s college tuition. To solve this, the financial industry created REITs. Real Estate Investment Trusts (REITs) pool investor capital to purchase or finance real estate properties.

To avoid corporate-level taxation and qualify for pass-through treatment, the IRS sets strict rules. To qualify as a REIT under US tax law, an entity must distribute at least 90 percent of its taxable income to shareholders annually. This makes them highly attractive to yield-seeking clients.

REITs generally fall into two functional categories:

- Equity REITs own and operate income-producing real estate properties. (Think shopping malls, apartment complexes, and data centers. Their revenues come primarily from rents.)

- Mortgage REITs provide financing for real estate by purchasing or originating mortgages and mortgage-backed securities. (They earn income from the interest on these financial instruments.)

The Two Faces of REIT Liquidity

Not all REITs offer the same access to your cash.

- Publicly Traded REITs: Publicly traded REITs offer high liquidity because their shares are bought and sold daily on major stock exchanges. If a client needs cash, you can sell shares of a public REIT just as easily as shares of Apple or Microsoft.

- Non-Traded REITs: Non-traded REITs are registered with the SEC but do not trade on national stock exchanges. They exist in a precarious middle ground. Because there is no active exchange to match buyers and sellers, non-traded REITs carry significant liquidity risk due to the lack of an active secondary market. Investors are generally reliant on the sponsor's limited share redemption programs, which can be suspended during economic downturns.

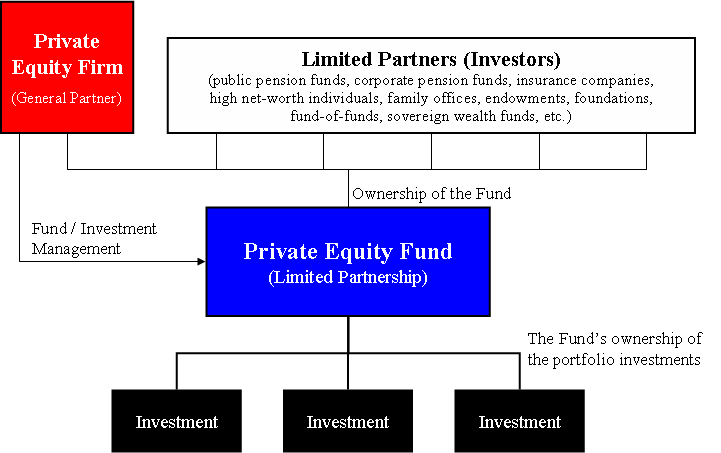

If public markets are the brightly lit, heavily regulated grocery store of investing, private markets are the direct farm-to-table supply chain. Private equity involves investing capital directly into private companies that are not listed on a public exchange.

Within this universe is a well-known, high-octane subcategory: Venture capital is a subset of private equity that provides funding to early-stage, high-growth companies.

Transforming a private company takes years of operational overhaul or technological development. Managers cannot achieve this if investors are constantly pulling their money out. Therefore, private equity investments typically impose multi-year lock-up periods.

A lock-up period restricts private equity investors from redeeming their shares for a specified duration, often spanning three to ten years or more.

For the CFP professional, this means private equity capital must be treated as utterly inaccessible for the duration of the lock-up.

Commodities represent physical goods such as precious metals, energy products, and agricultural crops.

Why add barrels of oil or bushels of wheat to a retirement portfolio? Because commodities historically act as a portfolio hedge against unexpected inflation. When the cost of living spikes, it is often because the underlying raw materials (energy to transport goods, grains to feed livestock) have become more expensive. Holding the commodities themselves provides a direct offset to inflationary pain.

However, owning physical assets creates logistical nightmares. Direct investments in physical commodities incur ongoing storage and insurance costs. You cannot simply store gold bullion or barrels of crude oil in a client's garage. To bypass these carrying costs, planners often use commodity futures or exchange-traded products rather than direct physical ownership.

The limited partnership (LP) is the structural bedrock for many alternative investments, including hedge funds, private equity funds, and real estate syndications.

By law, a limited partnership must have at least one general partner and at least one limited partner.

| Role | Liability Exposure | Management Control |

|---|---|---|

| General Partner (GP) | General partners in a limited partnership assume unlimited personal liability for the debts of the business. | Runs the day-to-day operations. |

| Limited Partner (LP) | Limited partners in a limited partnership have their financial liability restricted to their invested capital amount. | Passive investors; no daily management rights. |

Limited partnerships provide pass-through taxation for business income and losses. The partnership itself pays no entity-level income tax; instead, the tax attributes flow directly to the partners' individual tax returns via a Schedule K-1.

The Problem of Phantom Income

Because LPs are pass-through entities, partners are taxed on their proportional share of the earned income, regardless of whether cash was actually distributed.

Phantom income occurs when a limited partnership allocates taxable income to a partner without making a corresponding cash distribution.

Scenario: An LP earns $100,000 in net income and your client’s share is $10,000. However, the GP decides to reinvest all the cash into new equipment. Your client receives zero cash but still owes taxes on the $10,000. For a financial planner, failing to anticipate phantom income and prepare liquidity for the client’s tax bill is a severe unforced error.

Liquidity of Partnerships

Private limited partnership interests are highly illiquid investments due to severe restrictions on transferring ownership. You generally cannot sell your LP units without the explicit consent of the General Partner, making them unsuitable for emergency cash reserves.

However, the market created an exception: Master Limited Partnerships (MLPs) are limited partnerships that are publicly traded on a securities exchange. Primarily utilized in the energy infrastructure sector (like oil and gas pipelines), Master Limited Partnerships (MLPs) combine the tax benefits of a partnership with the liquidity of publicly traded stocks.

Collectibles include tangible assets like fine art, rare coins, vintage automobiles, and stamps.

While they can be visually beautiful and emotionally rewarding, mathematically, they are a drag on compounding wealth. Unlike stocks or real estate, collectibles do not generate ongoing interest or dividend income. Their only return comes from capital appreciation.

Furthermore, the tax code penalizes them. While traditional stocks enjoy a maximum 20% federal long-term capital gains tax rate, the maximum federal long-term capital gains tax rate on collectibles is 28 percent.

Collectibles are the ultimate illiquid asset. Collectibles carry high liquidity risk because finding a willing buyer requires specialized dealers or auction houses. Additionally, collectibles are subject to high valuation uncertainty due to subjective pricing and the lack of a centralized market. The value of a painting is purely what one specific person in a room is willing to pay on a given Tuesday.

Understanding the mechanics of these investments is only half the battle. The true test of a financial planner is integrating them into a holistic portfolio safely.

Investors with short-term cash needs must avoid heavy allocations to illiquid assets like private equity and direct real estate. Tying up funds required for an upcoming home purchase or tax bill in a non-traded REIT or a private LP is malpractice. A fundamental law of planning applies here: a high allocation to illiquid alternative investments reduces portfolio flexibility for meeting unexpected cash needs.

The Illusion of Smoothness: Appraisal-Based Valuation

How do you report the value of a private equity firm or an apartment building on a client's monthly statement? You cannot look up a ticker symbol. Valuation of illiquid assets often relies on periodic appraisals rather than continuous market pricing.

Because an asset isn't being priced by thousands of emotional buyers and sellers every second, its price appears incredibly stable on paper. Appraisal-based valuation can artificially smooth the reported volatility of an alternative investment compared to publicly traded securities. A client might look at their private real estate fund and think it is "safer" than the stock market because the line goes up smoothly, but this is an illusion created by the infrequency of pricing, not an absence of underlying economic risk.

The Rebalancing Dilemma

Finally, consider the mechanical act of maintaining a client's asset allocation. Illiquid alternative investments complicate portfolio rebalancing strategies because the assets cannot be sold rapidly to adjust target weights.

If the stock market crashes by 30%, equities will quickly become underweight in your client's portfolio, while their artificially "smoothed" private equity holdings will balloon to an overweight position. In a liquid portfolio, you would easily sell the winner to buy the cheaper loser. But with illiquid alts, your capital is locked up. You cannot sell the private equity to buy the discounted stocks. Planners must rely on external cash flows—like dividends or new client deposits—to rebalance, requiring a much higher degree of foresight and cash management discipline.