Client and planner attitudes, values, biases

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

Human beings do not behave like spreadsheets. When a practitioner constructs a Monte Carlo simulation or optimizes a tax-efficient withdrawal strategy, the mathematics assume a frictionless environment. But as any seasoned financial planner will discover, a mathematically flawless plan is frequently derailed by the architect of its execution: the human mind. Acknowledging that the success of a financial plan relies just as heavily on navigating human behavior as it does on quantitative analysis, The Psychology of Financial Planning was formally introduced as a Principal Knowledge Topic for the CFP exam in 2022.

To understand client behavior, we must first recognize the philosophical shift in how the financial planning profession views decision-making.

Traditional finance theories assume investors are perfectly rational actors maximizing utility. In this idealized model, if you present a client with a portfolio that optimizes their risk-adjusted return, they will accept it without hesitation. They act purely as calculating machines, untouched by sentiment.

However, reality routinely contradicts this assumption. Behavioral finance integrates psychological principles with traditional finance theories to explain irrational financial decisions. Instead of assuming perfect rationality, behavioral finance assumes investors are prone to predictable emotional and cognitive errors. By studying these predictable errors, financial planners can anticipate them, mitigate them, and ultimately guide clients toward their stated goals.

When a client makes a suboptimal decision, the planner must first diagnose the root cause. Behavioral finance categorizes these mental hurdles into two distinct buckets: cognitive errors and emotional biases.

Cognitive biases are systematic errors in thinking arising from faulty reasoning or memory. Think of these as "software glitches"—errors in the brain's information processing. Because they are rooted in logic and memory rather than deep sentiment, cognitive biases are generally easier to correct through education than emotional biases.

Emotional biases stem from feelings, impulses, or intuition. These are "hardware" issues. They are deeply ingrained evolutionary responses, making them highly resistant to purely logical arguments. You cannot simply educate a client out of an emotional bias; you must accommodate and manage it.

Cognitive Biases: Errors in Processing

Because they represent faulty reasoning, cognitive biases frequently manifest when clients are overwhelmed by data or relying on mental shortcuts (heuristics).

- Anchoring Bias: Anchoring bias involves relying too heavily on the first piece of information encountered during decision making. For example, an investor exhibiting anchoring bias might fixate entirely on the initial purchase price of a stock. Even if the underlying company fundamentals have fundamentally collapsed, the client anchors to that original $50/share price, refusing to sell until it "gets back to what I paid for it."

- Confirmation Bias: Confirmation bias is the tendency to search for information validating preexisting beliefs. A client convinced that a specific tech stock is the next massive breakthrough will read blog posts praising the company but ignore earnings reports showing catastrophic debt. Ultimately, confirmation bias causes investors to actively ignore data contradicting an established investment thesis.

- Recency Bias: Recency bias places disproportionate cognitive weight on recent events. If the market has surged over the past six months, recency bias leads investors to incorrectly assume recent market trends will continue indefinitely. This is precisely why clients eagerly demand aggressive equity allocations at the very peak of a bull market.

- Overconfidence Bias: Overconfidence bias is an unwarranted faith in one's own intuitive reasoning, judgments, or abilities. Because they believe they can "beat the market" through superior insight, overconfidence bias often leads an investor to execute excessive trades, churning their portfolio and destroying returns through transaction costs and taxes.

- Availability Heuristic: The availability heuristic relies on immediate examples coming rapidly to a person's mind. If a client recently watched a news segment about a local real estate crash, they may refuse to invest in REITs, overestimating the probability of a crash simply because the memory is easily retrievable.

- Mental Accounting: Money is fungible, meaning every dollar has the exact same purchasing power. Yet, mental accounting treats identical sums of money differently depending on the money's origin or intended use. A client might meticulously save their salary for retirement while recklessly gambling a $10,000 tax refund because they perceive it as "found money."

- Familiarity Bias: Familiarity bias is the tendency to invest disproportionately in well-known companies or familiar domestic markets. A client might insist on having 80% of their portfolio in the stock of the employer they work for, ignoring the immense concentration risk.

- The Framing Effect: The framing effect occurs when financial decisions are heavily influenced by the presentation format of information. A client might reject an investment with a "20% chance of failure" but enthusiastically accept the same investment when framed as having an "80% chance of success."

- Hindsight Bias: Hindsight bias is the psychological belief that a past event was completely predictable. After a market correction, a client exhibiting this bias will claim, "I knew the market was going to crash," forgetting that they had no such conviction beforehand.

Emotional Biases: The Pull of Intuition

Emotional biases are driven by psychological comfort, ego, and the fear of regret.

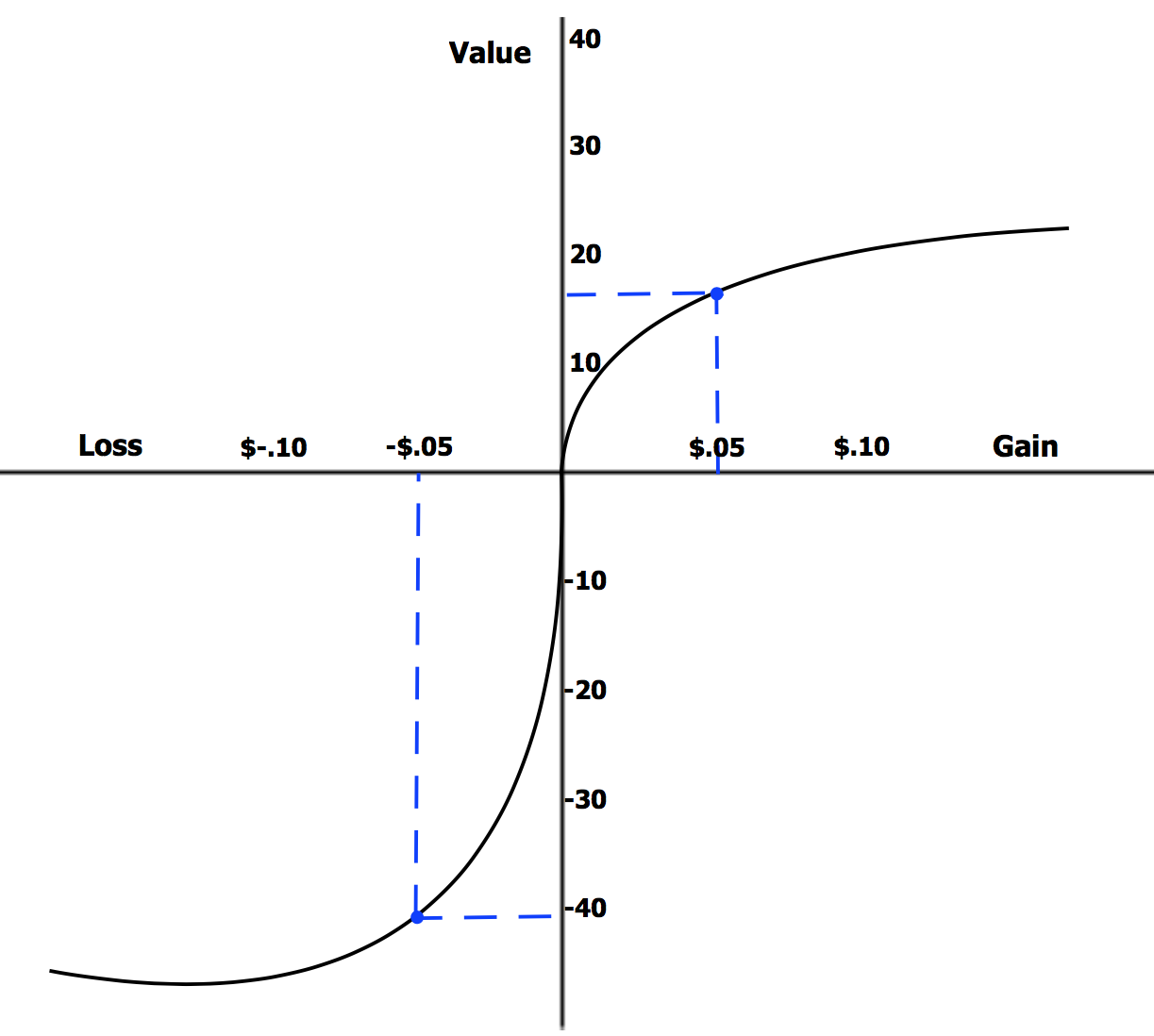

- Loss Aversion: Loss aversion is the psychological phenomenon where the pain of losing money feels significantly more intense than the joy of an equivalent gain. Studies show losing 1,000hurtsroughlytwiceasmuchasfinding1,000 feels good.

- The Disposition Effect: Driven by a mix of loss aversion and ego, the disposition effect is the behavioral tendency to sell winning investments prematurely (to lock in the psychological reward of being "right"). Conversely, the disposition effect includes the behavioral tendency to hold losing investments much longer than rationally justified (because selling realizes the loss and forces the client to admit they made a mistake).

- Endowment Effect: The endowment effect causes individuals to value an owned asset substantially more than an identical unowned asset. A client who inherited their grandfather’s dividend stock will demand a much higher premium to part with it than they would ever be willing to pay to acquire it in the open market.

- Status Quo Bias: Doing nothing is a choice, and often, it is the most comfortable one. Status quo bias is a psychological preference for keeping current financial arrangements exactly the same. Even if a planner proves a new asset allocation is mathematically superior, the client may resist the transition simply due to the emotional inertia of change.

A critical focus for the CFP® exam is recognizing that cognitive biases do not solely afflict the client. Financial planners, despite their expertise, are human beings subject to the exact same cognitive distortions. Recognizing these blind spots is an ethical and professional imperative.

| Bias | Impact on the Financial Planner |

|---|---|

| Confirmation Bias | A financial planner's confirmation bias can severely restrict the evaluation of alternative financial strategies for a client. If a planner inherently prefers whole life insurance, they may only research data supporting its use, failing to explore objectively better term-life strategies for their specific client. |

| Recency Bias | A financial planner's recency bias can result in portfolio allocations heavily weighted toward recently outperforming asset classes. A planner might heavily tilt a client's portfolio toward emerging markets simply because that sector led the previous year's returns. |

| Overconfidence Bias | Overconfidence bias can cause a financial planner to make excessively risky portfolio recommendations. A planner who recently predicted a market movement might suddenly feel invincible, taking unwarranted risks with client capital. |

| Hindsight Bias | Hindsight bias can cause a financial planner to unfairly critique a client's past financial decisions. Reviewing a client's previously self-managed portfolio, a planner might say, "It was obvious tech was going to drop," lacking empathy for the information the client actually had at the time. |

Long before a client sits across from a financial planner, their financial worldview has been rigidly constructed. Money scripts are unconscious, core beliefs about money formed primarily in early childhood. They are the silent operating systems running in the background of every financial decision.

Pioneering this field, psychologists Brad Klontz and Ted Klontz developed the four distinct money script categories used in financial psychology.

- Money Avoidance: Money avoidance is a money script where individuals believe money is a fundamental source of evil or stress. These clients may self-sabotage their wealth accumulation, ignore their bank statements, or feel deep guilt about having more than their peers.

- Money Worship: Money worship is a money script where individuals believe an increase in income will automatically resolve all life problems. This often leads to chronic overspending, extreme workaholism, and an unquenchable thirst for more, as the elusive "enough" is never reached.

- Money Status: Money status is a money script inextricably linking an individual's self-worth to the individual's net worth. Clients with this script often engage in competitive consumption—buying luxury cars or homes they cannot afford to project an image of success.

- Money Vigilance: Money vigilance is a money script characterized by extreme frugality and deep secrecy regarding personal finances. While these clients are often excellent savers, their relationship with money is driven by intense anxiety. They rarely enjoy their wealth.

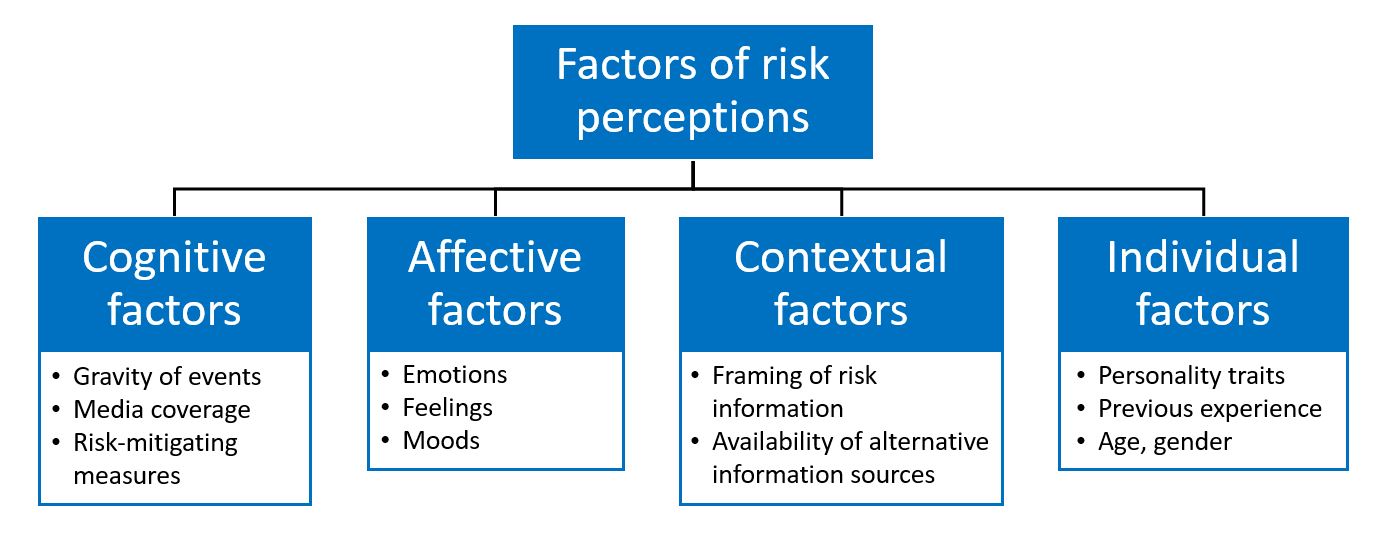

Risk is not a single, monolithic concept. When designing a portfolio, a planner must carefully untangle three separate elements of risk, distinguishing between a client's emotions, their math, and their cognitive processing.

- Risk Tolerance: Risk tolerance is a client's psychological willingness to take financial risks. It is emotional. Does market volatility keep them awake at night?

- Risk Capacity: Risk capacity is a client's objective, mathematical ability to endure financial losses without jeopardizing financial goals. This is driven by age, income, time horizon, and liquidity constraints.

- Risk Perception: Risk perception is a client's subjective assessment of the danger inherent in a specific investment. (e.g., A client perceiving international stocks as wildly dangerous despite historical data).

The Golden Rule of Risk: When designing a plan, what happens if a client has a high psychological tolerance for risk, but a low mathematical capacity (e.g., an aggressive 75-year-old with low savings)? Or conversely, a massive capacity but a low tolerance? A mismatch between risk tolerance and risk capacity generally requires the financial planner to prioritize the lower of the two metrics. You cannot force a terrified client into equities (they will sell at the bottom), nor can you allow a poor client to gamble away their necessary living expenses.

How do you untangle a client's money scripts, emotional biases, and conflicting risk metrics without making them feel interrogated or judged?

You cannot simply tell a client they are suffering from confirmation bias. The solution lies in communication techniques. Reflective listening helps a financial planner uncover a client's underlying money attitudes without creating defensiveness. By paraphrasing the client's statements and reflecting their emotions back to them (e.g., "It sounds like you feel highly anxious when thinking about passing down this inherited stock"), the planner creates a psychologically safe environment. This allows the client to hear their own reasoning out loud, opening the door for education, course correction, and ultimately, a successful financial plan.