Income tax fundamentals and calculations

Not sure you’re ready?

Take the ~3-minute readiness diagnostic and see where you stand.

The United States tax code operates as a vast, multi-tiered filtration system, systematically separating the total wealth an individual captures over a year from what they ultimately owe the federal government. Section 61 of the Internal Revenue Code lays the foundational bedrock for this system, defining gross income as all income from whatever source derived. For a financial planning professional, mastering the mechanics of this system is not merely an exercise in compliance; it is the fundamental mechanism through which wealth is preserved and optimized. Every dollar that passes through a client’s economic life is subject to specific structural rules, exclusions, and diversions. By understanding the precise anatomy of this calculation—from gross income down to the final tax refund or liability—you gain the ability to preemptively route your clients' money through the most efficient channels possible.

To calculate a client's tax, we must first determine what enters the tax funnel. Section 61 is notoriously broad. Gross income includes almost every inflow of wealth: compensation for services (wages, salaries, bonuses), net income from a business or profession, interest and dividend income, and income from rents and royalties. If a client receives an economic benefit, assume it is gross income unless the tax code explicitly shields it.

However, the IRS does provide powerful statutory shields. Certain inflows bypass the funnel entirely and are completely excluded from gross income. Understanding these is crucial for tax-efficient planning:

- Life insurance death benefits: When paid upon the death of the insured, these proceeds are generally excluded from the beneficiary's gross income.

- Municipal bond interest: Interest earned on state and local municipal bonds is generally excluded from federal gross income, making them highly attractive to clients in upper tax brackets.

- Gifts and inheritances: These transfers are excluded from the recipient's gross income (though they may be subject to separate transfer taxes for the donor).

The Alimony Pivot: The treatment of alimony provides a fascinating lesson in tax legislation timing. For divorce decrees executed before January 1, 2019, alimony payments are included in the recipient's gross income and act as an above-the-line deduction for the payer. However, the law changed fundamentally for divorce decrees executed after December 31, 2018. Under the new rules, alimony payments are entirely excluded from the recipient's gross income, and they are correspondingly not deductible by the payer. It is now a purely after-tax transfer of wealth.

Once we have gross income, the first set of filters applied are the above-the-line deductions. These are incredibly valuable because they reduce gross income to arrive at Adjusted Gross Income (AGI).

Why do we care if a deduction is "above" the line? Because AGI is the gravitational center of the entire tax return. A lower AGI opens the door to other tax benefits that phase out at higher income levels. Every dollar deducted here is a guaranteed reduction in taxable income, completely independent of whether the client chooses to itemize later.

Common above-the-line deductions include:

Retirement and Savings

- Traditional IRA Contributions: Contributions can qualify as an above-the-line deduction, though this deduction is subject to income phase-outs based on the client's AGI and active participation in workplace plans.

- Health Savings Accounts (HSAs): Contributions made to an HSA by an eligible individual (paired with a high-deductible health plan) are treated as a highly efficient above-the-line deduction.

- Bank Penalties: The penalty on the early withdrawal of savings from a bank time deposit (like breaking a CD early) is fully deductible above the line.

Self-Employment Deductions

The IRS recognizes that the self-employed pay both halves of the payroll tax and purchase their own benefits. To equalize the playing field with W-2 employees:

- Self-employed individuals can take an above-the-line deduction for 50 percent of their self-employment tax paid.

- They can also deduct 100 percent of health insurance premiums paid for themselves and their dependents as an above-the-line deduction.

Education Deductions

- Student Loan Interest: The student loan interest deduction is an above-the-line deduction, but it is strictly capped by a maximum annual dollar limit and is subject to income phase-outs based on AGI.

- Educator Expenses: Eligible educators can take a specific above-the-line deduction for qualifying out-of-pocket classroom expenses.

Formula Check: Total Gross Income – Allowable Above-The-Line Deductions = Adjusted Gross Income (AGI).

After establishing AGI, the tax code allows the taxpayer to filter out even more income to arrive at taxable income. Here, the system forces a mathematical choice. Taxpayers must choose between taking the standard deduction or itemizing their deductions. A rational taxpayer will always minimize their taxable income by subtracting the greater of the standard deduction or their total itemized deductions from their AGI.

The Standard Deduction

The standard deduction is an administrative convenience—a flat, predetermined dollar amount based strictly on a taxpayer's filing status (e.g., Single, Married Filing Jointly). To account for higher living costs and medical needs, taxpayers who are age 65 or older receive an increased standard deduction amount. Similarly, taxpayers who are legally blind also receive an increased standard deduction amount.

Itemized Deductions (Schedule A)

If a client's specific, IRS-allowed expenses exceed their standard deduction, they should itemize. Itemized deductions are specific below-the-line expenses claimed on Schedule A of Form 1040. As a planner, you will evaluate four major categories:

- Medical Expenses: Unreimbursed medical expenses are deductible, but they face a steep mathematical hurdle. They are deductible only to the extent the expenses exceed 7.5 percent of the client's AGI.

- State and Local Taxes (SALT): The itemized deduction for state and local taxes is severely capped. It is limited to a combined maximum of

\$10,000per year for married individuals filing jointly. Within this cap, the SALT deduction can include local property taxes. Furthermore, taxpayers must make a choice: they can deduct state income taxes or state sales taxes, but not both. - Mortgage Interest: Taxpayers can deduct interest paid on qualifying acquisition indebtedness (money used to buy, build, or substantially improve a home). The limits depend entirely on when the loan was secured:

- For mortgages originated on or before December 15, 2017, interest is deductible on up to

\$1,000,000of debt. - For mortgages originated after December 15, 2017, the limit drops, restricting the deduction to interest paid on up to

\$750,000of debt.

- For mortgages originated on or before December 15, 2017, interest is deductible on up to

- Charitable Contributions: Cash contributions to public charities are heavily incentivized and are deductible as an itemized deduction up to a generous 60 percent of the taxpayer's AGI.

The Qualified Business Income (QBI) Deduction

It is critical to note the structural placement of QBI. The Qualified Business Income deduction is unique; it is a below-the-line deduction that is subtracted after calculating Adjusted Gross Income to determine final taxable income, but it is available regardless of whether the taxpayer takes the standard deduction or itemizes.

Once you subtract the final deductions from AGI, you arrive at taxable income. We then apply the statutory progressive income tax brackets to this final taxable income figure to calculate the gross tax liability.

At this stage, we transition from deductions to credits. You must aggressively clarify this distinction for your clients:

- A tax deduction reduces the amount of income subject to taxation. Its actual cash value depends on the client's marginal tax bracket (a

\$1,000deduction in a 24% bracket saves\$240). - A tax credit reduces the actual tax liability on a dollar-for-dollar basis. A

\$1,000credit saves exactly\$1,000in taxes.

Tax credits are further divided into two distinct biological classes: nonrefundable and refundable.

- Nonrefundable tax credits can reduce a taxpayer's tax liability all the way to zero, but they stop there. They cannot result in a direct cash refund to the taxpayer for any excess credit amount.

- Refundable tax credits are far more powerful. They can reduce a taxpayer's tax liability below zero, actively generating a direct cash refund to the taxpayer for the credit amount that exceeds their tax liability.

Key Tax Credits to Master

1. Child and Family Credits

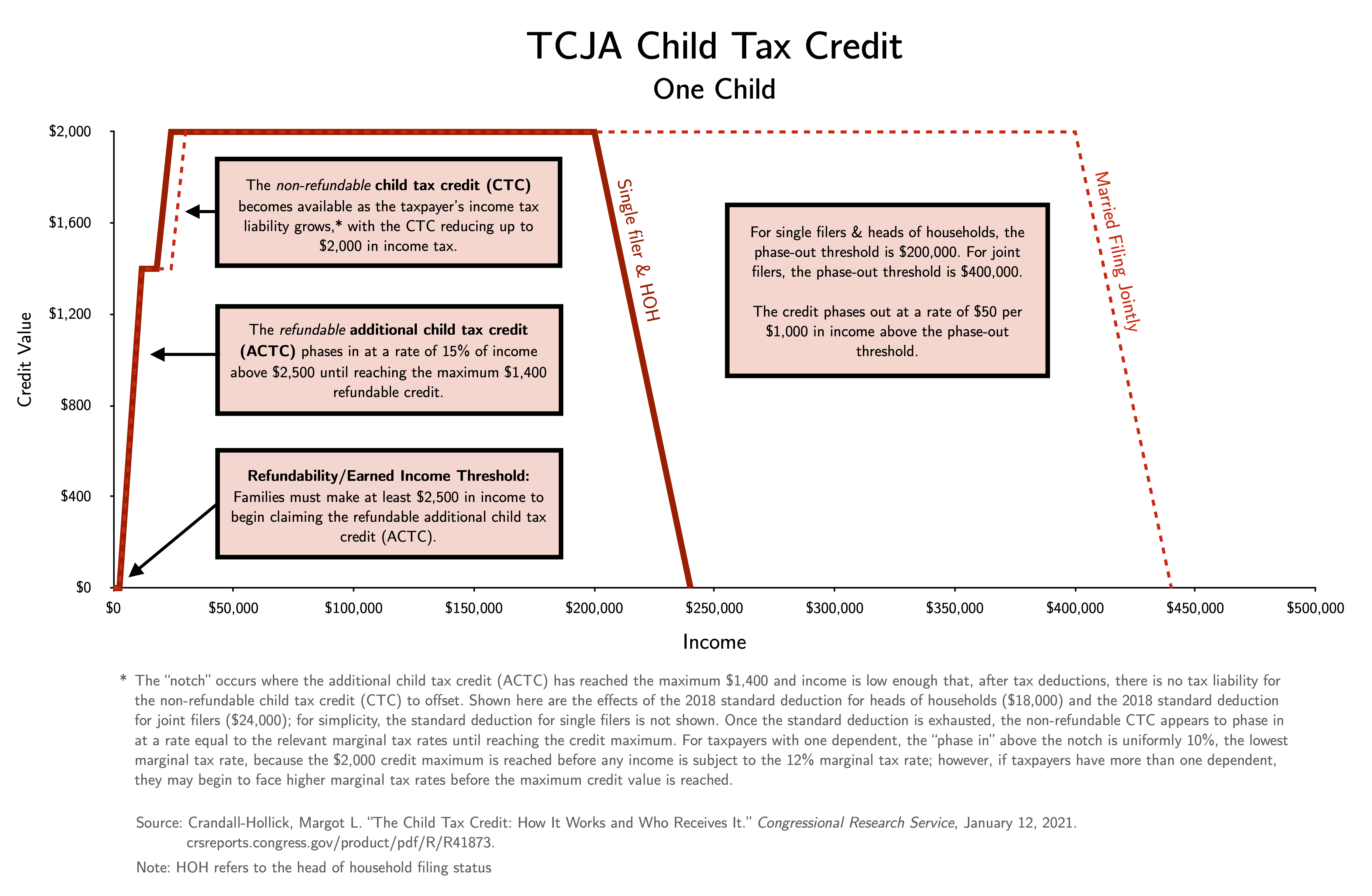

- Child Tax Credit: Available for a qualifying child who must be under age 17 at the end of the tax year. A specific portion of this credit is refundable, known technically as the Additional Child Tax Credit.

- Child and Dependent Care Credit: This is a nonrefundable tax credit that offsets a percentage of employment-related care expenses for qualifying dependents (e.g., daycare costs so the parents can work).

2. Educational Tax Credits The IRS offers two primary credits for higher education, but a taxpayer cannot claim both the American Opportunity Tax Credit and the Lifetime Learning Credit for the same student in the same tax year.

- American Opportunity Tax Credit (AOTC): Applies strictly to qualified education expenses incurred during the first four years of post-secondary education (undergraduate). It is highly sought after because a portion of the AOTC is a refundable tax credit.

- Lifetime Learning Credit (LLC): A nonrefundable educational tax credit that applies to qualified tuition and related expenses for eligible students enrolled in an eligible educational institution. Unlike the AOTC, the LLC is broadly available for an unlimited number of tax years per eligible student, making it ideal for graduate school or mid-career retraining.

3. Income and Savings Credits

- Earned Income Tax Credit (EITC): A fully refundable tax credit designed exclusively for working individuals with low-to-moderate earned income. Because it is fully refundable, it acts as a negative income tax, providing substantial cash refunds to working-class clients.

- Saver's Credit: A nonrefundable tax credit designed to encourage lower- and middle-income individuals to save for the future. It rewards eligible contributions to qualifying retirement plans or Individual Retirement Accounts.

The culmination of this massive mathematical journey occurs at the bottom of the 1040.

Net tax liability is calculated by subtracting all applicable nonrefundable and refundable tax credits from the gross tax liability. This number represents the total tax burden the client generated over the course of the year.

However, the US tax system operates on a "pay-as-you-go" basis. Throughout the year, the client has been dripping money into the IRS reservoir through tax prepayments. These prepayments primarily take two forms:

- Payroll withholdings collected systematically by employers.

- Estimated quarterly tax payments made directly by the taxpayer (highly common for your self-employed clients or those with massive investment income).

The final tax due or refund amount is determined by simply subtracting the total tax prepayments from the net tax liability. If the prepayments exceed the net liability, the IRS issues a refund of the difference. If the net liability exceeds the prepayments, the client must write a check to clear the balance.

By commanding this architecture—knowing precisely what constitutes gross income, aggressively maximizing above-the-line deductions to lower AGI, optimizing the standard-versus-itemized choice, and applying dollar-for-dollar tax credits—you transform the tax code from a punitive burden into an instrument of strategic financial planning.