Fundamental and current tax law

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

The architecture of the United States tax system rests upon a single, constitutional pillar: the Sixteenth Amendment to the United States Constitution grants Congress the explicit power to levy and collect taxes on income. [1.3.7] Every strategy a financial planner constructs—from Roth conversions to estate asset transfers—flows downstream from this singular authority. Congress exercises this power by enacting federal tax laws, which are systematically codified in Title 26 of the United States Code. Known to professionals simply as the Internal Revenue Code, this body of law represents the highest statutory foundation of all federal tax law in the United States. To master tax planning for the CFP® exam, one must understand not just the Code itself, but the hierarchy of guidance interpreting it, how its progressive math functions, and how recent landmark legislation has fundamentally rewritten the rules of wealth accumulation.

When we examine the Internal Revenue Code, we are looking at a vast, intricate framework. But statutory language is often broad. It cannot anticipate every nuance of modern commerce or family dynamics. Therefore, we must rely on administrative interpretations to understand exactly how the law operates in practice. A crucial skill for any financial planner is knowing the precise legal weight of the documents you are reading.

Treasury Regulations: The Official Translations

If the Internal Revenue Code is the fundamental law, the Treasury Regulations constitute the official interpretation of the Internal Revenue Code by the Department of the Treasury. Think of these regulations as the operational manual for the Code. However, not all regulations carry the same legal weight. They exist in three distinct stages of finality:

| Regulation Type | Legal Weight & Function |

|---|---|

| Final Treasury Regulations | These are fully vetted and legally bind both the Internal Revenue Service and taxpayers. They are the ultimate rule of the road short of the statute itself. |

| Temporary Treasury Regulations | Issued when urgent guidance is needed. Temporary Treasury regulations hold the exact same binding legal authority as final regulations. They remain binding until the temporary regulations expire or become final regulations. |

| Proposed Treasury Regulations | Issued to solicit public comment before finalization. Proposed Treasury regulations provide insight into the current position of the Internal Revenue Service, but they completely lack binding legal authority. You cannot rely on them to defend a client in court. |

IRS Administrative Guidance: Rules of Engagement

Below the Treasury Regulations sits a layer of day-to-day operational guidance issued directly by the IRS. Financial planners must routinely navigate these rulings to answer specific client questions.

Revenue Rulings represent official interpretations by the Internal Revenue Service of how tax law applies to specific factual situations. If a client comes to you with a scenario that perfectly matches the facts of a published Revenue Ruling, you can confidently apply that ruling's conclusion to your client. Conversely, Revenue Procedures provide official procedural instructions on how taxpayers must comply with specific tax laws—they are the "how-to" guides for administrative tasks, like changing accounting methods or claiming specific safe harbors.

Exam Tip: The Internal Revenue Service publishes official Revenue Rulings and Revenue Procedures in the Internal Revenue Bulletin. Because they are published here, they carry significant authoritative weight, though less than Treasury Regulations.

Sometimes, a client is about to execute a massive, multi-million dollar transaction and wants an absolute guarantee of how the IRS will treat it. In these cases, they can pay the IRS to issue a Private Letter Ruling (PLR). A PLR applies strictly to the specific taxpayer requesting the ruling. While they are fascinating to read and indicate IRS thinking, tax professionals cannot cite a Private Letter Ruling as legal precedent for other taxpayers.

If a client is unfortunately selected for an audit and a complex, novel tax issue arises, the examining agent might request Technical Advice Memoranda (TAM). These provide guidance from the Internal Revenue Service National Office to field personnel during a taxpayer audit, ensuring the IRS applies the law consistently across different jurisdictions.

Finally, a warning regarding the informal documents you and your clients read every day on the internet. Informal Internal Revenue Service guidance such as Frequently Asked Questions lacks the force of law. Taxpayers cannot cite informal Internal Revenue Service publications as binding legal precedent. An FAQ on IRS.gov is helpful, but if the statute says one thing and an FAQ says another, the FAQ offers zero legal protection.

Crucial Dispute Strategy: What happens when your client fundamentally disagrees with the IRS's assessment? They have a choice of venue. However, the United States Tax Court allows taxpayers to litigate tax disputes without paying the disputed tax liability beforehand. This makes it the premier venue for most taxpayers who cannot afford to front massive sums while waiting for a judge's decision.

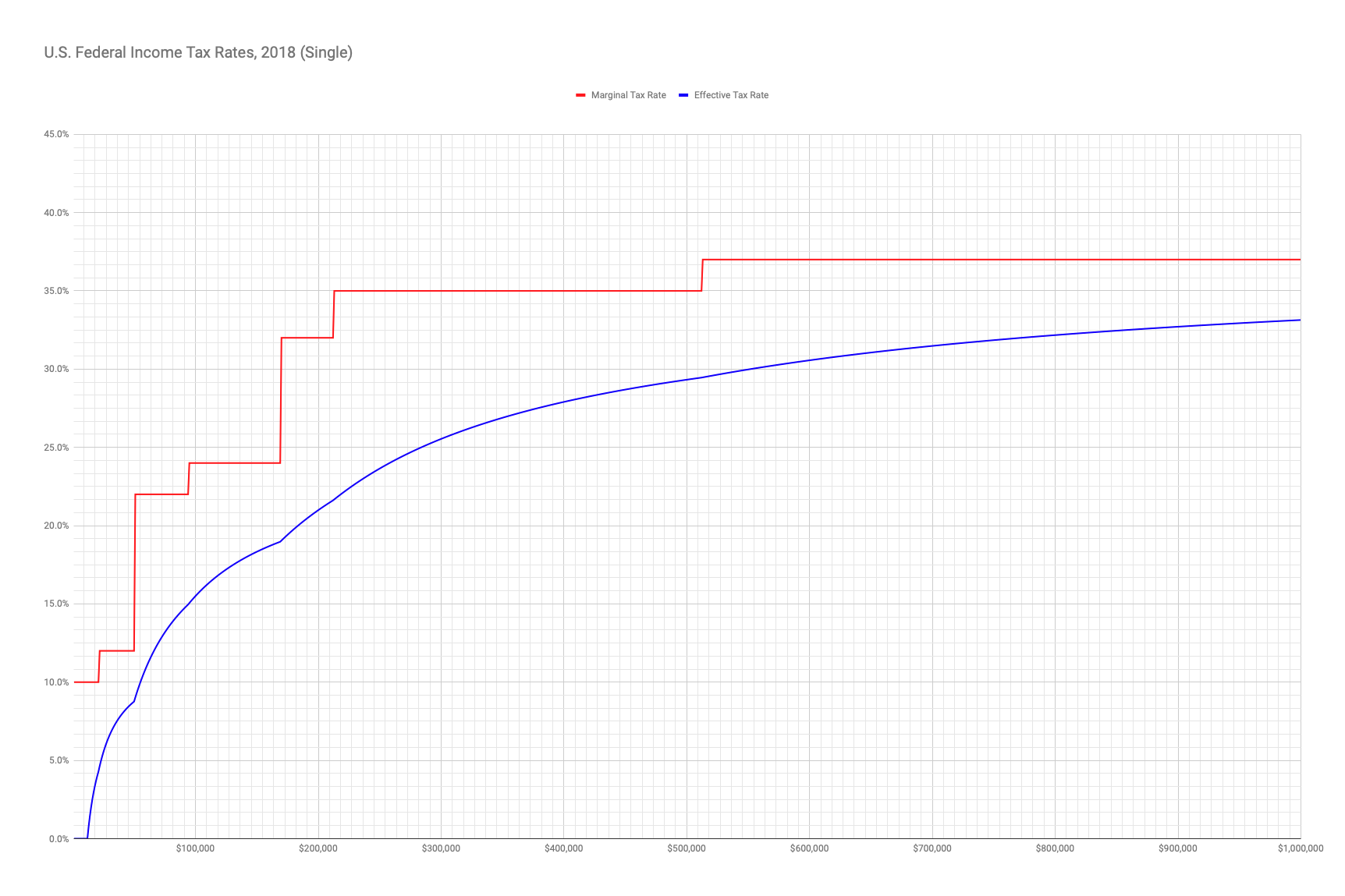

A surprising number of highly successful clients harbor a fundamental misunderstanding of how their income is taxed. You will frequently hear a client say, "I don't want to earn that extra bonus; it will push me into a higher bracket and I'll take home less money."

This mathematical fallacy is rooted in a misunderstanding of the progressive tax system. The progressive tax system divides taxable income into specific, tiered brackets. Crucially, the progressive tax system applies progressively higher tax rates exclusively to the income falling within each respective higher bracket.

Imagine a series of buckets. The first bucket holds income up to a certain threshold and taxes it at a low rate. Once that bucket is full, the excess spills into the next bucket, which is taxed at a slightly higher rate. The high rate of the second bucket never retroactively applies to the water in the first bucket. Earning more money in a progressive system always results in more after-tax wealth.

Financial planning requires up-to-the-minute knowledge of statutory changes. On July 4, 2025, the landscape of American taxation shifted dramatically when the One Big Beautiful Bill Act was signed into federal law.

This legislation was designed to resolve the looming expiration of the Tax Cuts and Jobs Act (TCJA) while introducing novel exclusions targeted at specific demographics. Let us deconstruct the structural changes you must integrate into your practice immediately.

1. Structural Permanence and Broad Rates

The most sweeping change is that the One Big Beautiful Bill Act made the majority of the individual tax provisions from the Tax Cuts and Jobs Act permanent. The looming sunset that planners spent years preparing for has been legislated away.

Furthermore, the Act maintained individual income tax brackets ranging from a bottom marginal rate of 10 percent to a top marginal rate of 37 percent. These permanent progressive brackets provide a stable foundation for long-term Roth conversion and income deferral strategies.

For your self-employed clients and small business owners, the anxiety surrounding pass-through income has been eliminated: the One Big Beautiful Bill Act established a permanent Qualified Business Income (QBI) deduction. Evaluating entity structures—such as whether a client should operate as an S-Corporation or a Sole Proprietorship—no longer requires factoring in a sunset date for this massive deduction.

2. Targeted Deductions and Exclusions

The legislation aggressively targeted relief toward specific taxpayer profiles, fundamentally altering how you advise families, retirees, and wage earners:

- Families: The One Big Beautiful Bill Act increased the Child Tax Credit to $2,200. This below-the-line, dollar-for-dollar reduction of tax liability dramatically enhances the cash flow of clients raising families.

- Retirees: Recognizing the fixed-income challenges of older Americans, the Act established a new $6,000 tax deduction for taxpayers who are at least 65 years old. This creates immediate tax planning opportunities the moment a client reaches their 65th birthday, shifting the math on when to take distributions from tax-deferred accounts.

- State and Local Taxpayers: For clients in high-tax states, the punitive $10,000 SALT cap of the TCJA era has been temporarily relaxed. The One Big Beautiful Bill Act raised the State and Local Tax (SALT) deduction cap to $40,400 for tax years 2026 through 2029. This four-year window requires immediate action regarding property tax and state income tax payment timing.

- Wage Earners: In a highly novel move, the Act carved out specific tranches of exempt compensation. First, it created a tax exclusion for tip income up to $25,000. Second, it created a tax exclusion for overtime pay up to $12,500. For clients in the service industry or those working heavy hourly shifts, this creates a distinct wedge between "Gross Income" and "Taxable Income" that has never existed in this format before.

3. Wealth Transfer Adjustments

Finally, the Act reshaped the horizons of estate planning. The One Big Beautiful Bill Act permanently increased the federal estate tax exemption to $15 million per individual.

By permanently establishing this historically high threshold, the focus of modern estate planning for the vast majority of your clients will formally shift away from federal estate tax avoidance and pivot heavily toward income tax planning, basis step-up optimization, and asset protection.

Mastering these distinctions—knowing exactly when a Treasury Regulation binds your client, how a progressive bracket captures their next dollar, and how the One Big Beautiful Bill Act impacts their balance sheet—is what separates a foundational financial advisor from an elite tax planner.