Classical economics models the investor as a perfectly rational calculating machine, relentlessly parsing data to meticulously optimize utility in a frictionless vacuum. Traditional finance assumes investors are perfectly rational and act purely to maximize their own wealth. Yet, when you sit across a conference table from a client who has just watched their retirement portfolio drop by 20% in a single month, you are not speaking to a rational calculating machine. You are speaking to a biological organism whose nervous system is reacting to a falling line on a screen with the same adrenaline response it would use to flee a physical predator.

Classical economics assumes investors are perfectly rational actors who meticulously maximize utility within given constraints, ignoring the biological and emotional realities of human behavior.

Modern portfolio theory relies on elegant mathematical models like the efficient frontier, contrasting sharply with the unpredictable reality of human behavioral biases.

As a CFP® professional, your technical mastery of taxation, estate planning, and asset allocation is only half your job. The other half is behavioral architecture. A brilliant financial plan is entirely worthless if your client abandons it at the first sign of market distress. To keep clients committed to their long-term plans, you must understand exactly how and why their minds deceive them, and deploy systematic strategies to protect them from themselves.

To correct a behavioral error, you must first diagnose its origin. Behavioral finance broadly categorizes investor errors into two distinct camps:

Emotional biases are spontaneous reactions driven by feelings or impulses rather than factual analysis. These are "hardware features"—deeply ingrained evolutionary responses rooted in fear, greed, or pride. They are exceptionally difficult to educate away and generally require structural mitigation rather than logical debate.

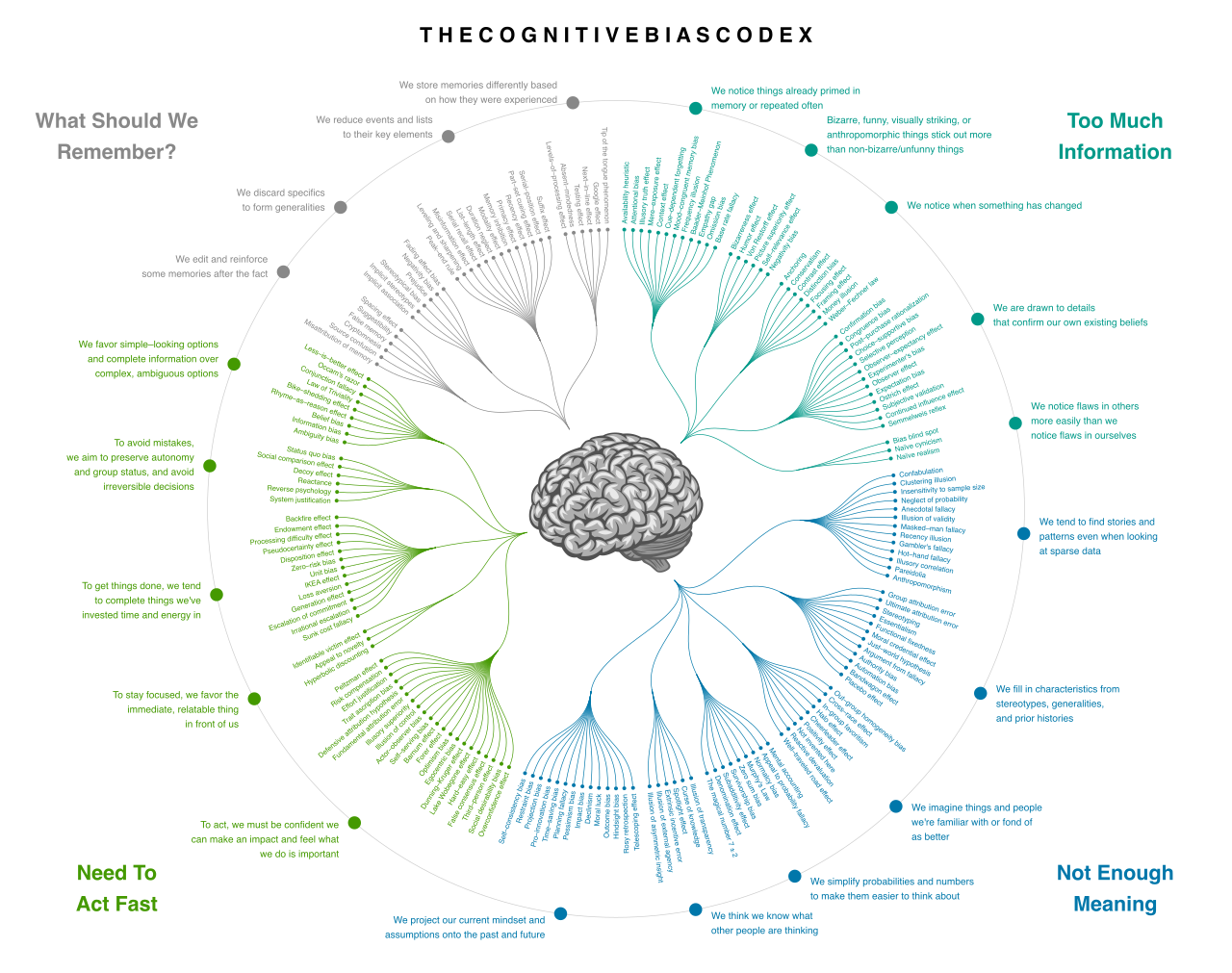

The Cognitive Bias Codex illustrates the vast array of systematic logical errors and heuristics that can derail rational decision-making in financial planning.

Source: Cognitive bias codex en by design: John Manoogian III categories and descriptions: Buster Benson implementation: TilmannR, CC BY-SA 4.0.

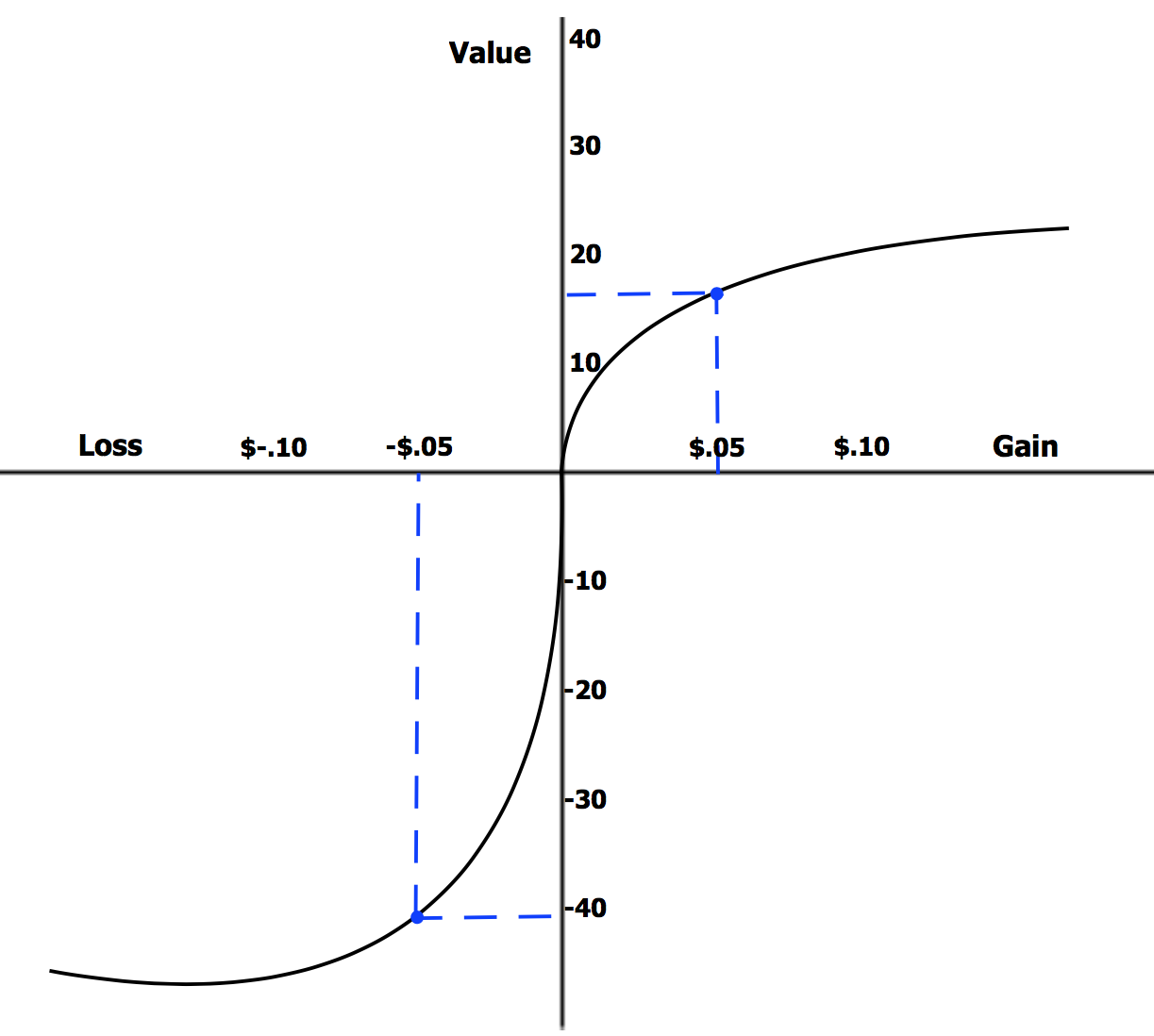

Prospect theory states that individuals evaluate potential gains and losses differently rather than focusing on the absolute outcome. Classical finance says that a client with $1 million who drops to $900,000 should feel exactly the same as a client with $800,000 who gains $100,000 to reach $900,000. Their absolute wealth is identical. But human beings do not experience life in absolute terms; we experience it relative to a reference point.

At the heart of prospect theory is a phenomenon that will govern nearly every client relationship you manage.

Loss Aversion: The psychological phenomenon where the pain of a financial loss is felt more intensely than the pleasure of an equivalent financial gain.

How much more intensely? Behavioral studies indicate the psychological pain of losing money is roughly twice as severe as the joy of gaining the exact same amount. Losing $10,000 feels like losing $20,000, while gaining $10,000 yields only a mild dopamine hit.

Prospect theory's asymmetrical value function visualizes loss aversion: the psychological penalty of a loss is significantly steeper and more intense than the pleasure of an equivalent gain.

This 2-to-1 asymmetry manifests in two incredibly destructive, yet entirely predictable, portfolio behaviors:

Loss aversion causes investors to hold onto losing investments too long in an attempt to avoid realizing a definitive loss. As long as the position is open, the loss is merely "paper." Selling makes the psychological pain real. They will ride a fundamentally broken stock to zero just to keep hope alive.

Conversely, loss aversion frequently causes investors to sell winning investments too early to lock in a guaranteed gain. The fear that the market will snatch away their unrealized profits outweighs the logical probability of continued compounding.

Beyond loss aversion, clients will walk into your office exhibiting a spectrum of cognitive and emotional biases. Let’s examine the most critical ones you will encounter.

Flawed Information Processing (Cognitive)

Mental Accounting: Money is fungible; a dollar is a dollar. However, mental accounting is the tendency of individuals to assign different psychological values to money based on its origin or intended use. For example, mental accounting can lead an investor to treat an unexpected tax refund as disposable income rather than long-term savings. They will meticulously budget their bi-weekly paycheck, but blow a $4,000 tax refund on a vacation because they mentally labeled it as "found money."

Anchoring Bias:The anchoring bias occurs when an individual relies too heavily on an initial piece of information to make subsequent judgments. In investing, this often defies logic. An investor exhibiting anchoring bias might fixate entirely on the historical purchase price of a stock when deciding whether to sell it. The market does not care what they paid for the stock five years ago, but the client’s mind is permanently anchored to that irrelevant metric.

The Framing Effect:The framing effect occurs when a decision is influenced by the specific way information is presented rather than the objective facts themselves. Telling a client "This portfolio has a 95% chance of succeeding" feels infinitely safer to them than "This portfolio has a 5% chance of catastrophic failure"—even though the mathematical reality is identical.

Belief Perseverance and Ego (Cognitive & Emotional)

Confirmation Bias: We love to be right. Confirmation bias is the human tendency to actively search for information that supports one's existing beliefs. In financial planning, confirmation bias causes investors to ignore objective market data that contradicts their current investment thesis. If they believe a specific tech stock is the future, they will read ten bullish articles and immediately scroll past the bearishearnings report.

Hindsight Bias: Have you ever had a client tell you, “I knew the market was going to crash last year!”? No, they didn't. Hindsight bias is the false belief that a past unpredictable market event was actually highly predictable. This is dangerous because it gives the client a false sense of security about predicting future events.

Overconfidence Bias: This is the emotional sibling to hindsight bias. Overconfidence bias leads investors to overestimate their own ability to accurately predict future market movements. The real-world consequences are devastating. First, overconfidence bias often results in excessive trading frequency, bleeding the portfolio dry through transaction costs and taxes. Second, overconfidence bias frequently results in poorly diversified investment portfolios, as the client is utterly convinced their concentrated bet is a sure thing.

Inertia and External Influence (Emotional)

Herding Behavior: Humans survived as a species by staying with the pack. Herding behavior is the psychological tendency of investors to copy the financial actions of a larger group. This evolutionary survival tactic is terrible for investing; herding behavior is a primary psychological contributor to the formation of asset bubbles and market panics.

Recency Bias:Recency bias is the tendency to overweight the importance of recent events when making long-term decisions. If the market dropped yesterday, the client feels it will drop forever. Consequently, recency bias can cause investors to abandon long-term equity strategies during temporary short-term market downturns.

The Endowment Effect:The endowment effect is the psychological bias where individuals assign a higher value to an asset simply because they currently own it. Ask a client what they would pay to buy their current concentrated company stock position today; they might say $50 a share. Ask them what they would sell it for; they might demand $80.

Status Quo Bias: We naturally resist change. The status quo bias is the psychological preference for maintaining the current state of affairs. This inertia can be highly detrimental; for example, the status quo bias can prevent a client from moving cash out of a low-yielding savings account into a higher-yielding investment, simply because opening the new account requires overcoming behavioral friction.

Sunk Cost Fallacy:The sunk cost fallacy is the tendency to continue investing in a losing proposition solely because of resources already committed. "I’ve already poured $50,000 into this failing rental property, I can't stop now." Rationality dictates that the past $50,000 is gone regardless of what they do today; decisions must be based on future expected value, not past unrecoverable costs.

The sunk cost fallacy is often termed the "Concorde fallacy," referencing the continued funding of the costly supersonic jet project based on past unrecoverable expenses rather than logical future expected value.

Knowing these biases exist is interesting psychology; deploying strategies to neutralize them is elite financial planning. As a CFP® professional, your mandate is to structure the client's financial environment so that doing the right thing becomes effortless, and doing the wrong thing becomes difficult.

Creating Structural Anchors

Before the storm hits, you must build the shelter. This begins with policy. Establishing a written Investment Policy Statement (IPS) creates a rational framework for future portfolio decisions. When the market is calm, you and the client logically agree on asset allocation, rebalancing thresholds, and risk tolerance.

When a panic inevitably hits and recency bias takes over, you do not argue with the client's fear. You point to the document. An Investment Policy Statement serves as an objective anchor to help mitigate client emotional reactions during periods of severe market volatility.

Automating the Journey

One of the most effective ways to bypass emotional biases is to remove the client from the decision-making loop entirely. Automating regular investment contributions removes the emotional hesitation from ongoing market timing decisions. When contributions happen mechanically on the 1st and 15th of the month, the client doesn't have to consciously decide if "now is a good time to buy."

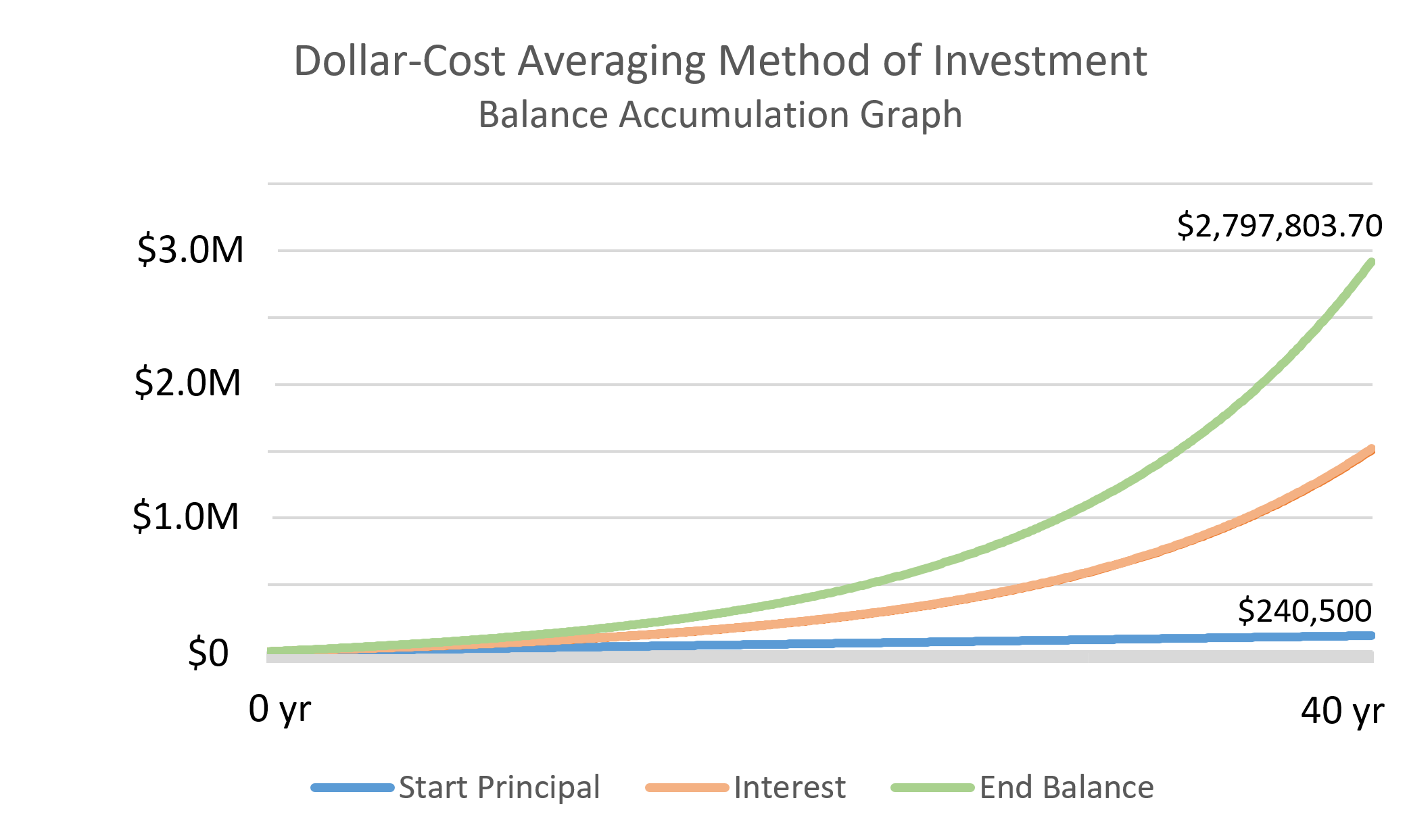

When a client inherits a large sum or sells a business, they are often paralyzed by the prospect of deploying the capital. What if I buy today and the market crashes tomorrow?Dollar-cost averaging is an automated investment strategy that directly helps clients overcome the psychological fear of investing a lump sum right before a market drop. By breaking the investment into systematic tranches, you soothe their loss aversion.

Dollar-cost averaging automates the investment process over time, mechanically bypassing the emotional friction and loss aversion associated with attempting to market-time a lump sum.

Because human beings are highly susceptible to presentation, you can use the framing effect for good. Financial planners can mitigate client framing bias by consistently presenting potential investment outcomes in both specific dollar amounts and percentage terms. Saying a portfolio dropped "10%" might sound abstract, while saying it dropped "$150,000" might sound terrifying. By presenting both—“We are down 10%, which is $150,000, leaving us with a highly secure $1.35 million that fully funds your retirement”—you strip the cognitive distortion away and present whole, objective reality.

When markets do decline, you must alter how the client perceives the pain. Financial planners can creatively counteract client loss aversion by framing inevitable portfolio declines as valuable opportunities for tax-loss harvesting. Instead of sitting helplessly while the screen bleeds red, you reframe the event as proactive, strategic action. You aren't "losing money"; you are "harvesting valuable tax assets to offset future gains." You pivot their brain from a state of victimhood to a state of opportunistic execution.

Building Friction Against Impulse

Finally, when a client is in the grip of an acute emotional bias—perhaps driven by a news cycle (herding) or a hot tip from a neighbor—they will demand immediate action. To protect them, introduce beneficial friction. Implementing a mandatory waiting period before executing a client's spontaneous trade request effectively reduces impulsive financial decision-making. Asking a client, "I have noted your request to liquidate your tech holdings. As per our agreed-upon protocol in your IPS, let's schedule a call in 48 hours to review the tax implications before we execute," gives their prefrontal cortex time to catch up with their amygdala.

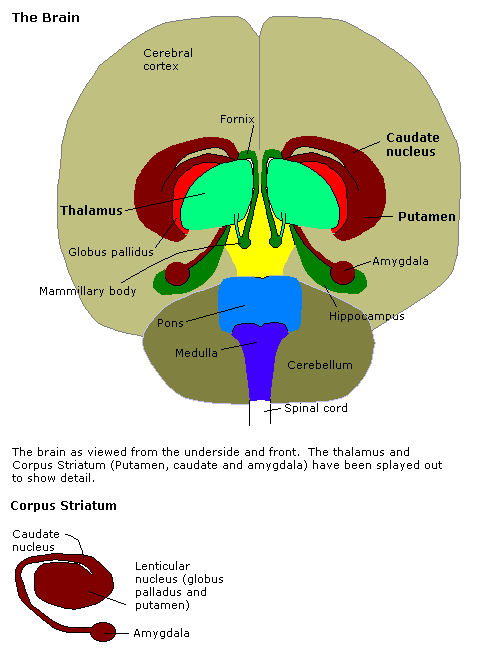

The amygdala (highlighted in red) governs emotional and impulsive fear reactions, often overriding the logical decision-making processed in the prefrontal cortex during times of acute financial stress.

Mastering behavioral finance transforms you from a mere asset allocator into a true financial guardian. By understanding the profound irrationality built into human neurobiology, you can construct portfolios, policies, and communication frameworks that allow your clients to successfully weather the most dangerous element in the financial markets: their own minds.