Cash flow management

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

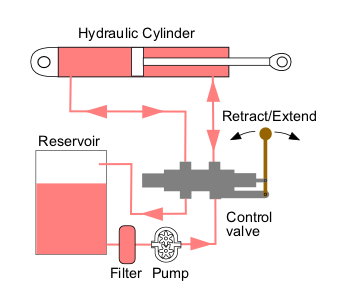

Consider a closed hydraulic system where fluid flows in at variable rates and drains out through multiple valves. If the outflow valves are left wide open, the reservoir depletes, leaving the system highly vulnerable to sudden drops in input pressure. Financial planning operates on identical principles, only the fluid is capital. At the center of every comprehensive financial plan is the mechanics of liquidity: how capital enters the household, how it exits, and how efficiently it is captured in the reservoir. For the financial planning practitioner, mastering cash flow management is the prerequisite to every other strategic recommendation—from asset allocation to tax mitigation. You cannot optimize a portfolio if the client is bleeding capital through unchecked monthly outflows.

Fundamentally, cash flow management involves tracking and optimizing a client's cash inflows and outflows. Without this foundation, financial planning is mere guesswork.

To analyze a household's financial physics, we categorize the movement of money into two distinct flows:

- Cash inflows include all sources of income entering the household, such as salary, bonuses, interest, dividends, and rental income.

- Cash outflows consist of all capital leaving the household, including expenses, taxes, savings contributions, and debt payments.

When you sit across from a client, the immediate health of their financial life is summarized by one simple equation:

Net Cash Flow = Total Cash Inflows - Total Cash Outflows

Calculated over a specific period, this formula reveals the fundamental trajectory of the client's wealth. A positive net cash flow indicates that total inflows exceed total outflows, meaning the client is generating surplus capital that can be deployed toward wealth accumulation. Conversely, a negative net cash flow indicates that total outflows exceed total inflows. A negative net cash flow mathematically guarantees the depletion of assets or the accumulation of debt.

Many clients, and even some practitioners, confuse a cash flow statement with a budget. To understand the difference, imagine driving a car.

A cash flow statement is looking in the rearview mirror. It is a historical record of a client's actual cash inflows and outflows over a past period. It diagnoses exactly what did happen.

A budget, on the other hand, is looking through the windshield. It is a forward-looking financial plan used to allocate future income toward expenses, debt repayment, and savings. A budget differs from a cash flow statement because a budget projects future allocations rather than recording past transactions.

When you begin developing a client budget, you must perform two essential tasks:

- Identify all expected future income sources.

- Categorize all anticipated expenses into specific buckets.

But how do you know if a client's budget projections are rooted in reality? Human beings are notoriously poor at estimating their own behavior. Analyzing historical bank statements and credit card statements is the most reliable way to identify a client's baseline spending habits. This historical data provides the empirical truth needed to construct a realistic forward-looking budget.

Once the budget is built, the work is not over. Tracking actual spending against a formal budget is necessary to identify cash flow leakages. What are cash flow leakages? They are those recurring, unmonitored small expenses—the daily premium coffee, the forgotten app subscriptions—that collectively reduce the client's overall savings capacity. A single drop of water seems harmless, but a slow leak will eventually empty the reservoir.

To optimize a client's cash flow, we cannot treat all expenses equally. We must dissect them based on necessity and predictability. Developing a client budget requires categorizing all anticipated expenses into discretionary and non-discretionary buckets.

Necessity: Discretionary vs. Non-Discretionary

- Non-discretionary expenses are essential costs required to maintain a client's basic standard of living. Examples of non-discretionary expenses include mortgage payments, utilities, taxes, and groceries. You cannot easily eliminate these without fundamentally disrupting the client's survival or legal standing.

- Discretionary expenses are flexible costs that a client can control or eliminate without impacting basic living standards. Entertainment, vacations, and dining out are classic examples of discretionary expenses.

Predictability: Fixed vs. Variable

Expenses must also be viewed through the lens of predictability:

- Fixed expenses are recurring costs that remain constant in amount from period to period. Auto loan payments and fixed-rate mortgage payments are examples of fixed expenses.

- Variable expenses are recurring costs that fluctuate in amount from period to period. Utility bills and grocery expenses are examples of variable expenses.

Notice how these categories intersect. A mortgage payment is a fixed, non-discretionary expense. Groceries are a variable, non-discretionary expense—you must eat, but you can choose between generic oats and prime rib. Vacation spending is a variable, discretionary expense.

Understanding these intersections is vital for the CFP® exam. When asked to improve a client's savings rate immediately, you must look at the variables you control. Reducing discretionary expenses is the most direct and immediate strategy to increase a client's capacity to save.

Clients often need a heuristic—a mental model—to structure their cash outflows. The CFP® exam will test your familiarity with several primary budgeting frameworks:

The 50/30/20 Budgeting Rule

This rule provides a simple, macro-level benchmark for household cash flow based on after-tax income:

- Allocates 50 percent of after-tax income to non-discretionary needs.

- Allocates 30 percent of after-tax income to discretionary wants.

- Allocates 20 percent of after-tax income to savings and debt repayment.

Zero-Based Budgeting

For clients who need precise control, zero-based budgeting is an active accounting method that requires assigning every single dollar of income to a specific expense, savings, or debt category. In zero-based budgeting, total expected income minus total budgeted allocations must exactly equal zero. There are no "leftover" or unassigned funds; every dollar is given a specific job.

The Envelope Method

Behavioral finance teaches us that clients spend physical currency differently than digital abstractions. The envelope method is a highly tactical budgeting technique that limits spending by allocating physical cash to specific spending categories (e.g., groceries, entertainment). When the "dining out" envelope is empty, the client simply cannot dine out again until the next period.

The ultimate goal of budgeting and expense categorization is to optimize the savings rate. The personal savings rate is the engine of wealth accumulation; without it, the most sophisticated investment strategy is just a high-performance engine with an empty fuel tank.

Personal Savings Rate = Total Savings / Gross Income

Notice that while the 50/30/20 rule utilizes after-tax income, the formal personal savings rate is calculated by dividing total savings by the client's gross income.

A standard CFP benchmark for a target personal savings rate is 10 to 12 percent of gross income. However, this is not a static rule. The target savings rate benchmark must be adjusted upward if the client starts saving for retirement later in life, simply because they have less time for compounding interest to do the heavy lifting.

The Mechanics of Saving: Pay Yourself First

Knowing the target is useless if the client's behavior prevents them from hitting it. Relying on willpower at the end of the month to save "whatever is left" is a mathematically proven path to failure.

Instead, recommend the "pay yourself first" strategy. This involves automatically transferring a portion of income to savings before paying other expenses. Automating savings contributions is powerful because it reduces the psychological friction of setting aside money. It removes human error and temptation from the equation entirely.

Beyond merely cutting discretionary spending (dining out less), as a practitioner, you must look for structural inefficiencies in a client's cash outflows. Two powerful levers are debt restructuring and insurance optimization.

Debt Restructuring

High-interest debt is a severe headwind to wealth accumulation. Debt restructuring can improve a client's savings rate by lowering monthly required interest payments. Common debt restructuring strategies include refinancing high-interest debt (like credit card balances) into lower-interest loans (like a personal loan or a home equity line of credit). By lowering the cost of capital, the client frees up cash flow that can be redirected into savings.

Insurance Optimization

Insurance policies often consume a significant portion of monthly cash flow. You can optimize this by adjusting the risk-sharing dynamic between the client and the insurer. Increasing a client's insurance deductibles can reduce recurring premium outflows. Consequently, lowering insurance premiums by raising deductibles frees up monthly cash flow for increased savings.

However, there is a critical contingency you must verify: a client must have sufficient emergency savings to cover an increased insurance deductible before implementing a high-deductible strategy. If they do not, an unforeseen accident could force them into high-interest debt, defeating the purpose of the strategy entirely.

Cash flow management is inherently vulnerable to real-world chaos—job losses, medical emergencies, or a blown transmission. Emergency funds protect a client's financial plan from unexpected negative cash flow events. They are the shock absorbers of the financial system.

To evaluate a client's liquidity buffer, we use the Emergency Fund Ratio:

Emergency Fund Ratio = Cash and Cash Equivalents / Monthly Non-Discretionary Cash Flows

The standard CFP benchmark for an emergency fund is three to six months of non-discretionary expenses. Notice the precise language here: we base the calculation on non-discretionary expenses, not total expenses. In a true emergency, we assume the client will halt all discretionary spending (vacations, entertainment).

Where a client falls on that three-to-six-month spectrum depends heavily on their household income stability:

- Married clients with dual stable incomes generally require an emergency fund closer to three months of non-discretionary expenses, as the probability of both spouses losing their jobs simultaneously is statistically lower.

- Clients with a single source of household income generally require an emergency fund closer to six months of non-discretionary expenses, as they lack a secondary income buffer if their primary cash inflow ceases.

As you prepare for the CFP® exam, remember that cash flow is an integrated ecosystem. Changing one variable—whether it is reducing a discretionary expense, raising an insurance deductible, or automating a savings transfer—ripples through the entire financial plan. Master the mechanics of cash flow, and you master the very foundation of financial planning.